RSS Feed

RSS Feed by Calculated Risk on 6/22/2024 08:11:00 AM

Saturday, June 22, 2024

Schedule for Week of June 23, 2024

The key reports this week are May New Home sales, the third estimate of Q1 GDP, Personal Income and Outlays for May and the April Case-Shiller house price index.

For manufacturing, the June Dallas, Kansas City and Richmond Fed manufacturing surveys will be released.

10:30 AM: Dallas Fed Survey of Manufacturing Activity for June.

8:30 AM ET: Chicago Fed National Activity Index for May. This is a composite index of other data.

9:00 AM: S&P/Case-Shiller House Price Index for April.

9:00 AM: S&P/Case-Shiller House Price Index for April.This graph shows the year-over-year change in the seasonally adjusted National Index, Composite 10 and Composite 20 indexes through the most recent report (the Composite 20 was started in January 2000).

The National index was up 6.5% year-over-year in March.

9:00 AM: FHFA House Price Index for April. This was originally a GSE only repeat sales, however there is also an expanded index.

10:00 AM: Richmond Fed Survey of Manufacturing Activity for June.

10:00 AM: State Employment and Unemployment (Monthly) for May 2024.

7:00 AM ET: The Mortgage Bankers Association (MBA) will release the results for the mortgage purchase applications index.

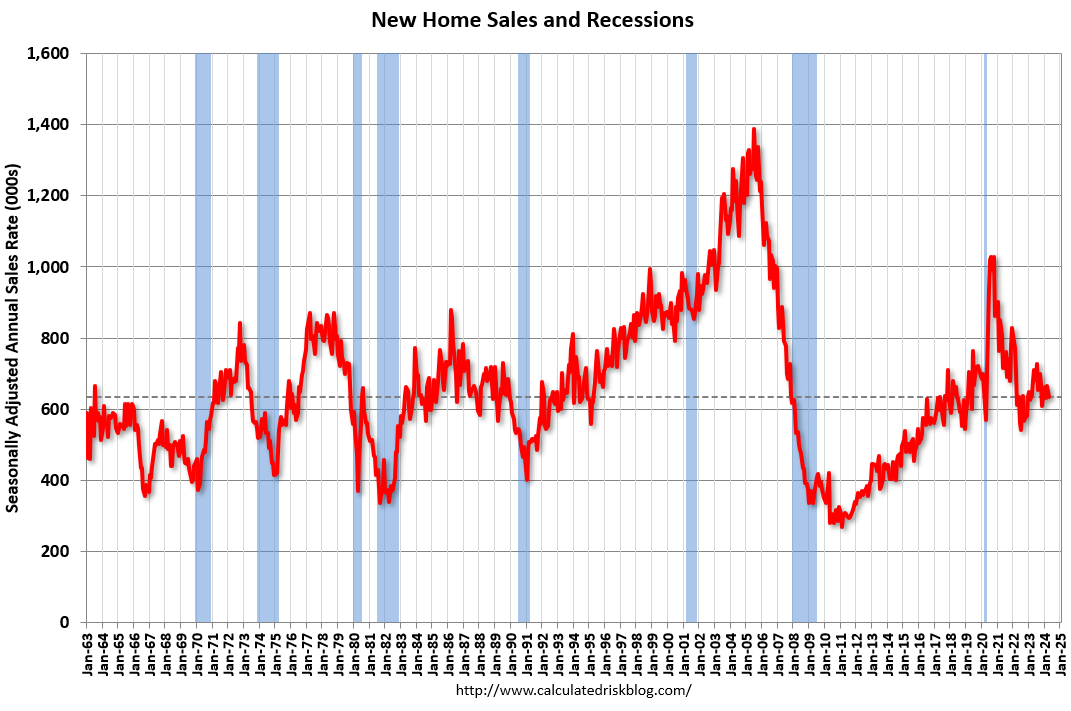

10:00 AM: New Home Sales for May from the Census Bureau.

10:00 AM: New Home Sales for May from the Census Bureau. This graph shows New Home Sales since 1963. The dashed line is the sales rate for last month.

The consensus is for 650 thousand SAAR, up from 634 thousand in April.

During the day: The AIA's Architecture Billings Index for May (a leading indicator for commercial real estate).

8:30 AM: The initial weekly unemployment claims report will be released. The consensus is for 240 thousand initial claims, up from 238 thousand last week.

8:30 AM: Gross Domestic Product, 1st quarter 2024 (Third estimate). The consensus is that real GDP increased 1.3% annualized in Q1, unchanged from the second estimate of a 1.3% increase.

8:30 AM: Durable Goods Orders for May from the Census Bureau. The consensus is for a 0.3% increase in durable goods orders.

10:00 AM: Pending Home Sales Index for May. The consensus is for a 0.3% decrease in the index.

11:00 AM: the Kansas City Fed manufacturing survey for June.

8:30 AM ET: Personal Income and Outlays, May 2024. The consensus is for a 0.4% increase in personal income, and for a 0.3% increase in personal spending.

9:45 AM: Chicago Purchasing Managers Index for June.

10:00 AM: University of Michigan's Consumer sentiment index (Final for June).

Friday, June 21, 2024

June 21st COVID Update: Wastewater Measure Increasing

by Calculated Risk on 6/21/2024 07:02:00 PM

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

For deaths, I'm currently using 4 weeks ago for "now", since the most recent three weeks will be revised significantly.

Note: "Effective May 1, 2024, hospitals are no longer required to report COVID-19 hospital admissions, hospital capacity, or hospital occupancy data." So I'm no longer tracking hospitalizations, however hospitalizations were at a pandemic low three weeks ago.

| COVID Metrics | ||||

|---|---|---|---|---|

| Now | Week Ago | Goal | ||

| Deaths per Week✅ | 316 | 316 | ≤3501 | |

| 1my goals to stop weekly posts, 🚩 Increasing number weekly for Deaths ✅ Goal met. | ||||

Click on graph for larger image.

Click on graph for larger image.This graph shows the weekly (columns) number of deaths reported.

Weekly deaths have declined from the recent peak of 2,561 and are now below the previous pandemic low of 491 last July. This week was at the pandemic low.

This appears to be a leading indicator for COVID hospitalizations and deaths.

This appears to be a leading indicator for COVID hospitalizations and deaths.COVID in wastewater is increasing - especially in the West - and this suggest weekly deaths likely start increasing again.

Q2 GDP Tracking: 1.8% to 3.0%

by Calculated Risk on 6/21/2024 02:36:00 PM

From BofA:

Our 2Q tracking estimate is two tenths higher at 1.8% q/q saar largely due to stronger than expected May payrolls and weaker than expected May CPI and PPI [June 20th estimate]From Goldman:

emphasis added

We lowered our Q2 GDP tracking estimate by 0.1pp to +1.9% (qoq ar) and our Q2 domestic final sales forecast by the same amount to +2.0%. [June 20th estimate]And from the Altanta Fed: GDPNow

The GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the second quarter of 2024 is 3.0 percent on June 20, down from 3.1 percent on June 18. After this morning's housing starts report from the US Census Bureau, the nowcast of second-quarter real gross private domestic investment growth decreased from 8.8 percent to 8.3 percent. [June 18th estimate]

NAR: Existing-Home Sales Decreased to 4.11 million SAAR in May; Median House Prices Increased 5.8% Year-over-Year

by Calculated Risk on 6/21/2024 10:48:00 AM

Today, in the CalculatedRisk Real Estate Newsletter: NAR: Existing-Home Sales Decreased to 4.11 million SAAR in May

Excerpt:

Sales Year-over-Year and Not Seasonally Adjusted (NSA)There is much more in the article.

The fourth graph shows existing home sales by month for 2023 and 2024.

Sales declined 2.8% year-over-year compared to May 2023. This was the thirty-third consecutive month with sales down year-over-year.

NAR: Existing-Home Sales Decreased to 4.11 million SAAR in May

by Calculated Risk on 6/21/2024 10:00:00 AM

From the NAR: Existing-Home Sales Edged Lower by 0.7% in May as Median Sales Price Reached Record High of $419,300

Existing-home sales slightly declined in May as the median sales price climbed to a record high, according to the National Association of REALTORS®. In the four major U.S. regions, sales slid month-over-month in the South but were unchanged in the Northeast, Midwest and West. Year-over-year, sales rose in the Midwest but receded in the Northeast, South and West.

Total existing-home sales – completed transactions that include single-family homes, townhomes, condominiums and co-ops – retreated 0.7% from April to a seasonally adjusted annual rate of 4.11 million in May. Year-over-year, sales waned 2.8% (down from 4.23 million in May 2023).

...

Total housing inventory registered at the end of May was 1.28 million units, up 6.7% from April and 18.5% from one year ago (1.08 million). Unsold inventory sits at a 3.7-month supply at the current sales pace, up from 3.5 months in April and 3.1 months in May 2023.

emphasis added

Click on graph for larger image.

Click on graph for larger image.This graph shows existing home sales, on a Seasonally Adjusted Annual Rate (SAAR) basis since 1994.

Sales in May (4.11 million SAAR) were down 0.7% from the previous month and were 2.8% below the May 2023 sales rate.

The second graph shows nationwide inventory for existing homes.

According to the NAR, inventory increased to 1.28 million in May from 1.20 million the previous month.

According to the NAR, inventory increased to 1.28 million in May from 1.20 million the previous month.

According to the NAR, inventory increased to 1.28 million in May from 1.20 million the previous month.

According to the NAR, inventory increased to 1.28 million in May from 1.20 million the previous month.Headline inventory is not seasonally adjusted, and inventory usually decreases to the seasonal lows in December and January, and peaks in mid-to-late summer.

The last graph shows the year-over-year (YoY) change in reported existing home inventory and months-of-supply. Since inventory is not seasonally adjusted, it really helps to look at the YoY change. Note: Months-of-supply is based on the seasonally adjusted sales and not seasonally adjusted inventory.

Inventory was up 18.5% year-over-year (blue) in May compared to May 2023.

Inventory was up 18.5% year-over-year (blue) in May compared to May 2023.

Months of supply (red) increased to 3.7 months in May from 3.5 months the previous month.

This was close to the consensus forecast. I'll have more later.

The last graph shows the year-over-year (YoY) change in reported existing home inventory and months-of-supply. Since inventory is not seasonally adjusted, it really helps to look at the YoY change. Note: Months-of-supply is based on the seasonally adjusted sales and not seasonally adjusted inventory.

Inventory was up 18.5% year-over-year (blue) in May compared to May 2023.

Inventory was up 18.5% year-over-year (blue) in May compared to May 2023. Months of supply (red) increased to 3.7 months in May from 3.5 months the previous month.

This was close to the consensus forecast. I'll have more later.

Thursday, June 20, 2024

Friday: Existing Home Sales

by Calculated Risk on 6/20/2024 07:51:00 PM

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

Friday:

• At 10:00 AM ET, Existing Home Sales for May from the National Association of Realtors (NAR). The consensus is for 4.10 million SAAR, down from 4.14 million.

Realtor.com Reports Active Inventory Up 36.0% YoY

by Calculated Risk on 6/20/2024 12:45:00 PM

What this means: On a weekly basis, Realtor.com reports the year-over-year change in active inventory and new listings. On a monthly basis, they report total inventory. For April, Realtor.com reported inventory was up 35.2% YoY, but still down almost 34% compared to April 2017 to 2019 levels.

Now - on a weekly basis - inventory is up 36.0% YoY.

Realtor.com has monthly and weekly data on the existing home market. Here is their weekly report: Weekly Housing Trends View—Data for Week Ending June 15, 2024 Here is a graph of the year-over-year change in inventory according to realtor.com.

Here is a graph of the year-over-year change in inventory according to realtor.com.

Inventory was up year-over-year for the 32nd consecutive week.

Realtor.com has monthly and weekly data on the existing home market. Here is their weekly report: Weekly Housing Trends View—Data for Week Ending June 15, 2024

• Active inventory increased, with for-sale homes 36.0% above year-ago levels.

For the 32nd straight week, there were more homes listed for sale versus the prior year, giving homebuyers more options. This past week, the inventory of homes for sale grew by 36.0% compared with last year, maintaining the same rate of growth as the previous week.

• New listings–a measure of sellers putting homes up for sale–were up this week, by 8.0% from one year ago.

Seller activity continued to climb annually last week, matching last week’s annual growth rate of 8%. These past few months sellers have been particularly sensitive to mortgage rates, with newly listed homes being one of the first metrics to respond to the small fluctuations seen in mortgage rates in recent months. If the promising inflation readings seen in May continue, it could lead to softening rates and increase in seller interest toward the latter half of the year. Meanwhile, newly listed homes remained approximately 22% below pre-pandemic (2017 to 2019) levels.

Here is a graph of the year-over-year change in inventory according to realtor.com.

Here is a graph of the year-over-year change in inventory according to realtor.com. Inventory was up year-over-year for the 32nd consecutive week.

However, inventory is still historically low.

New listings remain below typical pre-pandemic levels although up year-over-year.

Single Family Starts Down Slightly Year-over-year in May; Multi-Family Starts Down 50%

by Calculated Risk on 6/20/2024 09:12:00 AM

Today, in the Calculated Risk Real Estate Newsletter: Single Family Starts Down Slightly Year-over-year in May; Multi-Family Starts Down 50%

A brief excerpt:

Total housing starts in May were below expectations, however, starts in March and April were revised up slightly, combined.There is much more in the article.

The third graph shows the month-to-month comparison for total starts between 2023 (blue) and 2024 (red).

Total starts were down 19.3% in May compared to May 2023. Note that starts in May 2023 were very strong, so the year-over-year comparison was difficult.

The YoY decline in total starts was mostly due to the sharp YoY decrease in multi-family starts, although single family starts were down slightly YoY following 10 months of year-over-year increases.

Housing Starts Decreased to 1.277 million Annual Rate in May

by Calculated Risk on 6/20/2024 08:32:00 AM

From the Census Bureau: Permits, Starts and Completions

Housing Starts:

Privately‐owned housing starts in May were at a seasonally adjusted annual rate of 1,277,000. This is 5.5 percent below the revised April estimate of 1,352,000 and is 19.3 percent below the May 2023 rate of 1,583,000. Single‐family housing starts in May were at a rate of 982,000; this is 5.2 percent below the revised April figure of 1,036,000. The May rate for units in buildings with five units or more was 278,000.

Building Permits:

Privately‐owned housing units authorized by building permits in May were at a seasonally adjusted annual rate of 1,386,000. This is 3.8 percent below the revised April rate of 1,440,000 and is 9.5 percent below the May 2023 rate of 1,532,000. Single‐family authorizations in May were at a rate of 949,000; this is 2.9 percent below the revised April figure of 977,000. Authorizations of units in buildings with five units or more were at a rate of 382,000 in May.

emphasis added

Click on graph for larger image.

Click on graph for larger image.The first graph shows single and multi-family housing starts since 2000.

Multi-family starts (blue, 2+ units) decreased in May compared to April. Multi-family starts were down 49.5% year-over-year.

Single-family starts (red) decreased in May and were down 1.7% year-over-year.

The second graph shows single and multi-family housing starts since 1968.

The second graph shows single and multi-family housing starts since 1968. This shows the huge collapse following the housing bubble, and then the eventual recovery - and the recent collapse and recovery in single-family starts.

Total housing starts in May were below expectations, however, starts in March and April were revised up, combined.

I'll have more later …

Weekly Initial Unemployment Claims Decrease to 238,000

by Calculated Risk on 6/20/2024 08:30:00 AM

The DOL reported:

In the week ending June 15, the advance figure for seasonally adjusted initial claims was 238,000, a decrease of 5,000 from the previous week's revised level. The previous week's level was revised up by 1,000 from 242,000 to 243,000. The 4-week moving average was 232,750, an increase of 5,500 from the previous week's revised average. The previous week's average was revised up by 250 from 227,000 to 227,250.The following graph shows the 4-week moving average of weekly claims since 1971.

emphasis added

Click on graph for larger image.

Click on graph for larger image.The dashed line on the graph is the current 4-week average. The four-week average of weekly unemployment claims increased to 232,750.

The previous week was revised up.

Weekly claims were close to the consensus forecast.