RSS Feed

RSS Feed by Calculated Risk on 7/19/2024 07:59:00 AM

Friday, July 19, 2024

Q2 GDP Tracking: Mid-2%

The advance estimate of 2nd quarter GDP will be released next week.

From BofA:

Our 2Q GDP tracking estimate is up two-tenths to 2.4% q/q saar since our last publication, largely due to higher-than-expected industrial production (IP) and housing starts and permits [July 18th estimate]From Goldman:

emphasis added

We boosted our Q2 GDP tracking estimate by 0.3pp to +2.6% (qoq ar) and our Q2 domestic final sales forecast by 0.1pp to 2.2%. [July 17th estimate]And from the Altanta Fed: GDPNow

The GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the second quarter of 2024 is 2.7 percent on July 17, up from 2.5 percent on July 16. After this morning's housing starts report from the US Census Bureau and industrial production report from the Federal Reserve Board of Governors, the nowcasts of second-quarter real personal consumption expenditures growth and second-quarter real gross private domestic investment growth increased from 2.1 percent and 7.7 percent, respectively, to 2.2 percent and 8.9 percent. [July 17th estimate]

Thursday, July 18, 2024

Hotels: Occupancy Rate Decreased 3.7% Year-over-year

by Calculated Risk on 7/18/2024 03:54:00 PM

The U.S. hotel industry reported higher performance results than the previous week but lower comparisons year over year, according to CoStar’s latest data through 13 July. ...The following graph shows the seasonal pattern for the hotel occupancy rate using the four-week average.

7-13 July 2024 (percentage change from comparable week in 2023):

• Occupancy: 69.2% (-3.7%)

• Average daily rate (ADR): US$158.21 (-1.5%)

• Revenue per available room (RevPAR): US$109.51 (-5.2%)

emphasis added

Click on graph for larger image.

Click on graph for larger image.The red line is for 2024, blue is the median, and dashed light blue is for 2023. Dashed purple is for 2018, the record year for hotel occupancy.

The 4-week average of the occupancy rate is tracking just behind last year and is below the median rate for the period 2000 through 2023 (Blue).

Note: Y-axis doesn't start at zero to better show the seasonal change.

The 4-week average of the occupancy rate will increase seasonally due to summer recreational travel. So far, the summer leisure travel season has disappointed.

Realtor.com Reports Active Inventory Up 35.8% YoY

by Calculated Risk on 7/18/2024 01:41:00 PM

What this means: On a weekly basis, Realtor.com reports the year-over-year change in active inventory and new listings. On a monthly basis, they report total inventory. For June, Realtor.com reported inventory was up 36.7% YoY, but still down 32.4% compared to April 2017 to 2019 levels.

Now - on a weekly basis - inventory is up 35.8% YoY.

Realtor.com has monthly and weekly data on the existing home market. Here is their weekly report: Weekly Housing Trends View—Data for Week Ending July 13, 2024 Here is a graph of the year-over-year change in inventory according to realtor.com.

Here is a graph of the year-over-year change in inventory according to realtor.com.

Inventory was up year-over-year for the 36th consecutive week.

Realtor.com has monthly and weekly data on the existing home market. Here is their weekly report: Weekly Housing Trends View—Data for Week Ending July 13, 2024

• Active inventory increased, with for-sale homes 35.8% above year-ago levels.

For the 36th week in a row, the number of for-sale homes grew compared with one year ago. This past week, the inventory of homes for sale grew by 35.8% compared with last year, slightly higher than the rate observed in the previous week. Despite nearly 8 months of building inventory, buyers still see more than 30% fewer homes for sale compared with pre-pandemic.

• New listings–a measure of sellers putting homes up for sale–were up this week by 8.8% from one year ago.

This week marks 14 out of the past 15 weeks with new listings growth and at 8.8% year-over-year it is slightly above the 2024 weekly average of 8.7%. However, the share of active listings comprising new listings fell from the same last year by just under a percentage point. While newly listed homes increased by 6.3% annually in June, this rate is roughly half of what it was two months ago. Broadly speaking, the number of new homes for sale remains historically low and is still below the 2017-2022 levels, even with recent improvements.

Here is a graph of the year-over-year change in inventory according to realtor.com.

Here is a graph of the year-over-year change in inventory according to realtor.com. Inventory was up year-over-year for the 36th consecutive week.

However, inventory is still historically low.

New listings remain below typical pre-pandemic levels.

LA Port Traffic Increased Year-over-year in June

by Calculated Risk on 7/18/2024 11:15:00 AM

Container traffic gives us an idea about the volume of goods being exported and imported - and usually some hints about the trade report since LA area ports handle about 40% of the nation's container port traffic.

The following graphs are for inbound and outbound traffic at the ports of Los Angeles and Long Beach in TEUs (TEUs: 20-foot equivalent units or 20-foot-long cargo container).

To remove the strong seasonal component for inbound traffic, the first graph shows the rolling 12-month average.

Click on graph for larger image.

Click on graph for larger image.

On a rolling 12-month basis, inbound traffic increased 1.7% in June compared to the rolling 12 months ending in May. Outbound traffic increased 0.7% compared to the rolling 12 months ending the previous month.

The 2nd graph is the monthly data (with a strong seasonal pattern for imports).

Usually imports peak in the July to October period as retailers import goods for the Christmas holiday, and then decline sharply and bottom in the Winter depending on the timing of the Chinese New Year.

Usually imports peak in the July to October period as retailers import goods for the Christmas holiday, and then decline sharply and bottom in the Winter depending on the timing of the Chinese New Year.

Usually imports peak in the July to October period as retailers import goods for the Christmas holiday, and then decline sharply and bottom in the Winter depending on the timing of the Chinese New Year.

Usually imports peak in the July to October period as retailers import goods for the Christmas holiday, and then decline sharply and bottom in the Winter depending on the timing of the Chinese New Year. Imports were up 20% YoY in June, and exports were up 9% YoY.

In general, it appears port traffic is returning to the pre-pandemic patterns.

Weekly Initial Unemployment Claims Increase to 243,000

by Calculated Risk on 7/18/2024 08:30:00 AM

The DOL reported:

In the week ending July 13, the advance figure for seasonally adjusted initial claims was 243,000, an increase of 20,000 from the previous week's revised level. The previous week's level was revised up by 1,000 from 222,000 to 223,000. The 4-week moving average was 234,750, an increase of 1,000 from the previous week's revised average. The previous week's average was revised up by 250 from 233,500 to 233,750.The following graph shows the 4-week moving average of weekly claims since 1971.

emphasis added

Click on graph for larger image.

Click on graph for larger image.The dashed line on the graph is the current 4-week average. The four-week average of weekly unemployment claims increased to 234,750.

The previous week was revised up.

Weekly claims were higher than the consensus forecast.

Wednesday, July 17, 2024

Thursday: Unemployment Claims, Philly Fed Mfg

by Calculated Risk on 7/17/2024 07:31:00 PM

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

Thursday:

• At 8:30 AM ET, The initial weekly unemployment claims report will be released. The consensus is for 228 thousand initial claims, up from 222 thousand last week.

• Also at 8:30 AM, the Philly Fed manufacturing survey for July. The consensus is for a reading of 2.9, up from 1.0.

Fed's Beige Book: "Slight to modest pace of growth"

by Calculated Risk on 7/17/2024 02:00:00 PM

Economic activity maintained a slight to modest pace of growth in a majority of Districts this reporting cycle. However, while seven Districts reported some level of increase in activity, five noted flat or declining activity—three more than in the prior reporting period. Wages continued to grow at a modest to moderate pace in most Districts, while prices were generally reported to have risen modestly. Household spending was little changed this period according to most District banks. Auto sales varied across Districts this cycle, but some Districts noted that sales were lower due in part to a cyberattack on dealerships and high interest rates. Most Districts saw soft demand for consumer and business loans. Reports on residential and commercial real estate markets varied, but most banks reported only slight changes, if any, in recent weeks. Travel and tourism grew steadily and was on par with seasonal expectations. Agricultural conditions varied in tandem with sporadic droughts across the nation. Districts also reported widely disparate trends in manufacturing activity ranging from brisk downturn to moderate growth. Retail restocking spurred slight growth in transportation activity. Meanwhile, tight capacity in ocean shipping led to a surge in spot rates. Expectations for the future of the economy were for slower growth over the next six months due to uncertainty around the upcoming election, domestic policy, geopolitical conflict, and inflation.

Labor Markets

On balance, employment rose at a slight pace in the most recent reporting period. Most Districts reported employment was flat or up slightly, while a few Districts reported modest employment growth. Several Districts reported declines in employment in the manufacturing sector due to slowdowns in new orders. Skilled-worker availability remained a challenge across all Districts; however, several Districts reported some improvement in labor supply conditions. Additionally, labor turnover was lower, which reduced demand to find new workers. Looking ahead, contacts in several Districts expect to be more selective on who they hire and not backfill all open positions. Wages grew at a modest to moderate pace in most Districts. However, several Districts reported some slowing of wage growth due to increased worker availability and less competition for workers.

Prices

Prices increased at a modest pace overall, with a couple Districts noting only slight increases.

emphasis added

Single Family Starts Up Year-over-year in June; Multi-Family Starts Down 23% YoY

by Calculated Risk on 7/17/2024 09:39:00 AM

Today, in the Calculated Risk Real Estate Newsletter: Single Family Starts Up Year-over-year in June; Multi-Family Starts Down 23% YoY

A brief excerpt:

Total housing starts in June were above expectations and starts in April and May were revised up.There is much more in the article.

The third graph shows the month-to-month comparison for total starts between 2023 (blue) and 2024 (red).

Total starts were down 4.4% in June compared to June 2023.

The YoY decline in total starts was due to the sharp YoY decrease in multi-family starts. Single family starts have been up YoY for 12 consecutive months.

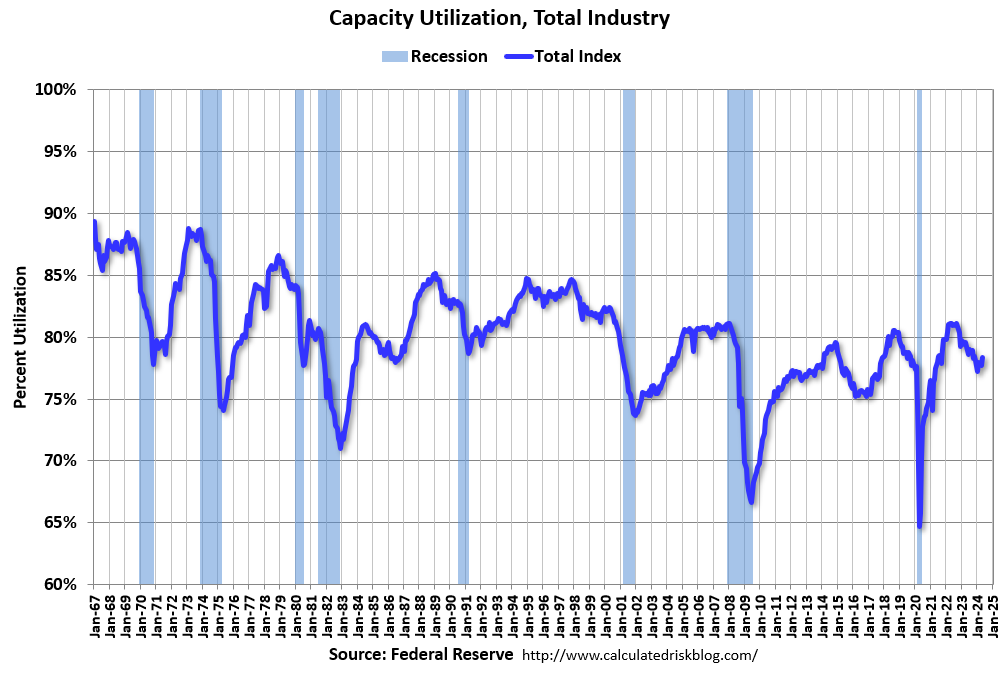

Industrial Production Increased 0.6% in June

by Calculated Risk on 7/17/2024 09:15:00 AM

From the Fed: Industrial Production and Capacity Utilization

Industrial production rose 0.6 percent in June after advancing 0.9 percent in May. For the second quarter as a whole, industrial production increased at an annual rate of 4.3 percent. Manufacturing output moved up 0.4 percent in June and rose 3.4 percent (annual rate) in the second quarter. In June, the indexes for mining and utilities posted gains of 0.3 percent and 2.8 percent, respectively. At 104 percent of its 2017 average, total industrial production in June was 1.6 percent above its year-earlier level. Capacity utilization moved up to 78.8 percent in June, a rate that is 0.9 percentage point below its long-run (1972–2023) average.

emphasis added

Click on graph for larger image.

Click on graph for larger image.This graph shows Capacity Utilization. This series is up from the record low set in April 2020, and above the level in February 2020 (pre-pandemic).

Capacity utilization at 78.8% is 0.9% below the average from 1972 to 2022. This was above consensus expectations.

Note: y-axis doesn't start at zero to better show the change.

The second graph shows industrial production since 1967.

The second graph shows industrial production since 1967.Industrial production increased to 104.0. This is above the pre-pandemic level.

Industrial production was above consensus expectations.

Housing Starts Increased to 1.353 million Annual Rate in June

by Calculated Risk on 7/17/2024 08:30:00 AM

From the Census Bureau: Permits, Starts and Completions

Housing Starts:

Privately-owned housing starts in June were at a seasonally adjusted annual rate of 1,353,000. This is 3.0 percent above the revised May estimate of 1,314,000, but is 4.4 percent below the June 2023 rate of 1,415,000. Single-family housing starts in June were at a rate of 980,000; this is 2.2 percent below the revised May figure of 1,002,000. The June rate for units in buildings with five units or more was 360,000.

Building Permits:

Privately-owned housing units authorized by building permits in June were at a seasonally adjusted annual rate of 1,446,000. This is 3.4 percent above the revised May rate of 1,399,000, but is 3.1 percent below the June 2023 rate of 1,493,000. Single-family authorizations in June were at a rate of 934,000; this is 2.3 percent below the revised May figure of 956,000. Authorizations of units in buildings with five units or more were at a rate of 460,000 in June.

emphasis added

Click on graph for larger image.

Click on graph for larger image.The first graph shows single and multi-family housing starts since 2000.

Multi-family starts (blue, 2+ units) increased in June compared to May. Multi-family starts were down 23.1% year-over-year.

Single-family starts (red) decreased in June and were up 5.4% year-over-year.

The second graph shows single and multi-family housing starts since 1968.

The second graph shows single and multi-family housing starts since 1968. This shows the huge collapse following the housing bubble, and then the eventual recovery - and the recent collapse and recovery in single-family starts.

Total housing starts in June were above expectations, and starts in April and May were revised up.

I'll have more later …