RSS Feed

RSS Feed by Calculated Risk on 12/11/2021 02:11:00 PM

Saturday, December 11, 2021

Real Estate Newsletter Articles this Week

At the Calculated Risk Real Estate Newsletter this week:

• 2nd Look at Local Housing Markets in November Adding Houston, Jacksonville, Nashville, New Hampshire, North Texas, Portland and Santa Clara

• The Home ATM in Q3 2021 aka Mortgage Equity Withdrawal (MEW)

• Lawler: Updates on Key Drivers of US Population Growth Lowest Growth in over a Century from 7/1/2020 to 7/1/2021

• 1st Look at Local Housing Markets in November "2022 will be a wild and competitive ride"

• As Forbearance Ends

This is usually published several times a week, and provides more in-depth analysis of the housing market.

The blog will continue as always!

You can subscribe at https://calculatedrisk.substack.com/ Currently all content is available for free - and some will always be free - but please subscribe!.

You can subscribe at https://calculatedrisk.substack.com/ Currently all content is available for free - and some will always be free - but please subscribe!.

Schedule for Week of December 12, 2021

by Calculated Risk on 12/11/2021 08:11:00 AM

The key economic reports this week are November Retail Sales and Housing Starts.

For manufacturing, November Industrial Production, and the December New York, Philly and Kansas City Fed surveys, will be released this week.

The FOMC meets this week, and the FOMC is expected to announce a faster taper pace for asset purchases.

No major economic releases scheduled.

6:00 AM: NFIB Small Business Optimism Index for November.

8:30 AM: The Producer Price Index for November from the BLS. The consensus is for a 0.6% increase in PPI, and a 0.5% increase in core PPI.

7:00 AM ET: The Mortgage Bankers Association (MBA) will release the results for the mortgage purchase applications index.

8:30 AM ET: Retail sales for November will be released. The consensus is for a 1.4% increase in retail sales.

8:30 AM ET: Retail sales for November will be released. The consensus is for a 1.4% increase in retail sales.This graph shows retail sales since 1992. This is monthly retail sales and food service, seasonally adjusted (total and ex-gasoline).

8:30 AM: The New York Fed Empire State manufacturing survey for December. The consensus is for a reading of 25.0, down from 30.9.

10:00 AM: The December NAHB homebuilder survey. The consensus is for a reading of 84, up from 83. Any number above 50 indicates that more builders view sales conditions as good than poor.

2:00 PM: FOMC Meeting Announcement. The FOMC is expected to announce a faster taper pace for asset purchases.

2:00 PM: FOMC Forecasts This will include the Federal Open Market Committee (FOMC) participants' projections of the appropriate target federal funds rate along with the quarterly economic projections.

2:30 PM: Fed Chair Jerome Powell holds a press briefing following the FOMC announcement.

8:30 AM: The initial weekly unemployment claims report will be released. The consensus is for 200 thousand initial claims, up from 184 thousand last week.

8:30 AM: Housing Starts for November.

8:30 AM: Housing Starts for November. This graph shows single and multi-family housing starts since 1968.

The consensus is for 1.570 million SAAR, up from 1.520 million SAAR.

8:30 AM: the Philly Fed manufacturing survey for December. The consensus is for a reading of 27.0, down from 39.0.

9:15 AM: The Fed will release Industrial Production and Capacity Utilization for November.

9:15 AM: The Fed will release Industrial Production and Capacity Utilization for November.This graph shows industrial production since 1967.

The consensus is for a 0.7% increase in Industrial Production, and for Capacity Utilization to increase to 76.8%.

11:00 AM: the Kansas City Fed manufacturing survey for December.

10:00 AM: State Employment and Unemployment (Monthly) for November

Friday, December 10, 2021

Black Knight: Number of Mortgages in Forbearance Declines "Significantly"

by Calculated Risk on 12/10/2021 07:05:00 PM

This data is as of December 7th.

From Andy Walden at Black Knight: Forbearance Plan Exits Drop Significantly

Active forbearance plan totals plunged in the first full week of December, led by portfolio held and privately securitized loans.

According to our McDash Flash daily forbearance tracking dataset, the number of active forbearance plans fell by 112,000 (-11%) this week, led by a 49,000 (-15%) drop in PLS/portfolio loans. FHA/VA plan volumes dropped 42,000 (-12%) followed by GSE (21,000/-7%). There is a modest opportunity for additional improvement in coming weeks with 33,000 loans still listed with November reviews for extension/removal (roughly half of which are expected to be reaching their final expirations).

As of December 7, 882,000 mortgage holders (1.7%) remain in COVID-19 related forbearance plans, including 1.1% of GSE, 2.6% of FHA/VA and 2.1% of portfolio/PLS.

Click on graph for larger image.

Overall, the number of forbearance plans is down by 177,000 (-17%) from the same time last month, with the potential for modest additional improvements through the end of the year. Plan starts over the past four weeks are up 24% from the preceding four-week period, driven by a more than 40% increase among FHA/VA loans (with GSEs seeing a 29% increase). This is a trend we’ll be watching closely as we round out the year.

emphasis added

2nd Look at Local Housing Markets in November

by Calculated Risk on 12/10/2021 01:33:00 PM

Today, in the Real Estate Newsletter: 2nd Look at Local Housing Markets in November

Excerpt:

Adding Houston, Jacksonville, Nashville, New Hampshire, North Texas, Portland and Santa Clara

...

Here is a summary of active listings for these housing markets in November. Inventory was down 15.8% in November month-over-month (MoM) from October, and down 25.0% year-over-year (YoY).

Inventory almost always declines seasonally in November, so the MoM decline is not a surprise. Last month, these markets were down 23.3% YoY, so the YoY decline in November is larger than in October. This isn’t indicating a slowing market.

Notes for all tables:

1. New additions to table in BOLD.

2. Northwest (Seattle), North Texas (Dallas), and Santa Clara (San Jose), Jacksonville, Source: Northeast Florida Association of REALTORS®

Q4 GDP Forecasts: Moving Up

by Calculated Risk on 12/10/2021 12:36:00 PM

From BofA:

4Q GDP tracking moved up to 6.5% qoq saar from 6.0%, reflecting the strong signal from the BAC card spending data. [December 10 estimate]And from the Altanta Fed: GDPNow

emphasis added

The GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the fourth quarter of 2021 is 8.7 percent on December 9, up from 8.6 percent on December 7. [December 9 estimate]

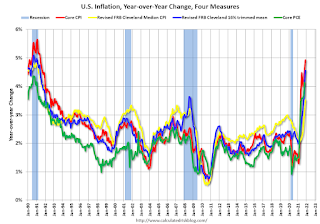

Cleveland Fed: Median CPI increased 0.5% and Trimmed-mean CPI increased 0.5% in November

by Calculated Risk on 12/10/2021 11:34:00 AM

The Cleveland Fed released the median CPI and the trimmed-mean CPI this morning:

According to the Federal Reserve Bank of Cleveland, the median Consumer Price Index rose 0.5% in November. The 16% trimmed-mean Consumer Price Index increased 0.5% in November. "The median CPI and 16% trimmed-mean CPI are measures of core inflation calculated by the Federal Reserve Bank of Cleveland based on data released in the Bureau of Labor Statistics’ (BLS) monthly CPI report".

Note: The Cleveland Fed released the median CPI details here: "Fuel oil and other fuels" were up 104% annualized.

Note that Owners' Equivalent Rent and Rent of Primary Residence account for almost 1/3 of median CPI, and these measures were up around 5% to 6% annualized in November.

Click on graph for larger image.

Click on graph for larger image.

This graph shows the year-over-year change for these four key measures of inflation.

Click on graph for larger image.This graph shows the year-over-year change for these four key measures of inflation.

On a year-over-year basis, the median CPI rose 3.5%, the trimmed-mean CPI rose 4.6%, and the CPI less food and energy rose 4.9%. Core PCE is for October and increased 4.1% year-over-year.

BLS: CPI increased 0.8% in November; Core CPI increased 0.5%

by Calculated Risk on 12/10/2021 08:32:00 AM

The Consumer Price Index for All Urban Consumers (CPI-U) increased 0.8 percent in November on a seasonally adjusted basis after rising 0.9 percent in October, the U.S. Bureau of Labor Statistics reported today. Over the last 12 months, the all items index increased 6.8 percent before seasonal adjustment.Both CPI and core CPI were close to expectations. I'll post a graph later today after the Cleveland Fed releases the median and trimmed-mean CPI.

The monthly all items seasonally adjusted increase was the result of broad increases in most component indexes, similar to last month. The indexes for gasoline, shelter, food, used cars and trucks, and new vehicles were among the larger contributors. The energy index rose 3.5 percent in November as the gasoline index increased 6.1 percent and the other major energy component indexes also rose. The food index increased 0.7 percent as the index for food at home rose 0.8 percent.

The index for all items less food and energy rose 0.5 percent in November following a 0.6-percent increase in October. Along with shelter, used cars and trucks, and new vehicles, the indexes for household furnishings and operations, apparel, and airline fares were among those that increased. The indexes for motor vehicle insurance, recreation, and communication all declined in November.

The all items index rose 6.8 percent for the 12 months ending October, the largest 12-month increase since the period ending June 1982. The index for all items less food and energy rose 4.9 percent over the last 12 months, while the energy index rose 33.3 percent over the last year, and the food index increased 6.1 percent. These changes are the largest 12-month increases in at least 13 years in the respective series.

emphasis added

Thursday, December 09, 2021

Friday: CPI

by Calculated Risk on 12/09/2021 08:47:00 PM

Friday:

• At 8:30 AM ET, The Consumer Price Index for November from the BLS. The consensus is for a 0.7% increase in CPI, and a 0.5% increase in core CPI.

• At 10:00 AM: University of Michigan's Consumer sentiment index (Preliminary for December).

| COVID Metrics | ||||

|---|---|---|---|---|

| Today | Week Ago | Goal | ||

| Percent fully Vaccinated | 60.5% | --- | ≥70.0%1 | |

| Fully Vaccinated (millions) | 200.7 | --- | ≥2321 | |

| New Cases per Day3🚩 | 118,515 | 86,315 | ≤5,0002 | |

| Hospitalized3🚩 | 53,714 | 48,089 | ≤3,0002 | |

| Deaths per Day3🚩 | 1,092 | 854 | ≤502 | |

| 1 Minimum to achieve "herd immunity" (estimated between 70% and 85%). 2my goals to stop daily posts, 37-day average for Cases, Currently Hospitalized, and Deaths 🚩 Increasing 7-day average week-over-week for Cases, Hospitalized, and Deaths ✅ Goal met. | ||||

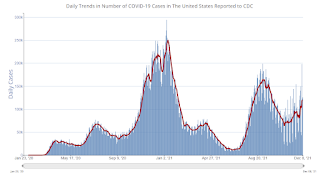

Click on graph for larger image.

Click on graph for larger image.This graph shows the daily (columns) and 7-day average (line) of positive tests reported.

The Home ATM, aka Mortgage Equity Withdrawal (MEW)

by Calculated Risk on 12/09/2021 02:46:00 PM

Today, in the Real Estate Newsletter: The Home ATM in Q3 2021

Excerpt:

In Q3 2021, mortgage debt increased $230 billion, the largest quarterly increase since 2006.

...

For Q3 2021, the Net Equity Extraction was $147 billion, or 3.24% of Disposable Personal Income (DPI). The last two quarters have shown a sharp increase in equity extraction compared to recent years, but the level is nothing like the amount of equity extraction during the housing bubble as a percent of DPI. During the housing bubble we saw several quarters with MEW above 8% of DPI.

...

The bottom line is the recent increase in MEW is not concerning - it is far less as a percent of disposable personal income than during the bubble, and most homeowners have substantial equity.

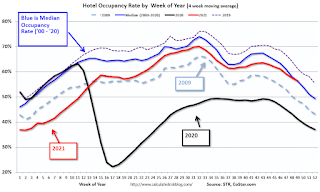

Hotels: Occupancy Rate Down 9% Compared to Same Week in 2019

by Calculated Risk on 12/09/2021 01:13:00 PM

Note: Since occupancy declined sharply at the onset of the pandemic, CoStar is comparing to 2019.

From CoStar: STR: US Weekly Hotel Occupancy Hovers Around Mid-50%

U.S. hotel occupancy increased from the previous week, but performance comparisons with 2019 were lower, according to STR‘s latest data through December 4.The following graph shows the seasonal pattern for the hotel occupancy rate using the four week average.

November 28 through December 4, 2021 (percentage change from comparable week in 2019*):

• Occupancy: 54.8% (-8.8%)

• Average daily rate (ADR): $127.92 (-0.5%)

• Revenue per available room (RevPAR): $70.08 (-9.2%)

*Due to the steep, pandemic-driven performance declines of 2020, STR is measuring recovery against comparable time periods from 2019.

emphasis added

Click on graph for larger image.

Click on graph for larger image.The red line is for 2021, black is 2020, blue is the median, dashed purple is 2019, and dashed light blue is for 2009 (the worst year on record for hotels prior to 2020).

Although down compared to 2019, the 4-week average of the occupancy rate is close to the median rate for the previous 20 years (Blue).

Note: Y-axis doesn't start at zero to better show the seasonal change.

The occupancy rate will now decline seasonally into the new year.