RSS Feed

RSS Feed by Calculated Risk on 5/02/2024 08:30:00 AM

Thursday, May 02, 2024

Weekly Initial Unemployment Claims at 208,000

The DOL reported:

In the week ending April 27, the advance figure for seasonally adjusted initial claims was 208,000, unchanged from the previous week's revised level. The previous week's level was revised up by 1,000 from 207,000 to 208,000. The 4-week moving average was 210,000, a decrease of 3,500 from the previous week's revised average. The previous week's average was revised up by 250 from 213,250 to 213,500.The following graph shows the 4-week moving average of weekly claims since 1971.

emphasis added

Click on graph for larger image.

Click on graph for larger image.The dashed line on the graph is the current 4-week average. The four-week average of weekly unemployment claims decreased to 210,000.

The previous week was revised up.

Weekly claims were lower than the consensus forecast.

Wednesday, May 01, 2024

Thursday: Unemployment Claims, Trade Deficit

by Calculated Risk on 5/01/2024 08:57:00 PM

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

Thursday:

• At 8:30 AM ET, The initial weekly unemployment claims report will be released. The consensus is for 210 thousand initial claims, up from 207 thousand last week.

• Also at 8:30 AM: Trade Balance report for March from the Census Bureau. The consensus is the trade deficit to be $68.8 billion. The U.S. trade deficit was at $68.9 billion in February.

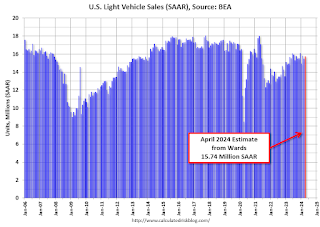

Vehicles Sales Increase to 15.7 million SAAR in April; Up Slightly YoY

by Calculated Risk on 5/01/2024 07:33:00 PM

Wards Auto released their estimate of light vehicle sales for April: U.S. Light-Vehicle Sales Trudge Along with Tepid Growth in April (pay site).

Affordability continued to dominate the sales mix as gains in entry-price CUV and car segments more than offset downturns recorded in most other segments. While the SAAR and the daily selling rate were up, raw volume declined year-over-year due to April 2024 having one fewer selling day than in 2023. Sales in the first four months of 2024 totaled 5.1 million units, up 3% from January-April 2023’s 4.9 million.

Click on graph for larger image.

Click on graph for larger image.This graph shows light vehicle sales since 2006 from the BEA (blue) and Wards Auto's estimate for April (red).

Sales in April (15.74 million SAAR) were up 1.6% from March, and up 0.4% from April 2023.

Sales in April were slightly above the consensus forecast.

Sales in April were slightly above the consensus forecast.

Construction Spending Decreased 0.2% in March

by Calculated Risk on 5/01/2024 02:57:00 PM

From the Census Bureau reported that overall construction spending increased:

Construction spending during March 2024 was estimated at a seasonally adjusted annual rate of $2,083.9 billion, 0.2 percent below the revised February estimate of $2,087.8 billion. The March figure is 9.6 percent above the March 2023 estimate of $1,901.4 billion.Private spending decreased and public spending increased:

emphasis added

Spending on private construction was at a seasonally adjusted annual rate of $1,600.8 billion, 0.5 percent below the revised February estimate of $1,608.5 billion. ...

In March, the estimated seasonally adjusted annual rate of public construction spending was $483.1 billion, 0.8 percent above the revised February estimate of $479.3 billion

Click on graph for larger image.

Click on graph for larger image.This graph shows private residential and nonresidential construction spending, and public spending, since 1993. Note: nominal dollars, not inflation adjusted.

Residential (red) spending is 8.8% below the recent peak in 2022.

Non-residential (blue) spending is 1.1% below the peak two months ago.

Public construction spending is 1.1% below the peak three months ago.

The second graph shows the year-over-year change in construction spending.

The second graph shows the year-over-year change in construction spending.On a year-over-year basis, private residential construction spending is up 4.4%. Non-residential spending is up 11.1% year-over-year. Public spending is up 17.9% year-over-year.

This was below consensus expectations for 0.3% increase in spending, and total construction spending for the previous two months was revised down. This is probably just the start of weakness for private non-residential construction.

FOMC Statement: No Change to Fed Funds Rate, "lack of further progress" on Inflation

by Calculated Risk on 5/01/2024 02:00:00 PM

Recent indicators suggest that economic activity has continued to expand at a solid pace. Job gains have remained strong, and the unemployment rate has remained low. Inflation has eased over the past year but remains elevated. In recent months, there has been a lack of further progress toward the Committee's 2 percent inflation objective.

The Committee seeks to achieve maximum employment and inflation at the rate of 2 percent over the longer run. The Committee judges that the risks to achieving its employment and inflation goals have moved toward better balance over the past year. The economic outlook is uncertain, and the Committee remains highly attentive to inflation risks.

In support of its goals, the Committee decided to maintain the target range for the federal funds rate at 5-1/4 to 5-1/2 percent. In considering any adjustments to the target range for the federal funds rate, the Committee will carefully assess incoming data, the evolving outlook, and the balance of risks. The Committee does not expect it will be appropriate to reduce the target range until it has gained greater confidence that inflation is moving sustainably toward 2 percent. In addition, the Committee will continue reducing its holdings of Treasury securities and agency debt and agency mortgage‑backed securities. Beginning in June, the Committee will slow the pace of decline of its securities holdings by reducing the monthly redemption cap on Treasury securities from $60 billion to $25 billion. The Committee will maintain the monthly redemption cap on agency debt and agency mortgage‑backed securities at $35 billion and will reinvest any principal payments in excess of this cap into Treasury securities. The Committee is strongly committed to returning inflation to its 2 percent objective.

In assessing the appropriate stance of monetary policy, the Committee will continue to monitor the implications of incoming information for the economic outlook. The Committee would be prepared to adjust the stance of monetary policy as appropriate if risks emerge that could impede the attainment of the Committee's goals. The Committee's assessments will take into account a wide range of information, including readings on labor market conditions, inflation pressures and inflation expectations, and financial and international developments.

Voting for the monetary policy action were Jerome H. Powell, Chair; John C. Williams, Vice Chair; Thomas I. Barkin; Michael S. Barr; Raphael W. Bostic; Michelle W. Bowman; Lisa D. Cook; Mary C. Daly; Philip N. Jefferson; Adriana D. Kugler; Loretta J. Mester; and Christopher J. Waller.

emphasis added

Freddie Mac House Price Index Increased in March; Up 6.6% Year-over-year

by Calculated Risk on 5/01/2024 10:11:00 AM

Today, in the Calculated Risk Real Estate Newsletter: Freddie Mac House Price Index Increased in March; Up 6.6% Year-over-year

A brief excerpt:

On a year-over-year basis, the National FMHPI was up 6.6% in March, up from up 6.5% YoY in February. The YoY increase peaked at 19.1% in July 2021, and for this cycle, bottomed at up 0.9% YoY in April 2023. ...

As of March, 11 states and D.C. were below their previous peaks, Seasonally Adjusted. The largest seasonally adjusted declines from the recent peak were in West Virginia (-3.1%), D.C. (-2.9%), North Dakota (-2.0%), and Idaho (-1.0%).

For cities (Core-based Statistical Areas, CBSA), here are the 30 cities with the largest declines from the peak, seasonally adjusted. Austin continues to be the worst performing city.

There is much more in the article.

BLS: Job Openings Decreased to 8.5 million in March

by Calculated Risk on 5/01/2024 10:09:00 AM

From the BLS: Job Openings and Labor Turnover Summary

The number of job openings changed little at 8.5 million on the last business day of March, the U.S. Bureau of Labor Statistics reported today. Over the month, the number of hires changed little at 5.5 million while the number of total separations decreased to 5.2 million. Within separations, quits (3.3 million) and layoffs and discharges (1.5 million) changed little.The following graph shows job openings (black line), hires (dark blue), Layoff, Discharges and other (red column), and Quits (light blue column) from the JOLTS.

emphasis added

This series started in December 2000.

Note: The difference between JOLTS hires and separations is similar to the CES (payroll survey) net jobs headline numbers. This report is for March; the employment report this Friday will be for April.

Click on graph for larger image.

Click on graph for larger image.Note that hires (dark blue) and total separations (red and light blue columns stacked) are usually pretty close each month. This is a measure of labor market turnover. When the blue line is above the two stacked columns, the economy is adding net jobs - when it is below the columns, the economy is losing jobs.

The spike in layoffs and discharges in March 2020 is labeled, but off the chart to better show the usual data.

Jobs openings decreased in March to 8.49 million from 8.81 million in February.

The number of job openings (black) were down 12% year-over-year.

Quits were down 13% year-over-year. These are voluntary separations. (See light blue columns at bottom of graph for trend for "quits").

ISM® Manufacturing index Decreased to 49.2% in April

by Calculated Risk on 5/01/2024 10:00:00 AM

(Posted with permission). The ISM manufacturing index indicated expansion. The PMI® was at 49.2% in April, down from 50.3% in March. The employment index was at 48.6%, up from 47.4% the previous month, and the new orders index was at 49.1%, down from 51.4%.

From ISM: anufacturing PMI® at 49.2%

April 2024 Manufacturing ISM® Report On Business®

Economic activity in the manufacturing sector contracted in April after one month of expansion following 16 consecutive months of contraction, say the nation's supply executives in the latest Manufacturing ISM® Report On Business®.This suggests manufacturing contracted slightly in April. This was below the consensus forecast.

The report was issued today by Timothy R. Fiore, CPSM, C.P.M., Chair of the Institute for Supply Management® (ISM®) Manufacturing Business Survey Committee:

“The Manufacturing PMI® registered 49.2 percent in April, down 1.1 percentage points from the 50.3 percent recorded in March. The overall economy continued in expansion for the 48th month after one month of contraction in April 2020. (A Manufacturing PMI® above 42.5 percent, over a period of time, generally indicates an expansion of the overall economy.) The New Orders Index moved back into contraction territory after one month of expansion, registering 49.1 percent, 2.3 percentage points lower than the 51.4 percent recorded in March. The April reading of the Production Index (51.3 percent) is 3.3 percentage points lower than March’s figure of 54.6 percent. The Prices Index registered 60.9 percent, up 5.1 percentage points compared to the reading of 55.8 percent in March. The Backlog of Orders Index registered 45.4 percent, down 0.9 percentage point compared to the 46.3 percent recorded in March. The Employment Index registered 48.6 percent, up 1.2 percentage points from March’s figure of 47.4 percent.

emphasis added

ADP: Private Employment Increased 192,000 in April

by Calculated Risk on 5/01/2024 08:15:00 AM

Private sector employment increased by 192,000 jobs in April and annual pay was up 5.0 percent year-over-year, according to the April ADP® National Employment ReportTM produced by the ADP Research Institute® in collaboration with the Stanford Digital Economy Lab (“Stanford Lab”). ...This was above the consensus forecast of 180,000. The BLS report will be released Friday, and the consensus is for 210 thousand non-farm payroll jobs added in April.

“Hiring was broad-based in April,” said Nela Richardson, chief economist, ADP. “Only the information sector – telecommunications, media, and information technology – showed weakness, posting job losses and the smallest pace of pay gains since August 2021.”

emphasis added

MBA: Mortgage Applications Decreased in Weekly Survey

by Calculated Risk on 5/01/2024 07:00:00 AM

From the MBA: Mortgage Applications Decrease in Latest MBA Weekly Survey

Mortgage applications decreased 2.3 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending April 26, 2024.

The Market Composite Index, a measure of mortgage loan application volume, decreased 2.3 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 1.4 percent compared with the previous week. The Refinance Index decreased 3 percent from the previous week and was 1 percent lower than the same week one year ago. The seasonally adjusted Purchase Index decreased 2 percent from one week earlier. The unadjusted Purchase Index decreased 1 percent compared with the previous week and was 14 percent lower than the same week one year ago.

“Inflation remains stubbornly high, and this trend is convincing markets that rates, including mortgage rates, are going to stay higher for longer. No doubt, this is a headwind for the housing and mortgage markets, with the 30-year fixed mortgage rate increasing to 7.29 percent last week, the highest level since November 2023,” said Mike Fratantoni, MBA’s SVP and Chief Economist. “Application volume for both purchase and refinances declined over the week and remain well below last year’s pace. One notable trend is that the ARM share has reached its highest level for the year at 7.8 percent. Prospective homebuyers are looking for ways to improve affordability, and switching to an ARM is one means of doing that, with ARM rates in the mid-6 percent range for loans with an initial fixed period of 5 years.”

...

The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($766,550 or less) increased to 7.29 percent from 7.24 percent, with points decreasing to 0.65 from 0.66 (including the origination fee) for 80 percent loan-to-value ratio (LTV) loans.

emphasis added

Click on graph for larger image.

Click on graph for larger image.The first graph shows the MBA mortgage purchase index.

According to the MBA, purchase activity is down 14% year-over-year unadjusted.

Red is a four-week average (blue is weekly).

Purchase application activity is up slightly from the lows in late October 2023, and below the lowest levels during the housing bust.

The second graph shows the refinance index since 1990.

With higher mortgage rates, the refinance index declined sharply in 2022, and has mostly flat lined since then.