RSS Feed

RSS Feed by Calculated Risk on 4/17/2024 01:41:00 PM

Wednesday, April 17, 2024

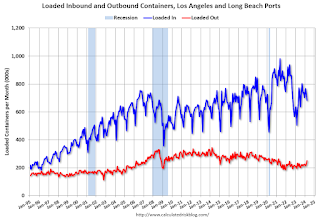

LA Port Traffic Increased Year-over-year in March

Container traffic gives us an idea about the volume of goods being exported and imported - and usually some hints about the trade report since LA area ports handle about 40% of the nation's container port traffic.

The following graphs are for inbound and outbound traffic at the ports of Los Angeles and Long Beach in TEUs (TEUs: 20-foot equivalent units or 20-foot-long cargo container).

To remove the strong seasonal component for inbound traffic, the first graph shows the rolling 12-month average.

Click on graph for larger image.

Click on graph for larger image.

On a rolling 12-month basis, inbound traffic increased 1.0% in March compared to the rolling 12 months ending in February. Outbound traffic increased 0.7% compared to the rolling 12 months ending the previous month.

The 2nd graph is the monthly data (with a strong seasonal pattern for imports).

Usually imports peak in the July to October period as retailers import goods for the Christmas holiday, and then decline sharply and bottom in the Winter depending on the timing of the Chinese New Year.

Usually imports peak in the July to October period as retailers import goods for the Christmas holiday, and then decline sharply and bottom in the Winter depending on the timing of the Chinese New Year.

Usually imports peak in the July to October period as retailers import goods for the Christmas holiday, and then decline sharply and bottom in the Winter depending on the timing of the Chinese New Year.

Usually imports peak in the July to October period as retailers import goods for the Christmas holiday, and then decline sharply and bottom in the Winter depending on the timing of the Chinese New Year. Imports were up 14% YoY in March, and exports were up 8% YoY.

In general, it appears port traffic is returning to the pre-pandemic patterns.

MBA: Mortgage Applications Increased in Weekly Survey

by Calculated Risk on 4/17/2024 07:00:00 AM

From the MBA: Mortgage Applications Increase in Latest MBA Weekly Survey

Mortgage applications increased 3.3 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending April 12, 2024.

The Market Composite Index, a measure of mortgage loan application volume, increased 3.3 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index increased 4 percent compared with the previous week. The Refinance Index increased 0.5 percent from the previous week and was 11 percent higher than the same week one year ago. The seasonally adjusted Purchase Index increased 5 percent from one week earlier. The unadjusted Purchase Index increased 6 percent compared with the previous week and was 10 percent lower than the same week one year ago.

“Rates increased for the second consecutive week, driven by incoming data indicating that the economy remains strong and inflation is proving tougher to bring down. Mortgage rates increased across the board, with the 30-year fixed rate at 7.13 percent – reaching its highest level since December 2023,” said Joel Kan, MBA’s Vice President and Deputy Chief Economist. “Despite these higher rates, application activity picked up, possibly as some borrowers decided to act in case rates continue to rise. Purchase applications drove most of the increase, but remain at low levels of around 10 percent behind last year’s pace. Refinance applications increased very slightly, driven by a 3 percent gain in conventional applications.”

...

The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($766,550 or less) increased to 7.13 percent from 7.01 percent, with points increasing to 0.65 from 0.59 (including the origination fee) for 80 percent loan-to-value ratio (LTV) loans.

emphasis added

Click on graph for larger image.

Click on graph for larger image.The first graph shows the MBA mortgage purchase index.

According to the MBA, purchase activity is down 10% year-over-year unadjusted.

Red is a four-week average (blue is weekly).

Purchase application activity is up slightly from the lows in late October 2023, and below the lowest levels during the housing bust.

The second graph shows the refinance index since 1990.

With higher mortgage rates, the refinance index declined sharply in 2022, and has mostly flat lined since then.

Tuesday, April 16, 2024

Wednesday: Beige Book

by Calculated Risk on 4/16/2024 09:11:00 PM

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

Wednesday:

• At 7:00 AM ET, The Mortgage Bankers Association (MBA) will release the results for the mortgage purchase applications index.

• At 2:00 PM, the Federal Reserve Beige Book, an informal review by the Federal Reserve Banks of current economic conditions in their Districts.

Lawler: Early Read on Existing Home Sales in March

by Calculated Risk on 4/16/2024 03:50:00 PM

Today, in the Calculated Risk Real Estate Newsletter: Lawler: Early Read on Existing Home Sales in March

A brief excerpt:

From housing economist Tom Lawler:Based on publicly-available local realtor/MLS reports released across the country through today, I project that existing home sales as estimated by the National Association of Realtors ran at a seasonally adjusted annual rate of 4.23 million in March, down 3.4% from February’s preliminary pace and down 2.8% from last ’s March’s seasonally adjusted pace. Unadjusted sales should show a larger YOY decline, as there were two fewer business days this March compared to last March.CR Note: The NAR is scheduled to release March existing home sales on Thursday, April 18th. The consensus is for 4.20 million SAAR, down from 4.38 million in February.

Local realtor/MLS reports suggest that the median existing single-family home sales price last month was up by about 6% from last March.

Single Family Starts Up 22% Year-over-year in March; Multi-Family Starts Down Sharply

by Calculated Risk on 4/16/2024 10:17:00 AM

Today, in the Calculated Risk Real Estate Newsletter: Single Family Starts Up 22% Year-over-year in March; Multi-Family Starts Down Sharply

A brief excerpt:

Total housing starts in March were well below expectations, however, starts in January and February were revised up.

The third graph shows the month-to-month comparison for total starts between 2023 (blue) and 2024 (red).

Total starts were down 4.3% in March compared to March 2023.

Starts were down year-over-year (YoY) in March following 4 consecutive months with starts up YoY. The YoY decline is due to the sharp decrease in multi-family starts.

Industrial Production Increased 0.4% in March

by Calculated Risk on 4/16/2024 09:15:00 AM

From the Fed: Industrial Production and Capacity Utilization

Industrial production rose 0.4 percent in March but declined at an annual rate of 1.8 percent in the first quarter. Manufacturing output increased 0.5 percent in March, boosted in part by a gain of 3.1 percent in motor vehicles and parts; factory output excluding motor vehicles and parts moved up 0.3 percent. The index for mining fell 1.4 percent, and the index for utilities gained 2 percent. At 102.7 percent of its 2017 average, total industrial production in March was unchanged compared with its year-earlier level. Capacity utilization moved up to 78.4 percent in March, a rate that is 1.2 percentage points below its long-run (1972–2023) average.

emphasis added

Click on graph for larger image.

Click on graph for larger image.This graph shows Capacity Utilization. This series is up from the record low set in April 2020, and above the level in February 2020 (pre-pandemic).

Capacity utilization at 78.4% is 1.2% below the average from 1972 to 2022. This was below consensus expectations.

Note: y-axis doesn't start at zero to better show the change.

The second graph shows industrial production since 1967.

The second graph shows industrial production since 1967.Industrial production increased to 102.7. This is above the pre-pandemic level.

Industrial production was at consensus expectations.

Housing Starts Decreased to 1.321 million Annual Rate in March

by Calculated Risk on 4/16/2024 08:30:00 AM

From the Census Bureau: Permits, Starts and Completions

Housing Starts:

Privately‐owned housing starts in March were at a seasonally adjusted annual rate of 1,321,000. This is 14.7 percent below the revised February estimate of 1,549,000 and is 4.3 percent below the March 2023 rate of 1,380,000. Single‐family housing starts in March were at a rate of 1,022,000; this is 12.4 percent below the revised February figure of 1,167,000. The March rate for units in buildings with five units or more was 290,000.

Building Permits:

Privately‐owned housing units authorized by building permits in March were at a seasonally adjusted annual rate of 1,458,000. This is 4.3 percent below the revised February rate of 1,523,000, but is 1.5 percent above the March 2023 rate of 1,437,000. Single‐family authorizations in March were at a rate of 973,000; this is 5.7 percent below the revised February figure of 1,032,000. Authorizations of units in buildings with five units or more were at a rate of 433,000 in March.

emphasis added

Click on graph for larger image.

Click on graph for larger image.The first graph shows single and multi-family housing starts since 2000.

Multi-family starts (blue, 2+ units) decreased in March compared to February. Multi-family starts were down 44.3% year-over-year in March.

Single-family starts (red) decreased in March and were up 21.2% year-over-year.

The second graph shows single and multi-family housing starts since 1968.

The second graph shows single and multi-family housing starts since 1968. This shows the huge collapse following the housing bubble, and then the eventual recovery - and the recent collapse and recovery in single-family starts.

Total housing starts in March were well below expectations, however, starts in January and February were revised up.

I'll have more later …

Monday, April 15, 2024

Tuesday: Housing Starts, Industrial Production

by Calculated Risk on 4/15/2024 07:18:00 PM

From Matthew Graham at Mortgage News Daily: After Months of Relative Calm, Rates are Starting to Look Panicked Again

From Matthew Graham at Mortgage News Daily: After Months of Relative Calm, Rates are Starting to Look Panicked Again

In 2023, there were multiple examples of mortgage rates moving up by roughly half a percent in a relatively short amount of time (1-3 weeks). Since the big shift in November, we've only seen one similar example and it was more of a technicality (a sharp drop in rates followed by a correction in early Feb), until today.Tuesday:

...

The culprit was economic data ... this data does not line up with the notion of Fed rate cuts in the near term. It also had an immediate negative impact on the rest of the bond market, including the bonds that most directly dictate mortgage rates.

The average lender is now back into the mid 7s for a top tier, conventional 30yr fixed scenario. [30 year fixed 7.44%]

emphasis added

• At 8:30 AM ET, Housing Starts for March. The consensus is for 1.480 million SAAR, down from 1.521 million SAAR in February.

• At 9:15 AM, The Fed will release Industrial Production and Capacity Utilization for March. The consensus is for a 0.4% increase in Industrial Production, and for Capacity Utilization to increase to 78.5%.

3rd Look at Local Housing Markets in March

by Calculated Risk on 4/15/2024 12:49:00 PM

Today, in the Calculated Risk Real Estate Newsletter: 3rd Look at Local Housing Markets in March

A brief excerpt:

NOTE: The tables for active listings, new listings and closed sales all include a comparison to March 2019 for each local market (some 2019 data is not available).There is much more in the article.

This is the third look at several early reporting local markets in March. I’m tracking about 40 local housing markets in the US. Some of the 40 markets are states, and some are metropolitan areas. I’ll update these tables throughout the month as additional data is released.

Closed sales in March were mostly for contracts signed in January and February when 30-year mortgage rates averaged 6.44% and 6.78%, respectively. This is down from the 7%+ mortgage rates in the August through November period (although rates are now back in the 7%+ range again).

...

And a table of March sales.

In March, sales in these markets were down 9.2% YoY. In February, these same markets were up 2.2% year-over-year Not Seasonally Adjusted (NSA).

Sales in most of these markets are down compared to January 2019.

...

Many more local markets to come!

NAHB: Builder Confidence Unchanged in April

by Calculated Risk on 4/15/2024 10:00:00 AM

The National Association of Home Builders (NAHB) reported the housing market index (HMI) was at 51, unchanged from 51 last month. Any number above 50 indicates that more builders view sales conditions as good than poor.

From the NAHB: Builder Sentiment Unchanged in April

Builder sentiment was flat in April as mortgage rates remained close to 7% over the past month and the latest inflation data failed to show improvement during the first quarter of 2024.

Builder confidence in the market for newly built single-family homes was 51 in April, unchanged from March, according to the National Association of Home Builders (NAHB)/Wells Fargo Housing Market Index (HMI) released today. This breaks a four-month period of gains for the index, which nonetheless remains above the key breakeven point of 50.

“With many frustrated buyers back on the fence waiting for interest rates to fall, policymakers can help ease affordability challenges by reducing inefficient regulatory rules that raise housing costs and limit supply,” said NAHB Chairman Carl Harris, a custom home builder from Wichita, Kan.

“April’s flat reading suggests potential for demand growth is there, but buyers are hesitating until they can better gauge where interest rates are headed,” said NAHB Chief Economist Robert Dietz. “With the markets now adjusting to rates being somewhat higher due to recent inflation readings, we still anticipate the Federal Reserve will announce future rate cuts later this year, and that mortgage rates will moderate in the second half of 2024.”

The April HMI survey also revealed that 22% of builders cut home prices this month, down from 24% in March and 36% in December 2023. However, the average price reduction in April held steady at 6% for the 10th straight month. Meanwhile, the use of sales incentives ticked down to 57% in April from a reading of 60% in March.

...

The HMI index charting current sales conditions in April increased one point to 57 and the component gauging traffic of prospective buyers also edged one point higher to 35. The component measuring sales expectations in the next six months fell two points to 60.

Looking at the three-month moving averages for regional HMI scores, the Northeast increased four points to 63, the Midwest gained five points to 46, the South rose one point to 51 and the West registered a four-point gain to 47.

emphasis added

Click on graph for larger image.

Click on graph for larger image.This graph shows the NAHB index since Jan 1985.

This was at the consensus forecast.