RSS Feed

RSS Feed by Calculated Risk on 9/24/2024 09:00:00 AM

Tuesday, September 24, 2024

Case-Shiller: National House Price Index Up 5.0% year-over-year in July

S&P/Case-Shiller released the monthly Home Price Indices for July ("July" is a 3-month average of May, June and July closing prices).

This release includes prices for 20 individual cities, two composite indices (for 10 cities and 20 cities) and the monthly National index.

From S&P S&P CoreLogic Case-Shiller Index All-Time Highs Continue in July 2024

The S&P CoreLogic Case-Shiller U.S. National Home Price NSA Index, covering all nine U.S. census divisions, reported a 5.0% annual gain for July, down from a 5.5% annual gain in the previous month. The 10-City Composite saw an annual increase of 6.8%, down from a 7.4% annual increase in the previous month. The 20-City Composite posted a year-over-year increase of 5.9%, dropping from a 6.5% increase in the previous month. New York again reported the highest annual gain among the 20 cities with an 8.8% increase in July, followed by Las Vegas and Los Angeles with annual increases of 8.2% and 7.2%, respectively. Portland held the lowest rank for the smallest year-over-year growth, notching the same 0.8% annual increase in July as last month.

...

The U.S. National Index, the 20-City Composite, and the 10-City Composite upward trends continued to decelerate from last month, with pre-seasonality adjustment increases of 0.1% for the national index, and both the 20-City and 10-City Composites remained unchanged on the month.

After seasonal adjustment, the U.S. National Index posted a month-over-month increase of 0.2%, while both the 20-City and 10-City Composite reported a monthly rise of 0.3%.

“Accounting for seasonality of home purchases, we have witnessed 14 consecutive record highs in our National Index,” says Brian D. Luke, CFA, Head of Commodities, Real & Digital Assets. “While the S&P 500 has achieved 39 record highs and the S&P GSCI Gold TR hit 35 record highs, housing is following a similar trajectory. The growth has come at a cost, with all but two markets decelerating last month, eight markets seeing monthly declines, and the slowest annual growth nationally in 2024. Overall, the indices continue to grow at a rate that exceeds long-run averages after accounting for inflation.

“We continue to observe outperformance in most low-price tiers in the market on a three- and five-year horizon,” Luke continued. “The low-price tier of Tampa was the best performing market nationally with five-year performance of 88%. The New York market was the best market annually, posting a gain of 8.9%. New York’s low-tier index, which include home values up to $533,000, helped drive that growth with 10.8% annual gains. Over five years, markets such as New York and Atlanta saw low-price-tiered indices outperforming their market by as much as 20% and 18%, respectively. The relative outperformance of low-price-tiered indices has both benefited first-time homebuyers as well as made it more difficult for those looking for a starter home. The opposite is happening in California, which has the most expensive high-price tiers in the nation, all well over $1 million. The rich are getting richer in San Diego, Los Angeles, and San Francisco where their high-price-tiered indices outperformed on a one- and three-year basis. ”

emphasis added

Click on graph for larger image.

Click on graph for larger image. The first graph shows the nominal seasonally adjusted Composite 10, Composite 20 and National indices (the Composite 20 was started in January 2000).

The Composite 10 index was up 0.3% in July (SA). The Composite 20 index was up 0.3% (SA) in July.

The National index was up 0.2% (SA) in July.

The second graph shows the year-over-year change in all three indices.

The second graph shows the year-over-year change in all three indices.The Composite 10 SA was up 6.8% year-over-year. The Composite 20 SA was up 5.9% year-over-year.

The National index SA was up 5.0% year-over-year.

Annual price changes were close to expectations. I'll have more later.

Monday, September 23, 2024

Tuesday: Case-Shiller House Prices, Richmond Fed Mfg

by Calculated Risk on 9/23/2024 06:59:00 PM

From Matthew Graham at Mortgage News Daily: Mortgage Rates Move Slightly Higher to Start New Week

From Matthew Graham at Mortgage News Daily: Mortgage Rates Move Slightly Higher to Start New Week

Mortgage rates rose modestly last week after hitting long term lows before the Fed announced its 0.50% rate cut. In not so many words, mortgage rates had already gotten in position for that cut and were thus left to undergo a mild correction. [30 year fixed 6.20%]Tuesday:

emphasis added

• At 9:00 AM ET, S&P/Case-Shiller House Price Index for July. The consensus is for a 5.9% year-over-year increase in the Composite 20 index for July.

• At 9:00 AM, FHFA House Price Index for July. This was originally a GSE only repeat sales, however there is also an expanded index.

• At 10:00 AM, the Richmond Fed manufacturing survey for September.

MBA Survey: Share of Mortgage Loans in Forbearance Increases to 0.31% in August

by Calculated Risk on 9/23/2024 04:10:00 PM

From the MBA: Share of Mortgage Loans in Forbearance Increases to 0.31% in August

The Mortgage Bankers Association’s (MBA) monthly Loan Monitoring Survey revealed that the total number of loans now in forbearance increased to 0.31% as of August 31, 2024. According to MBA’s estimate, 155,000 homeowners are in forbearance plans. Mortgage servicers have provided forbearance to approximately 8.2 million borrowers since March 2020.At the end of August, there were about 155,000 homeowners in forbearance plans.

The share of Fannie Mae and Freddie Mac loans in forbearance increased 1 basis point to 0.13% in August 2024. Ginnie Mae loans in forbearance increased by 10 basis points to 0.66%, and the forbearance share for portfolio loans and private-label securities (PLS) increased 2 basis points to 0.35%.

“For the third consecutive month, the percentage of loans in forbearance increased across all loan types,” said Marina Walsh, CMB, MBA’s Vice President of Industry Analysis. “By investor type, Ginnie Mae loans in forbearance have increased the most – up 27 basis points since May 2024.”

Added Walsh, “Forbearance levels are much lower than they were during the first two years of the pandemic. However, a weakening in the performance of servicing portfolios and an increase in forbearance requests are both likely given the softening observed in the labor market.”

emphasis added

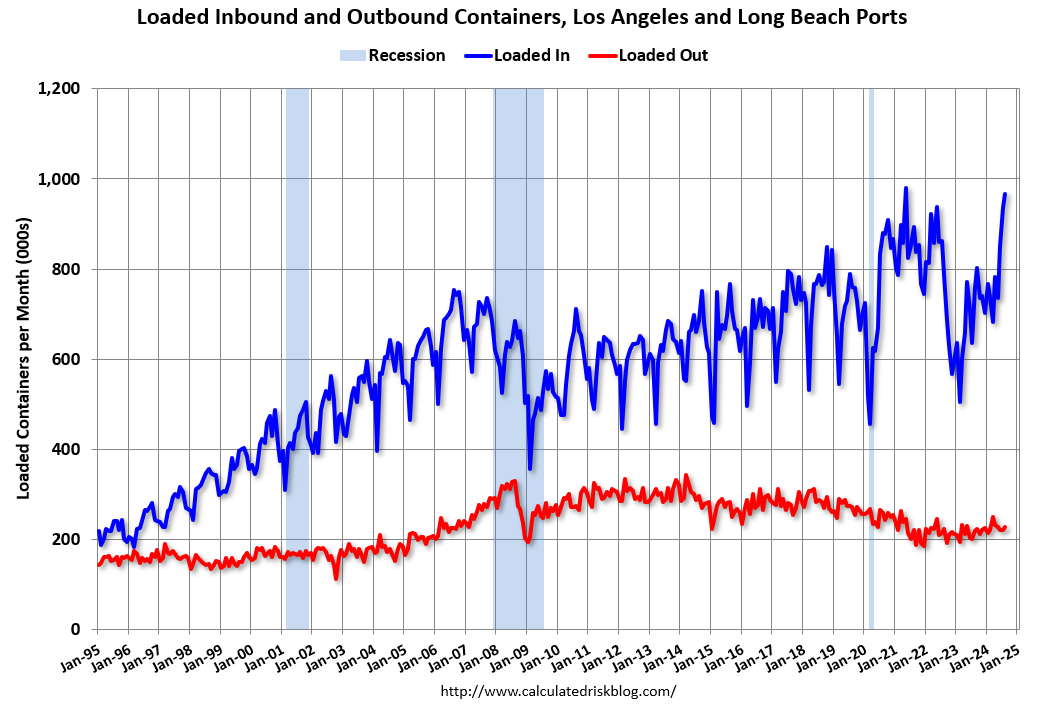

LA Ports: Inbound Traffic Increased Sharply Year-over-year in August

by Calculated Risk on 9/23/2024 02:05:00 PM

Container traffic gives us an idea about the volume of goods being exported and imported - and usually some hints about the trade report since LA area ports handle about 40% of the nation's container port traffic.

The following graphs are for inbound and outbound traffic at the ports of Los Angeles and Long Beach in TEUs (TEUs: 20-foot equivalent units or 20-foot-long cargo container).

To remove the strong seasonal component for inbound traffic, the first graph shows the rolling 12-month average.

Click on graph for larger image.

Click on graph for larger image.

On a rolling 12-month basis, inbound traffic increased 2.2% in August compared to the rolling 12 months ending in July. Outbound traffic increased 0.3% compared to the rolling 12 months ending the previous month.

The 2nd graph is the monthly data (with a strong seasonal pattern for imports).

Usually imports peak in the July to October period as retailers import goods for the Christmas holiday, and then decline sharply and bottom in the Winter depending on the timing of the Chinese New Year.

Usually imports peak in the July to October period as retailers import goods for the Christmas holiday, and then decline sharply and bottom in the Winter depending on the timing of the Chinese New Year.

Usually imports peak in the July to October period as retailers import goods for the Christmas holiday, and then decline sharply and bottom in the Winter depending on the timing of the Chinese New Year.

Usually imports peak in the July to October period as retailers import goods for the Christmas holiday, and then decline sharply and bottom in the Winter depending on the timing of the Chinese New Year. Imports were up 27% YoY in August, and exports were up 4% YoY.

In general, it appears port traffic is returning to the pre-pandemic patterns - although this was a very strong August for imports as retailers prepare for holiday shopping - and possibly to beat any increase in tariffs or the potential strike.

Watch Months-of-Supply!

by Calculated Risk on 9/23/2024 11:01:00 AM

Today, in the Calculated Risk Real Estate Newsletter: Watch Months-of-Supply!

A brief excerpt:

Both inventory and sales are well below pre-pandemic levels, and I think we need to keep an eye on months-of-supply to forecast price changes. Historically nominal prices declined when months-of-supply approached 6 months - and that is unlikely any time soon - however, as expected, months-of-supply is back to 2019 levels.There is much more in the article.

Months-of-supply was at 4.2 months in August compared to 4.0 months in August 2019. Even though inventory has declined significantly compared to 2019, sales have fallen even more - pushing up months-of-supply.

The following graph shows months-of-supply since 2017. Note that months-of-supply is higher than the last 3 years (2021 - 2023), and above August 2019. Months-of-supply was at 4.2 in August 2017 and 4.3 in August 2018. In 2020 (black), months-of-supply increased at the beginning of the pandemic and then declined sharply.

...

What would it take to get months-of-supply above 5 months? If sales stay depressed at 2023 and 2024 levels, how much would inventory have to increase to put months-of-supply at 5 months by, say, June 2024?

Housing Sept 23rd Weekly Update: Inventory up 1.6% Week-over-week, Up 37.2% Year-over-year

by Calculated Risk on 9/23/2024 08:11:00 AM

Altos reports that active single-family inventory was up 1.6% week-over-week. Inventory is now up 46.8% from the February seasonal bottom.

Click on graph for larger image.

Click on graph for larger image.This inventory graph is courtesy of Altos Research.

As of September 20th, inventory was at 725 thousand (7-day average), compared to 714 thousand the prior week.

This is the highest level of inventory since May 2020.

The second graph shows the seasonal pattern for active single-family inventory since 2015.

The red line is for 2024. The black line is for 2019.

Inventory was up 37.2% compared to the same week in 2023 (last week it was up 37.4%), and down 24.0% compared to the same week in 2019 (last week it was down 25.2%).

Back in June 2023, inventory was down almost 54% compared to 2019, so the gap to more normal inventory levels is slowly closing.

Mike Simonsen discusses this data regularly on Youtube.

Sunday, September 22, 2024

Sunday Night Futures

by Calculated Risk on 9/22/2024 07:55:00 PM

Weekend:

• Schedule for Week of September 22, 2024

Monday:

• At 8:30 AM ET, Chicago Fed National Activity Index for August. This is a composite index of other data.

From CNBC: Pre-Market Data and Bloomberg futures S&P 500 and DOW futures are mostly unchanged (fair value).

Oil prices were up over the last week with WTI futures at $71.01 per barrel and Brent at $74.50 per barrel. A year ago, WTI was at $90, and Brent was at $94 - so WTI oil prices are down about 20% year-over-year.

Here is a graph from Gasbuddy.com for nationwide gasoline prices. Nationally prices are at $3.16 per gallon. A year ago, prices were at $3.84 per gallon, so gasoline prices are down $0.68 year-over-year.

The Top Ten Job Streaks: Current Streak is in 5th Place

by Calculated Risk on 9/22/2024 08:22:00 AM

For fun:

Through August 2024, the employment report indicated positive job growth for 44 consecutive months, putting the current streak in 5th place of the longest job streaks in US history (since 1939).

It appears this streak will survive the annual benchmark revision (that will revise down job growth).

Trivia: The only presidential term that saw job growth every month was President Obama's 2nd term.

Although job growth has slowed recently, we might see job growth every month during the current term.

| Headline Jobs, Top 10 Streaks | ||

|---|---|---|

| Year Ended | Streak, Months | |

| 1 | 2019 | 100 |

| 2 | 1990 | 48 |

| 3 | 2007 | 46 |

| 4 | 1979 | 45 |

| 5 | 20241 | 44 |

| 6 tie | 1943 | 33 |

| 6 tie | 1986 | 33 |

| 6 tie | 2000 | 33 |

| 9 | 1967 | 29 |

| 10 | 1995 | 25 |

| 1Currrent Streak | ||

Saturday, September 21, 2024

Real Estate Newsletter Articles this Week: Existing-Home Sales Decreased to 3.86 million SAAR in August

by Calculated Risk on 9/21/2024 02:11:00 PM

At the Calculated Risk Real Estate Newsletter this week:

Click on graph for larger image.

Click on graph for larger image.

• NAR: Existing-Home Sales Decreased to 3.86 million SAAR in August

• Housing Starts Increased to 1.356 million Annual Rate in August

• Part 2: Current State of the Housing Market; Overview for mid-September 2024

• Q2 Update: Delinquencies, Foreclosures and REO

• Lawler: Early Read on Existing Home Sales in August

This is usually published 4 to 6 times a week and provides more in-depth analysis of the housing market.

Schedule for Week of September 22, 2024

by Calculated Risk on 9/21/2024 08:11:00 AM

The key reports this week are August New Home sales, the third estimate of Q2 GDP, Personal Income and Outlays for August, and Case-Shiller house prices for July.

For manufacturing, the Richmond and Kansas City Fed manufacturing surveys will be released this week.

8:30 AM ET: Chicago Fed National Activity Index for August. This is a composite index of other data.

9:00 AM: S&P/Case-Shiller House Price Index for July.

9:00 AM: S&P/Case-Shiller House Price Index for July.This graph shows the year-over-year change in the seasonally adjusted National Index, Composite 10 and Composite 20 indexes through the most recent report (the Composite 20 was started in January 2000).

The consensus is for a 5.9% year-over-year increase in the Composite 20 index for July.

9:00 AM: FHFA House Price Index for July. This was originally a GSE only repeat sales, however there is also an expanded index.

10:00 AM: the Richmond Fed manufacturing survey for September.

7:00 AM ET: The Mortgage Bankers Association (MBA) will release the results for the mortgage purchase applications index.

10:00 AM: New Home Sales for August from the Census Bureau.

10:00 AM: New Home Sales for August from the Census Bureau. This graph shows New Home Sales since 1963. The dashed line is the sales rate for last month.

The consensus is for 700 thousand SAAR, down from 739 thousand in July.

8:30 AM: The initial weekly unemployment claims report will be released. The consensus is for 226 thousand initial claims, up from 219 thousand last week.

8:30 AM: Gross Domestic Product, 2nd Quarter 2024 (Third Estimate), and Corporate Profits (Revised) The consensus is that real GDP increased 3.0% annualized in Q2, unchanged from the second estimate of 3.0%.

8:30 AM: Durable Goods Orders for August from the Census Bureau. The consensus is for a 2.8% decrease in durable goods orders.

9:20 AM: Speech, Fed Chair Jerome Powell, Opening Remarks (via pre-recorded video), At the 2024 U.S. Treasury Market Conference, Federal Reserve Bank of New York, New York, N.Y.

10:00 AM: Pending Home Sales Index for August. The consensus is 3.1% increase in the index.

11:00 AM: the Kansas City Fed manufacturing survey for September.

8:30 AM: Personal Income and Outlays, August 2024. The consensus is for a 0.4% increase in personal income, and for a 0.3% increase in personal spending. And for the Core PCE price index to increase 0.2%.

10:00 AM: University of Michigan's Consumer sentiment index (Final for September). The consensus is for a reading of 67.7.