RSS Feed

RSS Feed by Calculated Risk on 1/08/2024 10:58:00 AM

Monday, January 08, 2024

Wholesale Used Car Prices Decreased 0.5% in December; Down 7.0% Year-over-year

From Manheim Consulting today: Wholesale Used-Vehicle Prices Decrease in December, End Year Down 7.0%

Wholesale used-vehicle prices (on a mix, mileage, and seasonally adjusted basis) decreased 0.5% in December from November. The Manheim Used Vehicle Value Index (MUVVI) dropped to 204.0, down 7.0% from a year ago. Compared to December 2021, used-vehicle values are down nearly 21%.

“December’s decline brought a volatile year to a close,” said Jeremy Robb, senior director of Economic and Industry Insights for Cox Automotive. “The spring bounce was much more pronounced than expected in 2023, and prices slid just as rapidly after that bounce, finishing more calmly in December as expected. The 7.0% year-over-year loss was larger than our original forecast, but it pales in comparison to the nearly 15% decline we had a year earlier. 2024 is looking to be less volatile than 2023, but we’ve been taught to expect the unexpected in the wholesale market.”

The seasonal adjustment reduced the December decrease. The non-adjusted price in December declined by 2.0% compared to November, moving the unadjusted average price down 7.7% year over year.

emphasis added

Click on graph for larger image.

Click on graph for larger image.This index from Manheim Consulting is based on all completed sales transactions at Manheim’s U.S. auctions.

The Manheim index suggests used car prices decreased in December (seasonally adjusted) and were down 7.0% year-over-year (YoY).

Housing January 8th Weekly Update: Inventory Down 2.7% Week-over-week, Up 5.7% Year-over-year

by Calculated Risk on 1/08/2024 08:21:00 AM

Altos reports that active single-family inventory was down 2.7% week-over-week. Inventory will likely decrease seasonally until the Spring.

Click on graph for larger image.

Click on graph for larger image.This inventory graph is courtesy of Altos Research.

As of January 5th, inventory was at 499 thousand (7-day average), compared to 513 thousand the prior week.

Inventory is still far below pre-pandemic levels.

The red line is for 2024. The black line is for 2019. Note that inventory is up from the record low for the same week in 2022, but still well below normal levels.

Inventory was up 5.7% compared to the same week in 2023 (last week it was up 4.4%), and down 39.0% compared to the same week in 2019 (last week down 34.4%).

Back in June 2023, inventory was down almost 54% compared to 2019, so the gap to more normal inventory levels is closing.

Mike Simonsen discusses this data regularly on Youtube.

Sunday, January 07, 2024

Sunday Night Futures

by Calculated Risk on 1/07/2024 07:08:00 PM

Weekend:

• Schedule for Week of January 7, 2024

Monday:

• No major economic releases scheduled.

From CNBC: Pre-Market Data and Bloomberg futures S&P 500 are up slightly and DOW futures are down 43 (fair value).

Oil prices were up over the last week with WTI futures at $73.81 per barrel and Brent at $78.76 per barrel. A year ago, WTI was at $74, and Brent was at $76 - so WTI oil prices were mostly unchanged year-over-year.

Here is a graph from Gasbuddy.com for nationwide gasoline prices. Nationally prices are at $3.06 per gallon. A year ago, prices were at $3.26 per gallon, so gasoline prices are down $0.20 year-over-year.

Question #6 for 2024: What will the Fed Funds rate be in December 2024?

by Calculated Risk on 1/07/2024 09:57:00 AM

Earlier I posted some questions on my blog for next year: Ten Economic Questions for 2024. Some of these questions concern real estate (inventory, house prices, housing starts, new home sales), and I’ll post thoughts on those in the newsletter (others like GDP and employment will be on this blog).

I'm adding some thoughts, and maybe some predictions for each question.

6) Monetary Policy: To slow inflation, the FOMC raised the federal funds rate four times in 2023 from "4-1/4 to 4-1/2 percent" at the beginning of 2023, to "5-1/4 to 5-1/2" at the end of the year. Most FOMC participants expect around three 25 bp rate cuts in 2024. What will the Fed Funds rate be in December 2024?

As of December, looking at the "dot plot", the FOMC participants see the following number of rate cuts in 2024:

| 25 bp Rate Cuts | FOMC Members 2024 |

|---|---|

| No Change | 2 |

| One Rate Cut | 1 |

| Two Rate Cuts | 5 |

| Three Rate Cuts | 6 |

| Four Rate Cuts | 4 |

| More than Four | 1 |

The main view of the FOMC is for two to four rate cuts in 2024.

However, currently policy is restrictive with the Fed Funds rate range at '5-1/4 to 5-1/2' percent and core PCE inflation at 3.2% year-over-year in November. If we look at the last 6 months, inflation is even lower and policy even more restrictive.

PCE Price Index: 2.0% (over last 6 months annualized)

Core PCE Prices: 1.9%

Core minus Housing: 1.1%

If inflation continues to stay at the same level as the last 6 months or soften further (next question), the FOMC will have to start cutting rates soon.

“We are aware of the risk that we would hang on too long. We know that is a risk and we are very focused on not making that mistake.”

The next FOMC meeting ends on January 31st, and it appears the Fed will hold rates steady at that meeting. There will be two key December inflation reports prior to that meeting, with CPI on January 11th, and PCE on January 26th. If both reports are in line with expectations, the FOMC will likely hint at the first rate cut in March.

With inflation at target over the last 6 months, my sense is the FOMC will reduce rates more than they currently expect. My guess is there will be around 5 rate cuts in 2024, and the first cut is likely in March.

I also expect the FOMC to start discussing slowing balance sheet runoff late in the year.

Here are the Ten Economic Questions for 2024 and a few predictions:

• Question #1 for 2024: How much will the economy grow in 2024? Will there be a recession in 2024?

• Question #2 for 2024: How much will job growth slow in 2024? Or will the economy lose jobs?

• Question #3 for 2024: What will the unemployment rate be in December 2024?

• Question #4 for 2024: What will the participation rate be in December 2024?

• Question #5 for 2024: What will the YoY core inflation rate be in December 2024?

• Question #6 for 2024: What will the Fed Funds rate be in December 2024?

• Question #7 for 2024: How much will wages increase in 2024?

• Question #8 for 2024: How much will Residential investment change in 2024? How about housing starts and new home sales in 2024?

• Question #9 for 2024: What will happen with house prices in 2024?

• Question #10 for 2024: Will inventory increase further in 2024?

Saturday, January 06, 2024

Real Estate Newsletter Articles this Week: What will happen with house prices in 2024?

by Calculated Risk on 1/06/2024 02:11:00 PM

At the Calculated Risk Real Estate Newsletter this week:

• Question #9 for 2024: What will happen with house prices in 2024?

• Asking Rents Mostly Unchanged Year-over-year

• Question #8 for 2024: How much will Residential investment change in 2024? How about housing starts and new home sales in 2024?

This is usually published 4 to 6 times a week and provides more in-depth analysis of the housing market.

Schedule for Week of January 7, 2024

by Calculated Risk on 1/06/2024 08:11:00 AM

The key reports this week are December CPI and the November trade deficit.

No major economic releases scheduled.

6:00 AM: NFIB Small Business Optimism Index for December.

8:30 AM: Trade Balance report for November from the Census Bureau.

8:30 AM: Trade Balance report for November from the Census Bureau. This graph shows the U.S. trade deficit, with and without petroleum, through the most recent report. The blue line is the total deficit, and the black line is the petroleum deficit, and the red line is the trade deficit ex-petroleum products.

The consensus is the trade deficit to be $65.0 billion. The U.S. trade deficit was at $64.3 billion in October.

7:00 AM ET: The Mortgage Bankers Association (MBA) will release the results for the mortgage purchase applications index.

8:30 AM: The initial weekly unemployment claims report will be released. The consensus is for 215 thousand, up from 202 thousand.

8:30 AM: The Consumer Price Index for December from the BLS. The consensus is for 0.2% increase in CPI, and a 0.2% increase in core CPI. The consensus is for CPI to be up 3.2% year-over-year and core CPI to be up 3.9% YoY.

8:30 AM ET: The Producer Price Index for December from the BLS. The consensus is for a 0.1% increase in PPI, and a 0.2% increase in core PPI.

Friday, January 05, 2024

Jan 5th COVID Update: Deaths and Hospitalizations Increased

by Calculated Risk on 1/05/2024 07:47:00 PM

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

Due to changes at the CDC, weekly cases are no longer updated.

For deaths, I'm currently using 4 weeks ago for "now", since the most recent three weeks will be revised significantly.

Hospitalizations have almost quintupled from a low of 5,150 in June 2023.

Hospitalizations are far below the peak of 150,000 in January 2022.

| COVID Metrics | ||||

|---|---|---|---|---|

| Now | Week Ago | Goal | ||

| Hospitalized2🚩 | 25,430 | 22,242 | ≤3,0001 | |

| Deaths per Week2🚩 | 1,614 | 1,605 | ≤3501 | |

| 1my goals to stop weekly posts, 2Weekly for Currently Hospitalized, and Deaths 🚩 Increasing number weekly for Hospitalized and Deaths ✅ Goal met. | ||||

Click on graph for larger image.

Click on graph for larger image.This graph shows the weekly (columns) number of deaths reported.

Weekly deaths have more than tripled from a low of 485 in early July. Still weekly deaths are far below the weekly peak of 26,000 in January 2021.

And here is a new graph I'm following on COVID in wastewater as of Dec 30th:

This appears to be a leading indicator for COVID hospitalizations and deaths.

This appears to be a leading indicator for COVID hospitalizations and deaths.COVID in wastewater is at the highest level since January 2022 (about 55% that peak), and that suggests deaths will likely increase further over the next several weeks.

Q4 GDP Tracking: 1.4% to 2.5%

by Calculated Risk on 1/05/2024 02:30:00 PM

From Goldman:

Following today’s data, we left our Q4 GDP tracking estimate unchanged at +1.4% (qoq ar) and our Q4 domestic final sales growth forecast unchanged at +2.2% (qoq ar). [Jan 5th estimate]And from the Altanta Fed: GDPNow

emphasis added

The GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the fourth quarter of 2023 is 2.5 percent on January 3, up from 2.0 percent on January 2. [Jan 3rd estimate]

Question #7 for 2024: How much will wages increase in 2024?

by Calculated Risk on 1/05/2024 12:11:00 PM

Earlier I posted some questions on my blog for next year: Ten Economic Questions for 2024. Some of these questions concern real estate (inventory, house prices, housing starts, new home sales), and I’ll post thoughts on those in the newsletter (others like GDP and employment will be on this blog).

I'm adding some thoughts, and maybe some predictions for each question.

7) Wage Growth: Wage growth was solid in 2023, up 4.0% year-over-year as of November, but down from 4.8% YoY in 2022. How much will wages increase in 2024?

The most followed wage indicator is the “Average Hourly Earnings” from the Current Employment Statistics (CES) (aka "Establishment") monthly employment report.

Click on graph for larger image.

Click on graph for larger image.

The graph shows the nominal year-over-year change in "Average Hourly Earnings" for all private employees. There was a huge increase at the beginning of the pandemic as lower paid employees were let go, and then the pandemic related spike reversed a year later.

Real wage growth has trended down after peaking at 5.6% YoY in March 2022 and was at 4.1% YoY in December 2023. Although wage growth was above expectations in December, the trend is clearly down.

There are two quarterly sources for earnings data: 1) “Hourly Compensation,” from the BLS’s Productivity and Costs; and 2) the Employment Cost Index which includes wage/salary and benefit compensation. All three data series are different, and most of the focus recently has been the CES series (used in the graph above).

The second graph is from the Atlanta Fed Wage Tracker. This measure is the year-over-year change in nominal wages for individuals.

The second graph is from the Atlanta Fed Wage Tracker. This measure is the year-over-year change in nominal wages for individuals.By following wage changes for individuals, this removes the demographic composition effects (older workers who are retiring tend to be higher paid, and younger workers just entering the workforce tend to be lower paid).

The Atlanta Fed Wage tracker showed nominal wage growth increased sharply in 2021 and for most of 2022. In November 2023, the smoothed 3-month average wage growth was at 5.2% year-over-year, down from a peak of 6.7% in July 2022.

Clearly wage growth is slowing and I expect to see some further decreases in both the Average hourly earnings from the CES, and in the Atlanta Fed Wage Tracker. My sense is nominal wages will increase close to 3.5% YoY in 2024 according to the CES.

Here are the Ten Economic Questions for 2024 and a few predictions:

• Question #1 for 2024: How much will the economy grow in 2024? Will there be a recession in 2024?

• Question #2 for 2024: How much will job growth slow in 2024? Or will the economy lose jobs?

• Question #3 for 2024: What will the unemployment rate be in December 2024?

• Question #4 for 2024: What will the participation rate be in December 2024?

• Question #5 for 2024: What will the YoY core inflation rate be in December 2024?

• Question #6 for 2024: What will the Fed Funds rate be in December 2024?

• Question #7 for 2024: How much will wages increase in 2024?

• Question #8 for 2024: How much will Residential investment change in 2024? How about housing starts and new home sales in 2024?

• Question #9 for 2024: What will happen with house prices in 2024?

• Question #10 for 2024: Will inventory increase further in 2024?

Comments on December Employment Report

by Calculated Risk on 1/05/2024 09:26:00 AM

The headline jobs number in the December employment report was above expectations, however employment for the previous two months was revised down by 71,000, combined. The participation rate and the employment population ratio both decreased, and the unemployment rate was unchanged at 3.7%.

Leisure and hospitality gained 40 thousand jobs in December. At the beginning of the pandemic, in March and April of 2020, leisure and hospitality lost 8.2 million jobs, and are now down 163 thousand jobs since February 2020. So, leisure and hospitality has now added back about 98% all of the jobs lost in March and April 2020.

Construction employment increased 17 thousand and is now 448 thousand above the pre-pandemic level.

Manufacturing employment increased 6 thousand jobs and is now 201 thousand above the pre-pandemic level.

Seasonal Retail Hiring

Typically, retail companies start hiring for the holiday season in October, and really increase hiring in November. Here is a graph that shows the historical net retail jobs added for October, November and December by year.

This graph really shows the collapse in retail hiring in 2008. Since then, seasonal hiring had increased back close to more normal levels. Note: I expect the long-term trend will be down with more and more internet holiday shopping.

This graph really shows the collapse in retail hiring in 2008. Since then, seasonal hiring had increased back close to more normal levels. Note: I expect the long-term trend will be down with more and more internet holiday shopping.Retailers hired 120 thousand workers Not Seasonally Adjusted (NSA) net in December. This was above last year.

This was seasonally adjusted (SA) to a gain of 17 thousand jobs in December.

Prime (25 to 54 Years Old) Participation

Since the overall participation rate is impacted by both cyclical (recession) and demographic (aging population, younger people staying in school) reasons, here is the employment-population ratio for the key working age group: 25 to 54 years old.

Since the overall participation rate is impacted by both cyclical (recession) and demographic (aging population, younger people staying in school) reasons, here is the employment-population ratio for the key working age group: 25 to 54 years old.The 25 to 54 years old participation rate declined in December to 83.2% from 83.3% in November, and the 25 to 54 employment population ratio declined to 80.4% from 80.7% the previous month.

Both are close to the pre-pandemic levels.

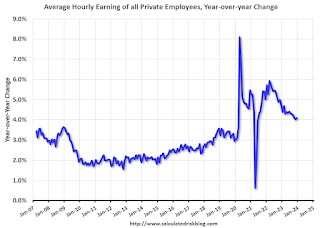

Average Hourly Wages

The graph shows the nominal year-over-year change in "Average Hourly Earnings" for all private employees from the Current Employment Statistics (CES).

The graph shows the nominal year-over-year change in "Average Hourly Earnings" for all private employees from the Current Employment Statistics (CES).

Average Hourly Wages

The graph shows the nominal year-over-year change in "Average Hourly Earnings" for all private employees from the Current Employment Statistics (CES).

The graph shows the nominal year-over-year change in "Average Hourly Earnings" for all private employees from the Current Employment Statistics (CES). There was a huge increase at the beginning of the pandemic as lower paid employees were let go, and then the pandemic related spike reversed a year later.

Wage growth has trended down after peaking at 5.9% YoY in March 2022 and was at 4.1% YoY in December.

Wage growth has trended down after peaking at 5.9% YoY in March 2022 and was at 4.1% YoY in December.

Part Time for Economic Reasons

From the BLS report:

From the BLS report:"The number of persons employed part time for economic reasons, at 4.2 million, changed little in December but was up by 333,000 over the year. These individuals, who would have preferred full-time employment, were working part time because their hours had been reduced or they were unable to find full-time jobs."The number of persons working part time for economic reasons decreased in December to 4.21 million from 3.99 million in November. This is at pre-recession levels.

These workers are included in the alternate measure of labor underutilization (U-6) that increased to 7.1% from 7.0% in the previous month. This is down from the record high in April 2020 of 23.0% and up from the lowest level on record (seasonally adjusted) in December 2022 (6.5%). (This series started in 1994). This measure is close to the 7.0% level in February 2020 (pre-pandemic).

Unemployed over 26 Weeks

This graph shows the number of workers unemployed for 27 weeks or more.

This graph shows the number of workers unemployed for 27 weeks or more. According to the BLS, there are 1.245 million workers who have been unemployed for more than 26 weeks and still want a job, up from 1.220 million the previous month.

This is down from post-pandemic high of 4.174 million, and up from the recent low of 1.050 million.

This is close to pre-pandemic levels.

Job Streak

Summary:

The headline monthly jobs number was above consensus expectations; however, employment for the previous two months was revised down by 71,000, combined. The participation rate and the employment population ratio both decreased, and the unemployment rate was unchanged at 3.7%.

This is close to pre-pandemic levels.

Job Streak

Through December 2023, the employment report indicated positive job growth for 36 consecutive months, putting the current streak in 5th place of the longest job streaks in US history (since 1939).

| Headline Jobs, Top 10 Streaks | ||

|---|---|---|

| Year Ended | Streak, Months | |

| 1 | 2019 | 100 |

| 2 | 1990 | 48 |

| 3 | 2007 | 46 |

| 4 | 1979 | 45 |

| 5 | 20231 | 36 |

| 6 tie | 1943 | 33 |

| 6 tie | 1986 | 33 |

| 6 tie | 2000 | 33 |

| 9 | 1967 | 29 |

| 10 | 1995 | 25 |

| 1Currrent Streak | ||

Summary:

The headline monthly jobs number was above consensus expectations; however, employment for the previous two months was revised down by 71,000, combined. The participation rate and the employment population ratio both decreased, and the unemployment rate was unchanged at 3.7%.

Another solid employment report.