RSS Feed

RSS Feed by Calculated Risk on 11/03/2023 09:21:00 AM

Friday, November 03, 2023

Comments on October Employment Report

The headline jobs number in the October employment report was below expectations, and employment for the previous two months was revised down by 101,000, combined. The participation rate and the employment population ratio both decreased, and the unemployment rate increased to 3.9%.

Leisure and hospitality gained 19 thousand jobs in October. At the beginning of the pandemic, in March and April of 2020, leisure and hospitality lost 8.2 million jobs, and are now down 223 thousand jobs since February 2020. So, leisure and hospitality has now added back about 97% all of the jobs lost in March and April 2020.

Construction employment increased 23 thousand and is now 425 thousand above the pre-pandemic level.

Manufacturing employment decreased 35 thousand jobs and is now 175 thousand above the pre-pandemic level.

In October, the year-over-year employment change was 2.97 million jobs.

Seasonal Retail Hiring

Typically, retail companies start hiring for the holiday season in October, and really increase hiring in November. Here is a graph that shows the historical net retail jobs added for October, November and December by year.

This graph really shows the collapse in retail hiring in 2008. Since then, seasonal hiring had increased back close to more normal levels. Note: I expect the long-term trend will be down with more and more internet holiday shopping.

This graph really shows the collapse in retail hiring in 2008. Since then, seasonal hiring had increased back close to more normal levels. Note: I expect the long-term trend will be down with more and more internet holiday shopping.Retailers hired 148 thousand workers Not Seasonally Adjusted (NSA) net in October. This was about the same as last year and suggests similar real retail sales this holiday season as last year.

This was seasonally adjusted (SA) to a gain of 1 thousand jobs in October.

Prime (25 to 54 Years Old) Participation

Since the overall participation rate is impacted by both cyclical (recession) and demographic (aging population, younger people staying in school) reasons, here is the employment-population ratio for the key working age group: 25 to 54 years old.

Since the overall participation rate is impacted by both cyclical (recession) and demographic (aging population, younger people staying in school) reasons, here is the employment-population ratio for the key working age group: 25 to 54 years old.The 25 to 54 participation rate decreased in October to 83.3% from 83.5% in September, and the 25 to 54 employment population ratio declined to 80.6% from 80.8% the previous month.

Both are close to the pre-pandemic levels.

Average Hourly Wages

The graph shows the nominal year-over-year change in "Average Hourly Earnings" for all private employees from the Current Employment Statistics (CES).

The graph shows the nominal year-over-year change in "Average Hourly Earnings" for all private employees from the Current Employment Statistics (CES).

Average Hourly Wages

The graph shows the nominal year-over-year change in "Average Hourly Earnings" for all private employees from the Current Employment Statistics (CES).

The graph shows the nominal year-over-year change in "Average Hourly Earnings" for all private employees from the Current Employment Statistics (CES). There was a huge increase at the beginning of the pandemic as lower paid employees were let go, and then the pandemic related spike reversed a year later.

Wage growth has trended down after peaking at 5.9% YoY in March 2022 and was at 4.1% YoY in October.

Wage growth has trended down after peaking at 5.9% YoY in March 2022 and was at 4.1% YoY in October.

On an annualized basis, wages increased 2.5% in October. Since wages increased sharply last November and December, it is likely YoY wage growth will slow further over the next couple of months.

Part Time for Economic Reasons

From the BLS report:

From the BLS report:"The number of persons employed part time for economic reasons, at 4.3 million, changed little in October. These individuals, who would have preferred full-time employment, were working part time because their hours had been reduced or they were unable to find full-time jobs."The number of persons working part time for economic reasons increased in October to 4.28 million from 4.07 million in September. This is below pre-recession levels.

These workers are included in the alternate measure of labor underutilization (U-6) that increased to 7.2% from 7.0% in the previous month. This is down from the record high in April 22.9% and up from the lowest level on record (seasonally adjusted) in December 2022 (6.5%). (This series started in 1994). This measure is above the 7.0% level in February 2020 (pre-pandemic).

Unemployed over 26 Weeks

This graph shows the number of workers unemployed for 27 weeks or more.

This graph shows the number of workers unemployed for 27 weeks or more. According to the BLS, there are 1.282 million workers who have been unemployed for more than 26 weeks and still want a job, up from 1.216 million the previous month.

This is above the pre-pandemic levels.

Job Streak

Through October 2023, the employment report indicated positive job growth for 34 consecutive months, putting the current streak in 5th place of the longest job streaks in US history (since 1939).

| Headline Jobs, Top 10 Streaks | ||

|---|---|---|

| Year Ended | Streak, Months | |

| 1 | 2019 | 100 |

| 2 | 1990 | 48 |

| 3 | 2007 | 46 |

| 4 | 1979 | 45 |

| 5 | 20231 | 34 |

| 6 tie | 1943 | 33 |

| 6 tie | 1986 | 33 |

| 6 tie | 2000 | 33 |

| 9 | 1967 | 29 |

| 10 | 1995 | 25 |

| 1Currrent Streak | ||

Summary:

The headline monthly jobs number was below consensus expectations and employment for the previous two months was revised down by 101,000, combined. The participation rate and the employment population ratio both decreased, and the unemployment rate increased to 3.9%.

This was a weaker than expected report, however the strikes reduced employment by about 30 thousand, and those jobs will likely be added back in November.

October Employment Report: 150 thousand Jobs, 3.9% Unemployment Rate

by Calculated Risk on 11/03/2023 08:30:00 AM

From the BLS:

Total nonfarm payroll employment increased by 150,000 in October, and the unemployment rate changed little at 3.9 percent, the U.S. Bureau of Labor Statistics reported today. Job gains occurred in health care, government, and social assistance. Employment declined in manufacturing due to strike activity.

...

The change in total nonfarm payroll employment for August was revised down by 62,000, from +227,000 to +165,000, and the change for September was revised down by 39,000, from +336,000 to +297,000. With these revisions, employment in August and September combined is 101,000 lower than previously reported.

emphasis added

Click on graph for larger image.

Click on graph for larger image.The first graph shows the jobs added per month since January 2021.

Total payrolls increased by 150 thousand in October. Private payrolls increased by 99 thousand, and public payrolls increased 51 thousand.

Payrolls for August and September were revised down 101 thousand, combined.

Payrolls for August and September were revised down 101 thousand, combined.

The second graph shows the year-over-year change in total non-farm employment since 1968.

The second graph shows the year-over-year change in total non-farm employment since 1968.In October, the year-over-year change was 2.97 million jobs. Employment was up solidly year-over-year but has slowed to more normal levels of job growth recently.

The third graph shows the employment population ratio and the participation rate.

The Labor Force Participation Rate was decreased to 62.7% in October, from 62.8% in September. This is the percentage of the working age population in the labor force.

The Labor Force Participation Rate was decreased to 62.7% in October, from 62.8% in September. This is the percentage of the working age population in the labor force. The Employment-Population ratio decreased to 60.2% from 60.4% (blue line).

I'll post the 25 to 54 age group employment-population ratio graph later.

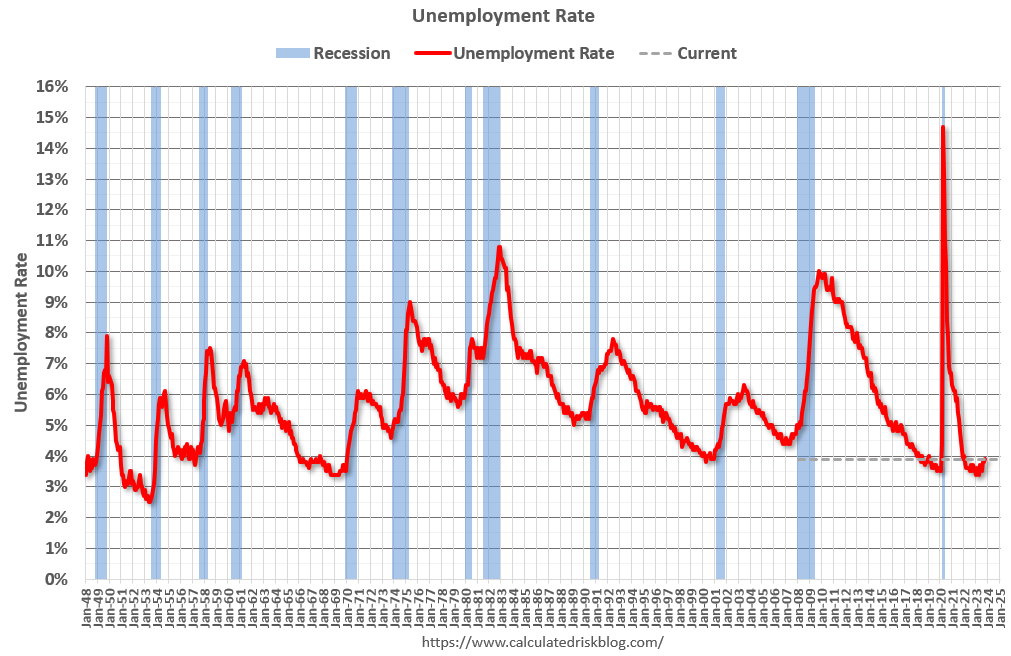

The fourth graph shows the unemployment rate.

The fourth graph shows the unemployment rate. The unemployment rate increased to 3.9% in October from 3.8% in September.

This was below consensus expectations, and August and September payrolls were revised down by 101,000 combined.

Thursday, November 02, 2023

Friday: Employment Report

by Calculated Risk on 11/02/2023 08:04:00 PM

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

Rates were at 8% just two weeks ago!

Thursday:

• At 8:30 AM ET, Employment Report for October. The consensus is for 168,000 jobs added, and for the unemployment rate to be unchanged at 3.8%.

• At 10:00 AM, the ISM Services Index for October. The consensus is for a decrease to 53.0 from 53.6.

Thursday:

• At 8:30 AM ET, Employment Report for October. The consensus is for 168,000 jobs added, and for the unemployment rate to be unchanged at 3.8%.

• At 10:00 AM, the ISM Services Index for October. The consensus is for a decrease to 53.0 from 53.6.

October Employment Preview

by Calculated Risk on 11/02/2023 03:56:00 PM

On Friday at 8:30 AM ET, the BLS will release the employment report for October. The consensus is for 168,000 jobs added, and for the unemployment rate to be unchanged at 3.8%.

There were 336,000 jobs added in September, and the unemployment rate was at 3.8%

From BofA economists:

"For the October employment report, we forecast nonfarm payroll job growth will slow from 336k in September to 230k ... Given our expectation for the participation rate to hold at 62.8% and for job growth to be strong, we expect the unemployment rate will fall to 3.7% from 3.8%."From Goldman Sachs:

"We estimate nonfarm payrolls rose by 195k in October ... tight labor markets may have incentivized a pull-forward of pre-holiday hiring, for example in the retail sector. ... We estimate that the unemployment rate declined to 3.7% ... Our forecast reflects a solid rise in household employment—striking workers are counted as employed in the household survey—and unchanged labor force participation at 62.8%."• ADP Report: The ADP employment report showed 113,000 private sector jobs were added in October. This suggests job gains below consensus expectations, however, in general, ADP hasn't been very useful in forecasting the BLS report.

• ISM Surveys: Note that the ISM surveys are diffusion indexes based on the number of firms hiring (not the number of hires). The ISM® manufacturing employment index decreased in October to 46.8%, down from 51.2% the previous month. This would suggest about 35,000 jobs lost in manufacturing. The ADP report indicated 3,000 manufacturing jobs gained in October.

The ISM® services employment index will be released tomorrow.

• Unemployment Claims: The weekly claims report showed about the same number of initial unemployment claims during the reference week (includes the 12th of the month) from 202,000 in September to 200,000 in October. This suggests about the same number of layoffs in October as in September.

• COVID: As far as the pandemic, the number of patients hospitalized during the reference week in October was around 14,000, down from 16,000 in September.

• Conclusion: Most of the key indicators suggest another solid employment report in October. We've seen an upside surprise in employment almost every month, however someday we will see a downside surprise. My guess is the headline number will be close to the consensus.

Realtor.com Reports Weekly New Listings UP 5.6% YoY; Active Inventory Down 1.0% YoY

by Calculated Risk on 11/02/2023 01:40:00 PM

Realtor.com has monthly and weekly data on the existing home market. Here is their weekly report: Weekly Housing Trends View — Data Week Ending Oct 28, 2023

• Active inventory declined, with for-sale homes lagging behind year ago levels by 1.0%.

For 19 straight weeks, the number of homes available for sale has registered below that of the previous year.

• New listings–a measure of sellers putting homes up for sale–were up this week, by 5.6% from one year ago.

Since mid-2022, new listings have registered lower than prior year levels, as the mortgage rate lock-in effect freezes homeowners with low-rate existing mortgages in place. This past week, the trend abruptly reversed as new listings during the week outpaced the same week in the previous year by 5.6%. While growth in new listings is a needed step for the market to return to normal, this growth rate reflects a rapid decline last year compared to a more stable newly listed homes pace this year, as we are lapping a period of time last year when new listing activity was unseasonably low due to the said mortgage rate lock-in effect.

Here is a graph of the year-over-year change in inventory according to realtor.com.

Here is a graph of the year-over-year change in inventory according to realtor.com. Inventory was down 1.0% year-over-year - this was the 19th consecutive week with a YoY decrease following 58 consecutive weeks with a YoY increase in inventory.

The YoY decline in inventory has generally been getting smaller recently and I expect inventory to be up YoY soon - but still historically very low.

New listings really collapsed a year ago, so the YoY comparison for new listings is easier now - and although new listings remain historically very low, new listings are now up YoY.

Asking Rents Down 1.2% Year-over-year

by Calculated Risk on 11/02/2023 11:03:00 AM

Today, in the Calculated Risk Real Estate Newsletter: Asking Rents Down 1.2% Year-over-year

A brief excerpt:

Tracking rents is important for understanding the dynamics of the housing market. For example, the sharp increase in rents helped me deduce that there was a surge in household formation in 2021 (See from September 2021: Household Formation Drives Housing Demand).There is much more in the article. You can subscribe at https://calculatedrisk.substack.com/

The surge in household formation has been confirmed (mostly due to work-from-home), and this led to the supposition that household formation would slow sharply in 2023 (mostly confirmed) and that asking rents might decrease in 2023 on a year-over-year basis (now negative year-over-year).

Recent data suggests household formation has slowed sharply and asking rents are declining year-over-year. With a near record number of multi-family units under construction, slow household formation, rising vacancy rates, and soft rents, most builders expect to start fewer multi-family units in 2024.

Rick Palacios Jr., Director of Research at John Burns Research and Consulting noted yesterday:

Apartment developers and investors we just surveyed expect a big drop in starts over the next 12 months....

25% expect apartment starts to fall by 50%+, and 52% expect a drop of 20%+. Very, very few expect growth ahead.

With slow household formation, more supply coming on the market and a rising rental vacancy rate, rents will be under pressure all year and multi-family starts will decline in 2024. See: Forecast: Multifamily Starts will Decline Sharply

Weekly Initial Unemployment Claims Increase to 217,000

by Calculated Risk on 11/02/2023 08:30:00 AM

The DOL reported:

In the week ending October 28, the advance figure for seasonally adjusted initial claims was 217,000, an increase of 5,000 from the previous week's revised level. The previous week's level was revised up by 2,000 from 210,000 to 212,000. The 4-week moving average was 210,000, an increase of 2,000 from the previous week's revised average. The previous week's average was revised up by 500 from 207,500 to 208,000.The following graph shows the 4-week moving average of weekly claims since 1971.

emphasis added

Click on graph for larger image.

Click on graph for larger image.The dashed line on the graph is the current 4-week average. The four-week average of weekly unemployment claims increased to 210,000.

The previous week was revised up.

Weekly claims were sligthly higher than the consensus forecast.

Wednesday, November 01, 2023

Thursday: Unemployment Claims

by Calculated Risk on 11/01/2023 08:56:00 PM

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

Thursday:

• At 8:30 AM: The initial weekly unemployment claims report will be released. The consensus is for 214 thousand initial claims, up from 210 thousand last week.

Vehicles Sales decrease to 15.5 million SAAR in October; Up 6% YoY

by Calculated Risk on 11/01/2023 05:11:00 PM

Wards Auto released their estimate of light vehicle sales for October: October U.S. Light-Vehicle Sales Miss Expectations but Still Record 6% Increase (pay site).

October’s results were below expectations, apparently due to weakness at the end of the month. Most automakers finished below mid-month projections for each, thus the industry’s overall weaker results can’t be blamed on underestimating the impacts to Ford, GM and Stellantis from the strike-related plant shutdowns. The results also show that other automakers did not benefit from losses at the Detroit 3. Still, most manufacturers recorded year-over-year gains and the industry posted its 14th straight increase.

Click on graph for larger image.

Click on graph for larger image.This graph shows light vehicle sales since 2006 from the BEA (blue) and Wards Auto's estimate for September (red).

The impact of COVID-19 was significant, and April 2020 was the worst month. After April 2020, sales increased, and were close to sales in 2019 (the year before the pandemic). However, sales decreased in 2021 due to supply issues. The "supply chain bottom" was in September 2021.

The second graph shows light vehicle sales since the BEA started keeping data in 1967.

The second graph shows light vehicle sales since the BEA started keeping data in 1967. Sales in October were below Ward's forecast, but above the consensus forecast.

FOMC Statement: No Change to Rates

by Calculated Risk on 11/01/2023 02:00:00 PM

Fed Chair Powell press conference video here or on YouTube here, starting at 2:30 PM ET.

FOMC Statement:

Recent indicators suggest that economic activity expanded at a strong pace in the third quarter. Job gains have moderated since earlier in the year but remain strong, and the unemployment rate has remained low. Inflation remains elevated.

The U.S. banking system is sound and resilient. Tighter financial and credit conditions for households and businesses are likely to weigh on economic activity, hiring, and inflation. The extent of these effects remains uncertain. The Committee remains highly attentive to inflation risks.

The Committee seeks to achieve maximum employment and inflation at the rate of 2 percent over the longer run. In support of these goals, the Committee decided to maintain the target range for the federal funds rate at 5-1/4 to 5-1/2 percent. The Committee will continue to assess additional information and its implications for monetary policy. In determining the extent of additional policy firming that may be appropriate to return inflation to 2 percent over time, the Committee will take into account the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation, and economic and financial developments. In addition, the Committee will continue reducing its holdings of Treasury securities and agency debt and agency mortgage-backed securities, as described in its previously announced plans. The Committee is strongly committed to returning inflation to its 2 percent objective.

In assessing the appropriate stance of monetary policy, the Committee will continue to monitor the implications of incoming information for the economic outlook. The Committee would be prepared to adjust the stance of monetary policy as appropriate if risks emerge that could impede the attainment of the Committee's goals. The Committee's assessments will take into account a wide range of information, including readings on labor market conditions, inflation pressures and inflation expectations, and financial and international developments.

Voting for the monetary policy action were Jerome H. Powell, Chair; John C. Williams, Vice Chair; Michael S. Barr; Michelle W. Bowman; Lisa D. Cook; Austan D. Goolsbee; Patrick Harker; Philip N. Jefferson; Neel Kashkari; Adriana D. Kugler; Lorie K. Logan; and Christopher J. Waller.

emphasis added