RSS Feed

RSS Feed by Calculated Risk on 12/30/2005 02:51:00 PM

Friday, December 30, 2005

Broken Promises

One of my predictions for top economic stories for 2006 concerned problems with pension plans. From the LA Times today: How Bedrock Promises Of Security Have Fractured Across America

...That's when Delphi Chief Executive Robert S. "Steve" Miller, citing global competition and crippling "legacy costs," ushered the $28.6 billion-a-year company into one of the largest industrial bankruptcies in U.S. history. In short order, Miller called for slashing workers' compensation by almost two-thirds, threatened to void the company's union contracts, and hinted broadly that he would follow the playbook he had used elsewhere of pushing responsibility for paying the firm's pensions to the federal government and dumping its retiree health benefits altogether.An excellent article. I was once the trustee of a retirement plan and I will write about my experiences in the new year.

Although Delphi has since backed off a bit — it says it's willing to negotiate with its unions and its former parent and largest customer, General Motors Corp. — the parts firm has left little doubt that its ultimate aim remains steep reductions in wages, benefits and retiree costs.

Delphi is at the cutting edge of a crisis that's engulfing the U.S. auto industry, much as it did steel and airlines. Its actions are adding to a gathering trend, a shift of economic risks once largely borne by business and government to the backs of working families.

Before the trouble is over, some believe, a corporate icon such as Ford Motor Co. or GM could be swept from the American landscape. So too could much of what remains of the already frayed relationship between millions of working people and their employers.

"When the history of this period is written, Delphi will be viewed as the tipping point where the auto industry either got its act together or failed," said David E. Cole, the son of a former GM president and head of the Center for Automotive Research, based in Ann Arbor, Mich. "The spillover to the rest of the economy is going to be tremendous."

Thursday, December 29, 2005

Snow: Raise Debt Limit

by Calculated Risk on 12/29/2005 06:47:00 PM

Reuters reports: Snow urges Congress to raise debt limit U.S. Treasury Secretary

John Snow warned lawmakers on Thursday that a legally set limit on the government's ability to borrow will be hit in mid-February and urged Congress to raise it quickly.

...

"The administration now projects that the statutory debt limit, currently $8.184 trillion, will be reached in mid-February 2006," Snow said in a letter to 21 members of the U.S. House of Representatives and Senate released by Treasury after financial markets had closed.

...

The debt limit was last raised in November 2004 by $800 billion to its current level. The letter to Congress does not specify an amount the Treasury wants the ceiling set at this time.

...

Treasury officials had said in November it was bracing for hefty borrowing needs in the January-March quarter, likely around a record $171 billion, and that it likely would hit the debt limit in that period.

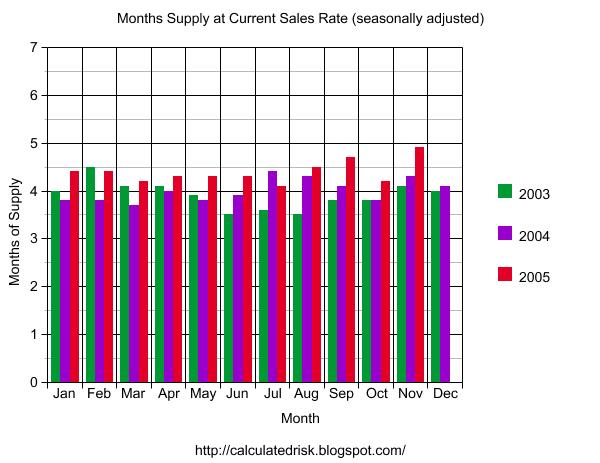

Existing Homes: Sales Fall, Inventory Increases

by Calculated Risk on 12/29/2005 11:23:00 AM

The National Association of Realtors (NAR) reports: Existing-Home Sales Trend Lower in November

Total existing-home sales – including single-family, townhomes, condominiums and co-ops – eased 1.7 percent to a seasonally adjusted annual rate of 6.97 million units in November from a pace of 7.09 million in October. Sales were 0.1 percent below the 6.98 million-unit level in November 2004.Inventories increased to a 5 month supply:

Total housing inventory levels rose 1.2 percent at the end of November to 2.90 million existing homes available for sale, which represents a 5.0-month supply at the current sales pace.This represents a 14% increase from November 2004, when the inventory of existing homes was 2.54 million.

Just a note for next month: Inventories usually fall in December as sellers take their houses off the market for the holidays.

Wednesday, December 28, 2005

Looking Forward: 2006 Top Economic Stories

by Calculated Risk on 12/28/2005 07:10:00 PM

First, here are a few stories that I don't think will be big in 2006:

1) Energy Prices: I expect oil prices to stabilize or decline next year. WTI spot prices closed at $59.96 today. This prediction could be wildly wrong, especially if production falls at Ghawar or the US bombs Iran. This prediction is based on the increased level of investment, the current levels of crude oil stocks and a slowing World economy in 2006.

2) Bush Economic proposals: I think the Bush Administration will be shackled by scandals and Iraq, so I don't expect any major new proposals. I hope I'm wrong about Iraq.

3) Trade Deficit / Current Account Deficit: I could be wildly wrong here too, but I think the trade deficit will stabilize or even decline slightly next year. As the economy slows, I think imports will slow.

4) The Budget Deficit: Although I expect the General Fund deficit to grow to around $600 Billion in 2006, I don't think it will become a huge story until '07 or '08.

So, without trying to predict natural disasters, a pandemic or human stupidity (terrorism, bombing Iran, etc.), I think these are five possible candidates for the top economic stories of 2006:

5) The End of the Greenspan Era

OK. I'll start with a gimme. I think Dr. Bernanke will face a significant challenge in '06, perhaps by one the following top stories - perhaps by something completely unexpected. Stephen Roach recently wrote:

"Alan Greenspan faced a stock-market crash two months after he took over in August 1987. Paul Volcker had to cope with a rout in the bond market three months after he became chairman in August 1979. G. William Miller was challenged immediately by a dollar crisis in the spring of 1978. For Arthur Burns, it was the inflation bogie in the early 1970s."When the challenge comes, expect investors to pine for their lost love: Alan Greenspan.

4) Housing Slowdown

In my opinion, the Housing Bubble was the top economic story of 2005, but I expect the slowdown to be a form of Chinese water torture. Sales for both existing and new homes will probably fall next year from the records set in 2005. And median prices will probably increase slightly, with declines in the more "heated markets".

3) Pension Blowup / Major Bankruptcy

Of course I am thinking GM, but maybe it will be another major corporation. Bankruptcy has become a tool to break labor agreements and terminate pension plans. This allows companies to "privatize profits and socialize risk" - and companies will increasingly use this tool.

Even "freezing" the pension plan has enormous consequences for many employees, since a large portion of the retirement benefit is accrued in the last few years before retirement. See the USAToday article: Pension problems loom for boomers.

2) Slowing Economy

If the US and the World economies slide into recession, this will be the top story next year. I still think it is too early to call, but I do think economic growth will slow substantially next year.

This slowdown will be partially housing related; as housing slows, real estate related employment will decline and jobs could become an issue in '06. Also, as mortgage equity withdrawal declines, consumer spending will slow.

And my prediction for the Top Story of '06:

1) Interest Rates

Like most investors, I expect the Fed to raise the Fed Funds rate 25 bps at each of the next two meetings to 4.75% in March. See Dr. Altig's graphs: An Inversion Arrives

And like many observers, I expect the Fed to start lowering rates later next year as the economy slows. But here is the surprise, I think long rates will start to rise when the Fed starts cutting the Fed Funds rate.

This will be Bernanke's "conundrum"! As the economy slows, this will reduce the trade deficit and also lower the amount of foreign dollars willing to invest in the US - the start of a possible vicious cycle.

I couldn't resist going out on a limb ... or a couple of limbs. Its fun making predictions - I'm looking forward to the comments.

Best to all. Happy New Year!

MBA: Mortgage Activity Declines

by Calculated Risk on 12/28/2005 10:49:00 AM

The Mortgage Bankers Association (MBA) reports: Mortgage Application Activity Slows Preceding Holiday Weekend

The Market Composite Index - a measure of mortgage loan application volume was 554.1 -- a decrease of 6.8 percent on a seasonally adjusted basis from 594.6 one week earlier. A holiday adjustment was included in the seasonally adjusted numbers to help account for the reduced application activity prior to the holiday weekend. On an unadjusted basis, the Index decreased 17.0 percent compared with the previous week and was up 3.1 percent compared with the same week one year earlier.Rates were steady:

The seasonally-adjusted Purchase Index decreased by 4.5 percent to 432.9 from 453.1 the previous week whereas the Refinance Index decreased by 11.2 percent to 1259.1 from 1418.1 one week earlier.

The average contract interest rate for 30-year fixed-rate mortgages decreased to 6.21 percent from 6.22 percent on week earlier ...Activity is falling, but still reasonably strong. These reports will be more informative after the holidays.

The average contract interest rate for one-year ARMs decreased to 5.36 percent from 5.41 percent one week earlier...

Tuesday, December 27, 2005

Looking Back: 2005 Top Economic Stories

by Calculated Risk on 12/27/2005 01:09:00 AM

Looking back, I think these were the Top Five economic stories of 2005:

5) Social Security

Social Security is the story of what didn't happen.

Drs. Mark Thoma, Brad DeLong, Paul Krugman, Andrew Samwick and my friends at Angry Bear all contributed to my understanding of this issue.

4) Interest Rates

The Federal Reserve raised the Fed Funds Rate eight times in 2005; steadily increasing the rate at a measured pace (25 bps) after each Federal Reserve meeting. The Fed Funds rate started the year at 2.25% and finished at 4.25%.

The eight increases might be a big story in and of itself, except the even bigger story was Greenspan's "conundrum" with long rates. The Ten Year Treasury Note started the year yielding 4.22% and closed last week yielding 4.38%.

Amazing.

Looking ahead: It appears the yield curve will officially invert after the next Fed Meeting (Jan 31, 2006 - Greenspan's last meeting).

For more on the Fed, I suggest reading Dr. Tim Duy and Dr. William Polley.

3) Energy Prices

Another huge story was energy prices. Even though prices have dropped recently, oil and gasoline prices are substantially higher than last year. According to the DOE, at the end of 2004, the weighted average price was $32.07 per barrel (all grades) and $51.58 last week. That is a 61% increase in the price of crude oil.

For Energy issues, see Dr. James Hamilton.

2) Trade Deficit

The trade deficit continued to increase in 2005. For the Jan through Oct period, the US trade deficit was $598 Billion, up from $504 Billion for the comparable period in 2005. The US is heading for a $720+ Billion trade deficit for 2005, or close to 6% of GDP.

For more, see Dr. Brad Setser and Dr. Menzie Chinn.

And the biggest story of the year ...

1) The Housing Bubble

I've written extensively about housing on this blog and at Angry Bear. For daily updates, I've linked to several sites on the right under "Housing Sites".

I'll write a "looking forward" to 2006 post later this week. Note: Iraq and Katrina were also huge stories in 2005 from an economic perspective, as were hurricanes in general and global warming. Iraq is a huge story from many perspectives, but I am trying to stick to macroeconomics.

Best to all. Happy New Year!

Friday, December 23, 2005

November New Home Sales: 1.245 Million Annual Rate

by Calculated Risk on 12/23/2005 10:11:00 AM

According to the Census Bureau report, New Home Sales in November were at a seasonally adjusted annual rate of 1.245 million vs. market expectations of 1.30 million. October's record sales were revised down slightly to 1.404 million from 1.424 million.

Click on Graph for larger image.

NOTE: The graph starts at 700 thousand units per month to better show monthly variation.

The Not Seasonally Adjusted monthly rate was 85,000 New Homes sold, down from a revised 110,000 in October.

On a year over year basis, November 2005 sales were 1% higher than November 2004.

The median and average sales prices are trending down.

The median sales price of new houses sold in November 2005 was $225,200; the average sales price was $283,300.

The seasonally adjusted estimate of new houses for sale at the end of November was 503,000. This represents a supply of 4.9 months at the current sales rate.

The 503,000 units of inventory is the all time record for new houses for sale. On a months of supply basis, inventory is above the level of recent years.

This report is still reasonably strong.

Thursday, December 22, 2005

West Coast Ports: November Imports Mixed, Exports Up

by Calculated Risk on 12/22/2005 03:01:00 PM

The Ports of Long Beach and Los Angeles reported mixed import traffic for October.

Import traffic at the Port of Long Beach increased 2.0% compared to October. A total of 305 thousand loaded cargo containers came into the Port of Long Beach, compared to 299 thousand in October. The record is 313 thousand set in August 2005.

The Port of Los Angeles import traffic decreased 11% in November. Imports were 325.1 thousand containers, off from the record set in October for the Port of Los Angeles of 368.5 thousand containers.

For Long Beach, outbound traffic was up 3.6% to 107 thousand containers. At Los Angeles, outbound traffic was flat at 98 thousand containers.

The quantity of containers says nothing about the content value, but provides a rough guide on imports from China and the rest of Asia. Given these numbers, I expect imports from Asia to be about the same in November as in October.

Wednesday, December 21, 2005

Martin Wolf Podcast: The surprises of the past year

by Calculated Risk on 12/21/2005 09:05:00 PM

From the Financial Times, Martin Wolf discusses the world economy:

Wolf's discussion starts a little slow, reciting a number of growth statistics, however the second half of the podcast regarding global imbalances is interesting.

MBA: Mortgage Application Volume Down

by Calculated Risk on 12/21/2005 10:38:00 AM

The Mortgage Bankers Association (MBA) reports: Mortgage Application Volume Down In Latest Survey

The Market Composite Index — a measure of mortgage loan application volume was 594.6 -- a decrease of 4.0 percent on a seasonally adjusted basis from 619.3 one week earlier. On an unadjusted basis, the Index decreased 5.2 percent compared with the previous week and was down 15.2 percent compared with the same week one year earlier.

The seasonally-adjusted Purchase Index decreased by 5.2 percent to 453.1 from 477.9 the previous week, whereas the Refinance Index decreased by 1.6 percent to 1418.1 from 1441.8 one week earlier.

Click on graph for larger image.

The graph shows overall and purchase activity since June. Overall activity has fallen significantly due to the drop in refis.

Mortgage rates decreased slightly again last week:

The average contract interest rate for 30-year fixed-rate mortgages decreased to 6.22 percent from 6.28 percent on week earlier ...Overall this report shows purchase activity might be weakening, but it is still at a very high level.

The average contract interest rate for 15-year fixed-rate mortgages decreased to 5.76 percent from 5.83 percent ...

{kind=link}