RSS Feed

RSS Feed by Calculated Risk on 7/05/2024 08:29:00 PM

Friday, July 05, 2024

July 5th COVID Update: Wastewater Measure Increasing Sharply

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

For deaths, I'm currently using 4 weeks ago for "now", since the most recent three weeks will be revised significantly.

Note: "Effective May 1, 2024, hospitals are no longer required to report COVID-19 hospital admissions, hospital capacity, or hospital occupancy data." So I'm no longer tracking hospitalizations.

| COVID Metrics | ||||

|---|---|---|---|---|

| Now | Week Ago | Goal | ||

| Deaths per Week✅ | 283 | 306 | ≤3501 | |

| 1my goals to stop weekly posts, 🚩 Increasing number weekly for Deaths ✅ Goal met. | ||||

Click on graph for larger image.

Click on graph for larger image.This graph shows the weekly (columns) number of deaths reported.

Weekly deaths have declined from the recent peak of 2,561 and are now below the previous pandemic low of 491 last July. This week was at the pandemic low.

This appears to be a leading indicator for COVID hospitalizations and deaths.

This appears to be a leading indicator for COVID hospitalizations and deaths.COVID in wastewater is increasing - especially in the West and South - and unfortunately this suggest weekly deaths will likely start increasing again.

Realtor.com Reports Active Inventory Up 38.1% YoY

by Calculated Risk on 7/05/2024 01:55:00 PM

What this means: On a weekly basis, Realtor.com reports the year-over-year change in active inventory and new listings. On a monthly basis, they report total inventory. For April, Realtor.com reported inventory was up 35.2% YoY, but still down almost 34% compared to April 2017 to 2019 levels.

Now - on a weekly basis - inventory is up 38.1% YoY.

Realtor.com has monthly and weekly data on the existing home market. Here is their weekly report: Weekly Housing Trends View—Data for Week Ending June 29, 2024 Here is a graph of the year-over-year change in inventory according to realtor.com.

Here is a graph of the year-over-year change in inventory according to realtor.com.

Inventory was up year-over-year for the 34th consecutive week.

Realtor.com has monthly and weekly data on the existing home market. Here is their weekly report: Weekly Housing Trends View—Data for Week Ending June 29, 2024

• Active inventory increased, with for-sale homes 38.1% above year-ago levels

For the 34th week in a row, the number of for-sale homes grew compared with one year ago. This past week, the inventory of homes for sale grew by 38.1% compared with last year, increasing the gap compared with recent weeks and notching the largest annual increase since April 2023.

Despite nearly eight months of building inventory, buyers still see more than 30% fewer homes for sale compared with before the pandemic. Limited home supply has kept upward pressure on home prices, which, combined with still-high mortgage rates, means many buyers remain on the sidelines.

• New listings–a measure of sellers putting homes up for sale–were up this week, by 10.8% from one year ago

Seller activity picked up momentum this week. New listing activity increased annually, climbing by more than in any week back to late April. Recently falling mortgage rates might be encouraging more homeowners to list their homes for sale.

Here is a graph of the year-over-year change in inventory according to realtor.com.

Here is a graph of the year-over-year change in inventory according to realtor.com. Inventory was up year-over-year for the 34th consecutive week.

However, inventory is still historically low.

New listings remain below typical pre-pandemic levels although up year-over-year.

Moody's: Apartment Vacancy Rate Unchanged in Q2; Office Vacancy Rate at New Record High

by Calculated Risk on 7/05/2024 10:52:00 AM

Today, in the Calculated Risk Real Estate Newsletter: Moody's: Apartment Vacancy Rate Unchanged in Q2; Office Vacancy Rate at New Record High

A brief excerpt:

From Moody’s:There is much more in the article.The office sector set a record vacancy rate at 20.1%, breaking the 20% barrier for the first time in history. The slow bleed occurring in the office sector has led to a steady rise in the vacancy rate as permanent shifts in working behavior have outlasted the initial wave of the pandemic four years ago. Q2’s record rate of 20.1% is up from 19.8% the previous quarter and represents the third straight record-breaking quarter beyond our previous historic peaks of 19.3% set in 1986 and 1991.Moody’s Analytics reported that the office vacancy rate was at 20.1% in Q2 2024, up from 19.8% in Q1 2024. This is a new record high, and above the 19.3% during the S&L crisis.

Comments on June Employment Report

by Calculated Risk on 7/05/2024 09:14:00 AM

The headline jobs number in the June employment report was above expectations, however April and May payrolls were revised down by 111,000 combined. The participation rate increased, the employment population ratio was unchanged, and the unemployment rate increased to 4.1%.

Construction employment increased 27 thousand and is now 630 thousand above the pre-pandemic level.

Manufacturing employment decreased 8 thousand and is now 170 thousand above the pre-pandemic level.

Prime (25 to 54 Years Old) Participation

Since the overall participation rate is impacted by both cyclical (recession) and demographic (aging population, younger people staying in school) reasons, here is the employment-population ratio for the key working age group: 25 to 54 years old.

Since the overall participation rate is impacted by both cyclical (recession) and demographic (aging population, younger people staying in school) reasons, here is the employment-population ratio for the key working age group: 25 to 54 years old.The 25 to 54 years old participation rate increased in June to 83.7% from 83.6% in May to the highest level since 2001.

The 25 to 54 employment population ratio was unchanged at 80.8% from 80.8% the previous month.

Both are above pre-pandemic levels and near the highest level this millennium.

Average Hourly Wages

The graph shows the nominal year-over-year change in "Average Hourly Earnings" for all private employees from the Current Employment Statistics (CES).

The graph shows the nominal year-over-year change in "Average Hourly Earnings" for all private employees from the Current Employment Statistics (CES).

Average Hourly Wages

The graph shows the nominal year-over-year change in "Average Hourly Earnings" for all private employees from the Current Employment Statistics (CES).

The graph shows the nominal year-over-year change in "Average Hourly Earnings" for all private employees from the Current Employment Statistics (CES). There was a huge increase at the beginning of the pandemic as lower paid employees were let go, and then the pandemic related spike reversed a year later.

Wage growth has trended down after peaking at 5.9% YoY in March 2022 and was at 3.9% YoY in June.

Wage growth has trended down after peaking at 5.9% YoY in March 2022 and was at 3.9% YoY in June.

Part Time for Economic Reasons

From the BLS report:

From the BLS report:"The number of people employed part time for economic reasons, at 4.2 million, changed little in June. These individuals, who would have preferred full-time employment, were working part time because their hours had been reduced or they were unable to find full-time jobs."The number of persons working part time for economic reasons decreased in June to 4.22 million from 4.42 million in May. This is lower than pre-pandemic levels.

These workers are included in the alternate measure of labor underutilization (U-6) that was unchanged at 7.4% from 7.4% in the previous month. This is down from the record high in April 2020 of 23.0% and up from the lowest level on record (seasonally adjusted) in December 2022 (6.5%). (This series started in 1994). This measure is above the 7.0% level in February 2020 (pre-pandemic).

Unemployed over 26 Weeks

This graph shows the number of workers unemployed for 27 weeks or more.

This graph shows the number of workers unemployed for 27 weeks or more. According to the BLS, there are 1.515 million workers who have been unemployed for more than 26 weeks and still want a job, up from 1.350 million the previous month.

This is down from post-pandemic high of 4.174 million, and up from the recent low of 1.050 million.

This is above pre-pandemic levels.

Job Streak

Summary:

The headline jobs number in the June employment report was above expectations, however, April and May payrolls were revised down by 111,000 combined. The participation rate increased, the employment population ratio was unchanged, and the unemployment rate increased to 4.1%.

This is above pre-pandemic levels.

Job Streak

Through June 2024, the employment report indicated positive job growth for 42 consecutive months, putting the current streak in 5th place of the longest job streaks in US history (since 1939).

| Headline Jobs, Top 10 Streaks | ||

|---|---|---|

| Year Ended | Streak, Months | |

| 1 | 2019 | 100 |

| 2 | 1990 | 48 |

| 3 | 2007 | 46 |

| 4 | 1979 | 45 |

| 5 | 20241 | 42 |

| 6 tie | 1943 | 33 |

| 6 tie | 1986 | 33 |

| 6 tie | 2000 | 33 |

| 9 | 1967 | 29 |

| 10 | 1995 | 25 |

| 1Currrent Streak | ||

Summary:

The headline jobs number in the June employment report was above expectations, however, April and May payrolls were revised down by 111,000 combined. The participation rate increased, the employment population ratio was unchanged, and the unemployment rate increased to 4.1%.

Another decent report, however, the three-month average employment growth has slowed to 177 per month.

June Employment Report: 206 thousand Jobs, 4.1% Unemployment Rate

by Calculated Risk on 7/05/2024 08:30:00 AM

From the BLS: Employment Situation

Total nonfarm payroll employment increased by 206,000 in June, and the unemployment rate changed little at 4.1 percent, the U.S. Bureau of Labor Statistics reported today. Job gains occurred in government, health care, social assistance, and construction.

...

The change in total nonfarm payroll employment for April was revised down by 57,000, from +165,000 to +108,000, and the change for May was revised down by 54,000, from +272,000 to +218,000. With these revisions, employment in April and May combined is 111,000 lower than previously reported.

emphasis added

Click on graph for larger image.

Click on graph for larger image.The first graph shows the jobs added per month since January 2021.

Total payrolls increased by 206 thousand in June. Private payrolls increased by 136 thousand, and public payrolls increased 70 thousand.

Payrolls for April and May were revised down 111 thousand, combined.

Payrolls for April and May were revised down 111 thousand, combined.

The second graph shows the year-over-year change in total non-farm employment since 1968.

The second graph shows the year-over-year change in total non-farm employment since 1968.In June, the year-over-year change was 2.61 million jobs. Employment was up solidly year-over-year.

The third graph shows the employment population ratio and the participation rate.

The Labor Force Participation Rate increased to 62.6% in June, from 62.5% in May. This is the percentage of the working age population in the labor force.

The Labor Force Participation Rate increased to 62.6% in June, from 62.5% in May. This is the percentage of the working age population in the labor force. The Employment-Population ratio was unchanged at 60.1% from 60.2% in May (blue line).

I'll post the 25 to 54 age group employment-population ratio graph later.

The fourth graph shows the unemployment rate.

The fourth graph shows the unemployment rate. The unemployment rate increased to 4.1% in June from 4.0% in May.

This was above consensus expectations; however, April and May payrolls were revised down by 111,000 combined.

Thursday, July 04, 2024

June Employment Preview

by Calculated Risk on 7/04/2024 09:47:00 AM

On Friday at 8:30 AM ET, the BLS will release the employment report for June. The consensus is for 180,000 jobs added, and for the unemployment rate to be unchanged at 4.0%.

There were 272,000 jobs added in May, and the unemployment rate was at 4.0%.

From Goldman Sachs:

Big Data measures ... indicate a soft pace of spring hiring, and we expect an additional drag from residual seasonality in the official payroll figures this Friday. We left our forecast for June nonfarm payroll unchanged at +140k (mom sa).From BofA:

emphasis added

We forecast nonfarm payrolls rose by a solid 200k in June, a 72k decline from the 272k print in May and about 50k lower than the trailing three-month average. ... A slight slowdown in hiring is likely to result in the unemployment rate remaining at 4.0, while wage growth moderates a tenth to 0.3% m/m.• ADP Report: The ADP employment report showed 150,000 private sector jobs were added in June. This was below consensus forecasts and suggests job gains below consensus expectations, however, in general, ADP hasn't been very useful in forecasting the BLS report.

• ISM Surveys: Note that the ISM indexes are diffusion indexes based on the number of firms hiring (not the number of hires). The ISM® manufacturing employment index decreased to 49.3%, down from 51.1% the previous month. This would suggest about 20,000 jobs lost in manufacturing. The ADP report indicated 5,000 manufacturing jobs lost in June.

The ISM® services employment index decreased to 46.1%, from 47.1%. This would suggest 30,000 jobs lost in the service sector. Combined this suggests 50,000 jobs lost in June, far below consensus expectations.

• Unemployment Claims: The weekly claims report showed more initial unemployment claims during the reference week at 239,000 in June compared to 216,000 in May. This suggests more layoffs in June compared to May.

• Conclusion: My guess is employment gains will be below consensus expectations.

Wednesday, July 03, 2024

"Mortgage Rates Move Lower"

by Calculated Risk on 7/03/2024 07:27:00 PM

From Matthew Graham at Mortgage News Daily: Mortgage Rates Move Lower After Weak Service Sector Report

From Matthew Graham at Mortgage News Daily: Mortgage Rates Move Lower After Weak Service Sector Report

"Data dependent" is one of the most common phrases heard from the Federal Reserve these days when it comes to rate-setting policy. And while the Fed doesn't directly dictate mortgage rates, the bond market tends to trade the same data that the Fed cares about.Thursday:

Today's key report, the ISM Services index, isn't quite at the top of the Fed's list, but it's a longstanding market mover when it comes to bonds and, thus, rates. Today's installment was much weaker than expected. Weak data correlates with lower rates, all other things being equal.

Bonds improved immediately after the release. This allowed mortgage lenders to set lower rates today. Some lenders had already published their initial rates for the day and several of them ended up issuing positive reprices before the end of the day.

The bond market is closed tomorrow for the holiday, but will be back to digest an even more important economic report on Friday morning: the big jobs report. [30 year fixed 7.08%]

emphasis added

• All US markets will be closed in observance of Independence Day

Heavy Truck Sales Unchanged in June

by Calculated Risk on 7/03/2024 02:23:00 PM

This graph shows heavy truck sales since 1967 using data from the BEA. The dashed line is the June 2024 seasonally adjusted annual sales rate (SAAR).

Heavy truck sales really collapsed during the great recession, falling to a low of 180 thousand SAAR in May 2009. Then heavy truck sales increased to a new record high of 570 thousand SAAR in April 2019.

Click on graph for larger image.

Click on graph for larger image.

Note: "Heavy trucks - trucks more than 14,000 pounds gross vehicle weight."

Heavy truck sales declined sharply at the beginning of the pandemic, falling to a low of 308 thousand SAAR in May 2020.

Heavy truck sales were at 496 thousand SAAR in June, up slightly from 495 thousand in May, and down 9.6% from 549 thousand SAAR in June 2023.

Usually, heavy truck sales decline sharply prior to a recession. Heavy truck sales are solid.

FOMC Minutes: "Additional favorable data were required to give them greater confidence that inflation" was Moving to Target

by Calculated Risk on 7/03/2024 02:00:00 PM

From the Fed: Minutes of the Federal Open Market Committee June 11–12, 2024. Excerpt:

With regard to the outlook for inflation, participants emphasized that they were strongly committed to their 2 percent objective and that they remained concerned that elevated inflation continued to harm the purchasing power of households, especially those least able to meet the higher costs of essentials like food, housing, and transportation. Participants highlighted a variety of factors that were likely to help contribute to continued disinflation in the period ahead. The factors included continued easing of demand–supply pressures in product and labor markets, lagged effects on wages and prices of past monetary policy tightening, the delayed response of measured shelter prices to rental market developments, or the prospect of additional supply-side improvements. The latter prospect included the possibility of a boost to productivity associated with businesses' deployment of artificial intelligence–related technology. Participants observed that longer-term inflation expectations had remained well anchored and viewed this anchoring as underpinning the disinflation process. Participants affirmed that additional favorable data were required to give them greater confidence that inflation was moving sustainably toward 2 percent.

...

In discussing the outlook for monetary policy, participants noted that progress in reducing inflation had been slower this year than they had expected last December. They emphasized that they did not expect that it would be appropriate to lower the target range for the federal funds rate until additional information had emerged to give them greater confidence that inflation was moving sustainably toward the Committee's 2 percent objective. In discussing their individual outlooks for the target range for the federal funds rate, participants emphasized the importance of conditioning future policy decisions on incoming data, the evolving economic outlook, and the balance of risks. Several participants noted that financial market reactions to data and feedback received from contacts suggested that the Committee's policy approach was generally well understood. Some participants suggested that further clarity about the FOMC's reaction function might be provided by communications that emphasized the Committee's data-dependent approach, with monetary policy decisions being conditional on the evolution of the economy rather than being on a preset path. A couple of participants remarked that providing more information about the Committee's views on the economic outlook and the risks around the outlook would improve the public's understanding of the Committee's decisions.

emphasis added

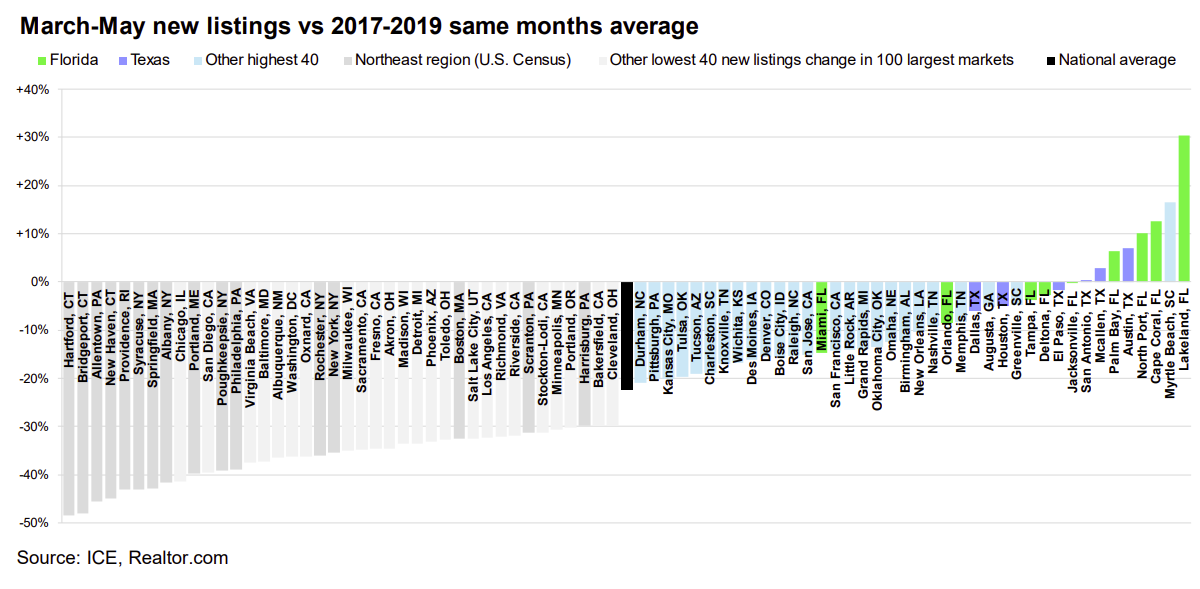

ICE Mortgage Monitor: Existing Home Inventory Surges in Florida and Texas

by Calculated Risk on 7/03/2024 11:50:00 AM

Today, in the Real Estate Newsletter: ICE Mortgage Monitor: Existing Home Inventory Surges in Florida and Texas

Brief excerpt:

The local data I track is indicating that Florida and Texas inventory is above normal, whereas inventory is still low in most of the country.There is much more in the article.

• While the new inflow of listings nationally has averaged a 23% deficit from pre-pandemic levels over the past three months, most Texas and Florida markets are seeing new listing volumes near or above pre-pandemic averages

• In fact, of the 19 markets with new listings volumes within 10% of their 2017-2019 same-month average, 14 are in Texas or Florida, including seven of the nine markets with surpluses