RSS Feed

RSS Feed by Calculated Risk on 1/22/2025 07:00:00 AM

Wednesday, January 22, 2025

MBA: Mortgage Applications Increased in Weekly Survey

From the MBA: Mortgage Applications Increase in Latest MBA Weekly Survey

Mortgage applications increased 0.1 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending January 17, 2025.

The Market Composite Index, a measure of mortgage loan application volume, increased 0.1 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index increased 3 percent compared with the previous week. The Refinance Index decreased 3 percent from the previous week and was 42 percent higher than the same week one year ago. The seasonally adjusted Purchase Index increased 1 percent from one week earlier. The unadjusted Purchase Index increased 7 percent compared with the previous week and was 2 percent higher than the same week one year ago.

“Mortgage application volume was little changed last week, but there was a small increase in conventional purchase volume, which brought the level of total purchase volume up almost 2 percent above last year at this time,” said Mike Fratantoni, MBA’s SVP and Chief Economist. “Mortgage rates remained near 7 percent, a key psychological level, which likely continues to slow the pace of activity for both refinances and purchases. Incoming economic data are likely to keep the Federal Reserve on hold for now, while uncertainties about economic policy are likely to keep longer-term rates, including mortgage rates, steady at these levels.”

...

The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($766,550 or less) decreased to 7.02 percent from 7.09 percent, with points decreasing to 0.62 from 0.65 (including the origination fee) for 80 percent loan-to-value ratio (LTV) loans. The effective rate decreased from last week.

emphasis added

Click on graph for larger image.

Click on graph for larger image.The first graph shows the MBA mortgage purchase index.

According to the MBA, purchase activity is up 2% year-over-year unadjusted.

Red is a four-week average (blue is weekly).

Purchase application activity is up about 30% from the lows in late October 2023 and is now 8% above the lowest levels during the housing bust.

The second graph shows the refinance index since 1990.

The refinance index is very low.

Tuesday, January 21, 2025

Wednesday: Architecture Billings Index

by Calculated Risk on 1/21/2025 07:24:00 PM

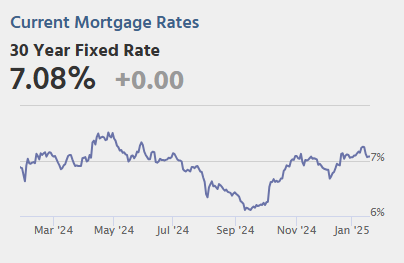

From Matthew Graham at Mortgage News Daily: Mortgage Rates Unimpacted by New Executive Orders

From Matthew Graham at Mortgage News Daily: Mortgage Rates Unimpacted by New Executive Orders

Bonds were thus able to hold onto the gains from last week with some additional improvement today. The average mortgage lender wasn't eager to adjust rates, however, with the top tier 30yr fixed rate remaining unchanged from last Friday. [30 year fixed 7.08%]Wednesday:

emphasis added

• At 7:00 AM ET: The Mortgage Bankers Association (MBA) will release the mortgage purchase applications index.

During the day: The AIA's Architecture Billings Index for December (a leading indicator for commercial real estate).

MBA Survey: Share of Mortgage Loans in Forbearance Decreases to 0.47% in December

by Calculated Risk on 1/21/2025 01:14:00 PM

From the MBA: Share of Mortgage Loans in Forbearance Decreases Slightly to 0.47% in December

The Mortgage Bankers Association’s (MBA) monthly Loan Monitoring Survey revealed that the total number of loans now in forbearance decreased by 3 basis points from 0.50% of servicers’ portfolio volume in the prior month to 0.47% as of December 31, 2024. According to MBA’s estimate, 235,000 homeowners are in forbearance plans. Mortgage servicers have provided forbearance to approximately 8.5 million borrowers since March 2020.

The share of Fannie Mae and Freddie Mac loans in forbearance decreased 2 basis points to 0.19% in December 2024. Ginnie Mae loans in forbearance decreased by 4 basis points to 1.07%, and the forbearance share for portfolio loans and private-label securities (PLS) decreased 2 basis points to 0.40%.

“The overall mortgage forbearance rate decreased slightly in December as some borrowers got back on track following last fall’s severe weather in the Southeast,” said Marina Walsh, CMB, MBA’s Vice President of Industry Analysis. “Even with the slight decrease, the level of forbearance is higher than it was six months ago across all loan types and the performance of servicing portfolios and loan workouts has weakened.”

Added Walsh, “At year end, almost 43% of borrowers in forbearance were there due to a natural disaster. Given the disruption and devastation caused by the California wildfires, that share will likely move higher in the months ahead, as homeowners turn to forbearance to allow time to navigate their recovery process.”

emphasis added

Click on graph for larger image.

Click on graph for larger image.By reason, 54.5% of borrowers are in forbearance for reasons such as a temporary hardship caused by job loss, death, divorce, or disability. Another 42.8% are in forbearance because of a natural disaster. Less than 2.7% of borrowers are still in forbearance because of COVID-19.At the end of December, there were about 235,000 homeowners in forbearance plans.

Benchmarking the U.S. economy

by Calculated Risk on 1/21/2025 01:07:00 PM

Presidents receive too much credit and blame for the economy!

But it worth looking at the current state of the economy. From economist Ernie Tedeschi: Benchmarking the U.S. economy that President Donald Trump is set to inherit

• While the U.S. economy still has challenges, especially lingering inflation and poor consumer sentiment, many important economic metrics are outperforming the 2008 cycle (the most recent nonpandemic business cycle and the cycle in which the first Trump administration began), and some are even at historical highs.

• Some measures have already met goals set by the incoming administration, even before Inauguration Day. Real Gross Domestic Product growth, for example, has averaged 3 percent over the past two years.

• Expectations are for output growth to moderate to trend next year, inflation to take roughly two years to fully return to the Federal Reserve’s 2 percent target, and the unemployment rate to remain roughly at current levels.

• Economic forecasts even one year or two years out are highly uncertain.

...

Broadly speaking, the data indicate that the U.S. economy in the later part of 2024 was in a strong position. Growth in output, measured by real GDP, and nonfarm productivity were above estimates of trend, employment levels were at near-historic highs, and real wage and income growth was positive. Though inflation was not yet fully back to the Federal Reserve’s inflation target of 2 percent, it was generally thought to be in the “last mile,” or the phase when inflation declines tend to slow as inflation approaches 2 percent. The risk of inflation reaccelerating, however, remains a concern. And some measures of labor market momentum, such as quits and hires, softened in recent quarters off of their prior strong reads.

Table 1 below summarizes recent U.S. economic data and contrasts it with the performance over the 2008–2019 business cycle, which includes the Great Recession of 2007–2009 and the subsequent recovery prior to the onset of the COVID-19 recession in 2020. Numbers in blue are metrics that outperformed the average over the entire previous business cycle, while numbers in purple indicate metrics that outperformed the second half of the previous cycle, from 2014 to 2019, when the Great Recession recovery accelerated. (See Table 1.)

Click on graph for larger image.

Click on graph for larger image.NOTE: I broke the table in two to make it more readable.

As a caveat, economic aggregates are, by their nature, summary statistics that do not represent all lived experiences. Indeed, by definition, half of people are above and below the median. No one economic measure or set of measures perfectly encapsulates all the positives and negatives of the U.S. economy. With that said, were one to compare U.S. outcomes in 2025 and 2026 to those coming out of 2024, Table 1 gives a sense of what the most prominent metrics look like at the end of President Biden’s term in office.

3rd Look at Local Housing Markets in December

by Calculated Risk on 1/21/2025 09:24:00 AM

Today, in the Calculated Risk Real Estate Newsletter: 3rd Look at Local Housing Markets in December

A brief excerpt:

The NAR is scheduled to release December Existing Home sales on Friday, January 24th at 10:00 AM. The consensus is for 4.20 million SAAR, up from 4.15 million in November. Last year, the NAR reported sales in December 2023 at 3.88 million SAAR. This will be the third consecutive month with a year-over-year increase following YoY declines every month since July 2021.There is much more in the article.

Housing economist Tom Lawler expects the NAR to report sales of 4.15 million SAAR for December.

...

Here is a look at months-of-supply using NSA sales. Since this is NSA data, it is likely this will be the seasonal low for months-of-supply.

Note the regional differences with more months-of-supply in the South, especially in Florida and Texas.

...

More local markets to come!

Monday, January 20, 2025

Monday Night Futures

by Calculated Risk on 1/20/2025 06:29:00 PM

Tuesday:

• No major economic releases scheduled.

From CNBC: Pre-Market Data and Bloomberg futures S&P 500 are up 32 and DOW futures are up 225 (fair value).

1.73 million Total Housing Completions in 2024 including Manufactured Homes; Most Since 2006

by Calculated Risk on 1/20/2025 02:04:00 PM

Today, in the Calculated Risk Real Estate Newsletter: 1.73 million Total Housing Completions in 2024 including Manufactured Homes; Most Since 2006

A brief excerpt:

Although total housing starts decreased 3.9% in 2024 compared to 2023, completions increased sharply year-over-year. There were 1.731 million total completions and placements in 2024, up 12.5% compared to 2023, and the most since 2006.There is much more in the article.

Not counting Manufactured homes, there are 1.628 million completions in 2024, up 12.4% from 1.449 million in 2023, and also the most since 2006.

...

The housing start report last week indicated 1,020.4 thousand single family completions in 2024 (red), up 2.2% from 998.8 thousand in 2023. There were 16.8 thousand completions of 2-to-4 units, and 590.6 thousand completions of 5+ units (blue), up 35% from 2023, and the most since 1974!

AAR: Rail Carloads Down YoY in 2024, Intermodal Up

by Calculated Risk on 1/20/2025 11:17:00 AM

From the Association of American Railroads (AAR) Rail Time Indicators. Graphs and excerpts reprinted with permission.

For the full year 2024, total U.S. carloads were 11.34 million, down 2.9% (343,156 carloads) from 2023 and down 2.3% (265,491 carloads) from 2022. ... Carloads excluding coal, on the other hand, rose in 2024 — up 1.4%, or 117,264 carloads, over 2023 and their third year-over-year gain in the past four years.

U.S. railroads originated 13.84 million containers and trailers in 2024, the most since 2021; the third most ever (behind 2018 and 2021); and up 9.3% (1.17 million units) over 2023.

emphasis added

Click on graph for larger image.

Click on graph for larger image.This graph from the Rail Time Indicators report shows the six-week average for carloads for the last 3 years. Total carloads were down 2.0% in Q4 YoY.

Total originated carloads on U.S. railroads in the fourth quarter of 2024 fell 2.0%, or 57,285 carloads, from the fourth quarter of 2023. Total carloads fell year-over-year each quarter in 2024 after rising (albeit modestly) in three of the four quarters of 2023. Total carloads averaged 220,336 per week in Q4 2024. In our records that begin in 1988, only 2020 had a lower fourth-quarter weekly average.

And on Intermodal:

And on Intermodal:In Q4 2024, intermodal averaged 279,275 units per week, up 8.8% over Q4 2023 and the most ever for a fourth quarter in our records. (Q3 2018 and Q2 2021 were higher among all quarters.) Container volume averaged 269,460 per week in Q4 2024, up 10.0% over Q4 2023 and the most ever for any quarter.Note: rail traffic was weak even before the pandemic. As AAR noted: "Trade tensions and declining mfrg. output lead to lower rail volumes" in 2019. These factors might impact rail traffic again in 2025.

Housing Jan 20th Weekly Update: Inventory Up 1.2% Week-over-week, Up 24.8% Year-over-year

by Calculated Risk on 1/20/2025 08:11:00 AM

Altos reports that active single-family inventory was up 1.2% week-over-week.

Inventory always declines seasonally in the Winter and usually bottoms in late January or February. If the previous week was the seasonal bottom, that would be very early in the year, but that has happened before.

The first graph shows the seasonal pattern for active single-family inventory since 2015.

Click on graph for larger image.

Click on graph for larger image.The red line is for 2024. The black line is for 2019.

Inventory was up 24.8% compared to the same week in 2024 (last week it was up 23.6%), and down 23.4% compared to the same week in 2019 (last week it was down 23.3%).

Back in June 2023, inventory was down almost 54% compared to 2019, so the gap to more normal inventory levels has closed significantly!

This second inventory graph is courtesy of Altos Research.

This second inventory graph is courtesy of Altos Research.

As of Jan 17th, inventory was at 632 thousand (7-day average), compared to 624 thousand the prior week.

Mike Simonsen discusses this data regularly on Youtube

Sunday, January 19, 2025

Sunday Night: Markets Closed in observance of Martin Luther King Jr. Day

by Calculated Risk on 1/19/2025 07:16:00 PM

Weekend:

• Schedule for Week of January 19, 2025

Monday:

• All US markets will be closed in observance of Martin Luther King Jr. Day

Oil prices were up over the last week with WTI futures at $77.88 per barrel and Brent at $80.79 per barrel. A year ago, WTI was at $74, and Brent was at $81 - so WTI oil prices are up about 5% year-over-year.

Here is a graph from Gasbuddy.com for nationwide gasoline prices. Nationally prices are at $3.11 per gallon. A year ago, prices were at $3.10 per gallon, so gasoline prices are mostly unchanged year-over-year.