RSS Feed

RSS Feed by Calculated Risk on 9/29/2024 07:08:00 PM

Sunday, September 29, 2024

Sunday Night Futures

Weekend:

• Schedule for Week of September 29, 2024

Monday:

• At 9:45 AM ET, Chicago Purchasing Managers Index for September. The consensus is for a reading of 46.5, up from 46.1 in August.

• At 10:30 AM, Dallas Fed Survey of Manufacturing Activity for September.

• At 1:55 PM, Speech, Fed Chair Jerome Powell, Economic Outlook, At the National Association for Business Economics (NABE) Annual Meeting, Nashville, Tenn

From CNBC: Pre-Market Data and Bloomberg futures S&P 500 and DOW futures are mostly unchanged (fair value).

Oil prices were down over the last week with WTI futures at $68.01 per barrel and Brent at $71.86 per barrel. A year ago, WTI was at $91, and Brent was at $96 - so WTI oil prices are down about 25% year-over-year.

Here is a graph from Gasbuddy.com for nationwide gasoline prices. Nationally prices are at $3.18 per gallon. A year ago, prices were at $3.82 per gallon, so gasoline prices are down $0.64 year-over-year.

Realtor.com Reports Active Inventory Up 33.2% YoY

by Calculated Risk on 9/29/2024 01:23:00 PM

What this means: On a weekly basis, Realtor.com reports the year-over-year change in active inventory and new listings. On a monthly basis, they report total inventory. For August, Realtor.com reported inventory was up 5.8% YoY, but still down 26.4% compared to the 2017 to 2019 same month levels.

Now - on a weekly basis - inventory is up 33.2% YoY.

Realtor.com has monthly and weekly data on the existing home market. Here is their weekly report: Weekly Housing Trends View—Data for Week Ending Sept. 21, 2024 Here is a graph of the year-over-year change in inventory according to realtor.com.

Here is a graph of the year-over-year change in inventory according to realtor.com.

Inventory was up year-over-year for the 46th consecutive week.

Realtor.com has monthly and weekly data on the existing home market. Here is their weekly report: Weekly Housing Trends View—Data for Week Ending Sept. 21, 2024

• Active inventory increased, with for-sale homes 33.2% above year-ago levels.

For the 46th consecutive week dating back to November 2023, the number of listings for sale has grown year-over-year, and this week continues a string of growth rates in the mid-30% range that started in April. There were more homes for sale this week than in any week since January 2020, pre-pandemic. Much of the inventory build up is due to more seller activity than buyer activity, but falling mortgage rates could mean more buyers enter the market in the coming weeks.

• New listings–a measure of sellers putting homes up for sale- jumped 8.0% this week compared to one year ago.

As the recent easing of mortgage rates kept encouraging many sellers to return to the market, the year-over-year growth in new listings continued this week. With mortgage rates at their lowest level in nearly two years, eager sellers are taking the chance to get their home listed, hoping to catch some of the fall buyer activity. This trend is expected to continue as rates ease further and more sellers are ‘unlocked’.

Here is a graph of the year-over-year change in inventory according to realtor.com.

Here is a graph of the year-over-year change in inventory according to realtor.com. Inventory was up year-over-year for the 46th consecutive week.

However, inventory is still historically low.

New listings remain below typical pre-pandemic levels.

Saturday, September 28, 2024

Real Estate Newsletter Articles this Week: Case-Shiller National HPI Up 5.0% year-over-year in July

by Calculated Risk on 9/28/2024 02:11:00 PM

At the Calculated Risk Real Estate Newsletter this week:

Click on graph for larger image.

Click on graph for larger image.

• Case-Shiller: National House Price Index Up 5.0% year-over-year in July

• New Home Sales Decrease to 716,000 Annual Rate in August

• Inflation Adjusted House Prices 1.5% Below 2022 Peak

• Fannie and Freddie: Single Family Serious Delinquency Rate Ticked Up in August

• Watch Months-of-Supply!

This is usually published 4 to 6 times a week and provides more in-depth analysis of the housing market.

Schedule for Week of September 29, 2024

by Calculated Risk on 9/28/2024 08:11:00 AM

The key report scheduled for this week is the September employment report on Friday.

Other key indicators include the September ISM Manufacturing and Services indices and September auto sales.

10:30 AM: Dallas Fed Survey of Manufacturing Activity for September.

9:45 AM: Chicago Purchasing Managers Index for September. The consensus is for a reading of 46.5, up from 46.1 in August.

1:55 PM: Speech, Fed Chair Jerome Powell, Economic Outlook, At the National Association for Business Economics (NABE) Annual Meeting, Nashville, Tenn

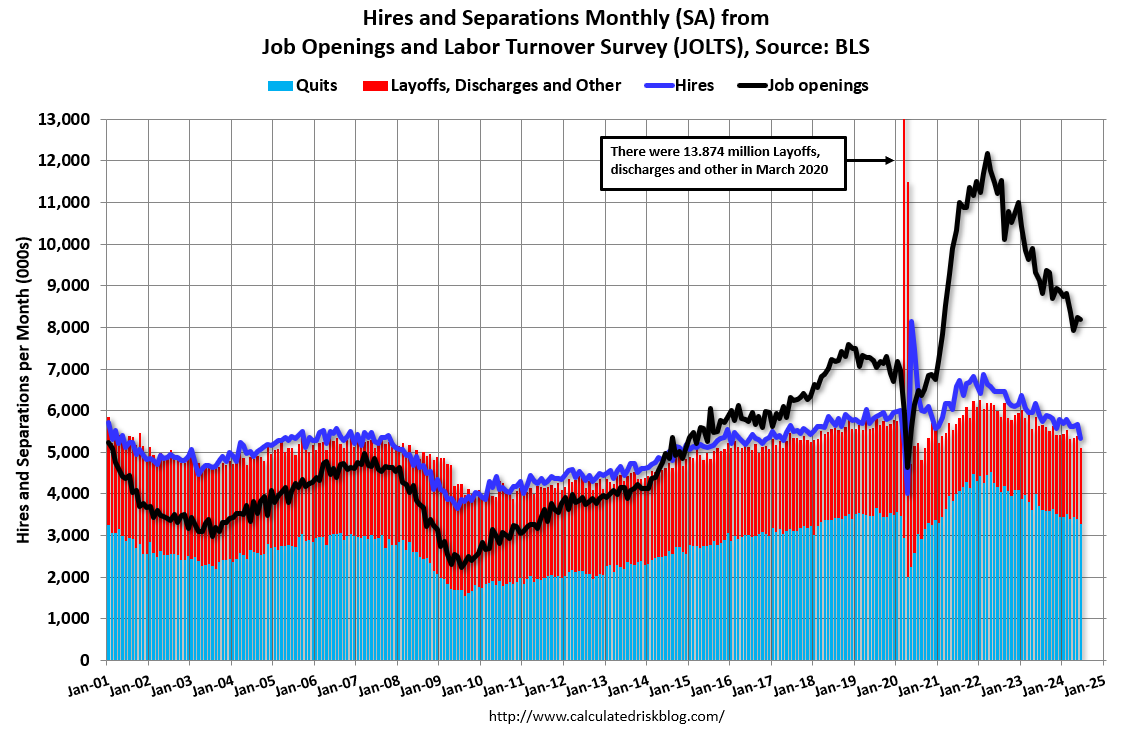

10:00 AM: Job Openings and Labor Turnover Survey for August from the BLS.

10:00 AM: Job Openings and Labor Turnover Survey for August from the BLS. This graph shows job openings (black line), hires (purple), Layoff, Discharges and other (red column), and Quits (light blue column) from the JOLTS.

10:00 AM: ISM Manufacturing Index for September. The consensus is for a reading of 47.6, up from 47.2 in August.

10:00 AM: Construction Spending for August. The consensus is for a 0.1% increase.

All day: Light vehicle sales for September.

All day: Light vehicle sales for September.The consensus is for sales of 15.7 million SAAR, up from 15.1 million SAAR in August (Seasonally Adjusted Annual Rate).

This graph shows light vehicle sales since the BEA started keeping data in 1967. The dashed line is the current sales rate.

7:00 AM ET: The Mortgage Bankers Association (MBA) will release the results for the mortgage purchase applications index.

8:15 AM: The ADP Employment Report for September. This report is for private payrolls only (no government). The consensus is for 110,000 jobs added, up from 99,000 in August.

8:30 AM: The initial weekly unemployment claims report will be released. The consensus is for 224 thousand initial claims, up from 218 thousand last week.

10:00 AM: the ISM Services Index for September.

8:30 AM: Employment Report for September. The consensus is for 145,000 jobs added, and for the unemployment rate to be unchanged at 4.2%.

8:30 AM: Employment Report for September. The consensus is for 145,000 jobs added, and for the unemployment rate to be unchanged at 4.2%.There were 142,000 jobs added in August, and the unemployment rate was at 4.2%.

This graph shows the jobs added per month since January 2021.

Friday, September 27, 2024

September 27th COVID Update: Wastewater Measure Declining

by Calculated Risk on 9/27/2024 07:20:00 PM

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

For deaths, I'm currently using 4 weeks ago for "now", since the most recent three weeks will be revised significantly.

Note: "Effective May 1, 2024, hospitals are no longer required to report COVID-19 hospital admissions, hospital capacity, or hospital occupancy data." So I'm no longer tracking hospitalizations.

| COVID Metrics | ||||

|---|---|---|---|---|

| Now | Week Ago | Goal | ||

| Deaths per Week🚩 | 1,239 | 1,176 | ≤3501 | |

| 1my goals to stop weekly posts, 🚩 Increasing number weekly for Deaths ✅ Goal met. | ||||

Click on graph for larger image.

Click on graph for larger image.This graph shows the weekly (columns) number of deaths reported.

Although weekly deaths met the original goal to stop posting, I'm going to continue to post now that deaths are above the goal again.

Weekly deaths are quadruple the low of 302 in early June.

This appears to be a leading indicator for COVID hospitalizations and deaths.

This appears to be a leading indicator for COVID hospitalizations and deaths.COVID in wastewater is now declining suggesting weekly deaths will start declining soon.

Fannie and Freddie: Single Family Serious Delinquency Rate Ticked Up in August

by Calculated Risk on 9/27/2024 05:32:00 PM

Today, in the Calculated Risk Real Estate Newsletter: Fannie and Freddie: Single Family Serious Delinquency Rate Ticked Up in August

Brief excerpt:

Single-family serious delinquencies increased slightly in August, and multi-family serious delinquencies decreased slightly.

...

Freddie Mac reports that the multi-family delinquencies rate decreased to 0.38% in August, down from 0.39% in July, and down from the recent peak of 0.44% in January.

This graph shows the Freddie multi-family serious delinquency rate since 2012. Rates were still high in 2012 following the housing bust and financial crisis.

The multi-family rate increased following the pandemic and has increased recently as rent growth slowed, vacancy rates increased and borrowing costs increased sharply. The rate surged higher in January and has moved mostly sideways at an elevated level since then.

There is much more in the article.

ICE: "Home prices continued to cool in August, with prices up +3.0%" YoY

by Calculated Risk on 9/27/2024 11:46:00 AM

Note: This is a repeat sales index (like Case-Shiller and FHFA). ICE is releasing this index early this month.

Several cities in Florida are now seeing year-over-year price declines (as inventory surges).

From ICE:

From ICE:

• Home prices continued to cool in August, with prices up +3.0% from the same time last year according to the ICE Home Price Index, marking the slowest rate of home price growth in over a year

• On an adjusted basis prices rose by +0.12% in the month – the slowest adjusted monthly growth since last November – equivalent to a seasonally adjusted annualized rate (SAAR) of +1.4%

• While those soft monthly gains suggest that the annual home price growth rate may slow further in September, the market may be poised to catch a two different tail winds in coming months

• The first will come from softer comparable sales from late 2023 when mortgage rates had climbed above 7.5%, with the second coming from easing 30-year rates and improved affordability in September

• August home price gains were driven by mortgage rates in the high 6% range in July, before they trended sharply lower through August and September

• September home prices were driven by rates in the mid-6% range, while October prices will be driven by 30-year rates that have been in the low 6% range

• It will be worth watching the housing supply/demand and price dynamics closely in coming months given the sharp downward trend in mortgage rates in recent weeks Price growth slowed across two-thirds of the nation’s largest markets in August

• The strongest cooling was seen in the Midwest and Northeast – areas of the country that, while slightly cooler than recent months, continue to see the strongest home price growth nationwide

• On the other end of the spectrum, 1 in 4 of the nation’s largest markets saw prices edge lower on a seasonally adjusted basis, led by North Port, Cape Coral, Austin TX, Memphis, Tucson, and Atlanta

• A dozen major markets are now seeing home prices below last year’s levels, including Cape Coral and North Port where prices are down 6.4% and 5.7%, respectively, from this same time last year

• Of the 12 markets where prices have fallen over the past 12 months, 7 are in the state of Florida along with San Francisco, Austin, San Antonio, Memphis, and New Orleans

emphasis added

Q3 GDP Tracking: Around 3%

by Calculated Risk on 9/27/2024 10:50:00 AM

From BofA:

Since our last weekly publication, our 3Q GDP tracking estimate is down two-tenths to 2.3% q/q saar while 2Q GDP came in at 3.0% q/q saar in the final official estimate. [Sept 27th estimate]From Goldman:

emphasis added

The details of yesterday’s durable goods report and this morning’s Advance Economic Indicators report were stronger than our previous GDP tracking assumptions, while the details of the PCE report were slightly softer. On net, we boosted our Q3 GDP tracking estimate by 0.2pp to +3.2% (quarter-over-quarter annualized). Our Q3 domestic final sales estimate stands at +2.8%. [Sept 27th estimate]And from the Atlanta Fed: GDPNow

The GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the third quarter of 2024 is 3.1 percent on September 27, up from 2.9 percent on September 18. After recent releases from the US Census Bureau, the US Bureau of Economic Analysis, and the National Association of Realtors, a decline in the nowcast of real personal consumption expenditures growth was more than offset by increases in the nowcasts of real gross private domestic investment growth and the contribution of net exports to third-quarter real GDP growth. [Sept 27th estimate]

PCE Measure of Shelter Increases to 5.3% YoY in August

by Calculated Risk on 9/27/2024 09:15:00 AM

Here is a graph of the year-over-year change in shelter from the CPI report and housing from the PCE report this morning, both through August 2024.

CPI Shelter was up 5.2% year-over-year in August, up from 5.0 in July, and down from the cycle peak of 8.2% in March 2023.

CPI Shelter was up 5.2% year-over-year in August, up from 5.0 in July, and down from the cycle peak of 8.2% in March 2023.

Housing (PCE) was up 5.3% YoY in August, up from 5.2% in July, and down from the cycle peak of 8.3% in April 2023.

Since asking rents are mostly flat year-over-year, these measures will slowly continue to decline over the next year.

Since asking rents are mostly flat year-over-year, these measures will slowly continue to decline over the next year.

The second graph shows PCE prices, Core PCE prices and Core ex-housing over the last 3 months (annualized):

The second graph shows PCE prices, Core PCE prices and Core ex-housing over the last 3 months (annualized):Key measures are slightly below the Fed's target on a 3-month basis. Note: There appears to be some residual seasonality distorting PCE prices in Q1, especially in January.

3-month annualized change:

PCE Price Index: 1.5%

Core PCE Prices: 2.1%

Core minus Housing: 1.5%

Core PCE Prices: 2.1%

Core minus Housing: 1.5%

Personal Income increased 0.2% in August; Spending increased 0.2%

by Calculated Risk on 9/27/2024 08:30:00 AM

The BEA released the Personal Income and Outlays report for August:

Personal income increased $50.5 billion (0.2 percent at a monthly rate) in August, according to estimates released today by the U.S. Bureau of Economic Analysis. Disposable personal income (DPI), personal income less personal current taxes, increased $34.2 billion (0.2 percent) and personal consumption expenditures (PCE) increased $47.2 billion (0.2 percent).The August PCE price index increased 2.2 percent year-over-year (YoY), down from 2.5 percent YoY in July, and down from the recent peak of 7.2 percent in June 2022.

The PCE price index increased 0.1 percent. Excluding food and energy, the PCE price index increased 0.1 percent. Real DPI increased 0.1 percent in August and real PCE increased 0.1 percent; goods increased less than 0.1 percent and services increased 0.2 percent.

emphasis added

The PCE price index, excluding food and energy, increased 2.7 percent YoY, up from 2.6 percent in July, and down from the recent peak of 5.6 percent in February 2022.

The following graph shows real Personal Consumption Expenditures (PCE) through August 2024 (2017 dollars). Note that the y-axis doesn't start at zero to better show the change.

Click on graph for larger image.

Click on graph for larger image.

The dashed red lines are the quarterly levels for real PCE.

Personal income was above expectations, and PCE was below expectations.

The following graph shows real Personal Consumption Expenditures (PCE) through August 2024 (2017 dollars). Note that the y-axis doesn't start at zero to better show the change.

Click on graph for larger image.

Click on graph for larger image.The dashed red lines are the quarterly levels for real PCE.

Personal income was above expectations, and PCE was below expectations.

Inflation was below expectations.

Using the two-month method to estimate Q3 real PCE growth, real PCE was increasing at a 3.3% annual rate in Q3 2024. (Using the mid-month method, real PCE was increasing at 2.6%). This suggests solid PCE growth in Q3.