RSS Feed

RSS Feed by Calculated Risk on 6/26/2009 09:49:00 PM

Friday, June 26, 2009

Bank Failure #45: Mirae Bank, California Fails

A mirage of asset wealth

We now know the truth.

by Soylent Green is People

Update: From the FDIC:

The FDIC estimates that the cost to the Deposit Insurance Fund (DIF) will be $50 million. Wilshire State Bank's acquisition of all the deposits was the "least costly" resolution for the FDIC's DIF compared to alternatives. Mirae Bank is the 45th FDIC-insured institution to fail in the nation this year, and the sixth in California.Press Release from the California Department of Financial Institutions (DFI)

The California Department of Financial Institutions (DFI) announced today that regulators have closed Mirae Bank, citing inadequate capital.No announcement from FDIC yet.

As of June 15, 2009, Mirae Bank, located in Southern California, had total assets of approximately $411.1 million and total deposits of approximately $338.5 million. The DFI has been closely monitoring the bank because of its inadequate capital level. The DFI had ordered it to increase its capital reserves to a safe and sound level but efforts by the bank to do so were unsuccessful.

Immediately following the closure, the DFI named the Federal Deposit Insurance Corporation (FDIC) as receiver of Mirae Bank. The depositors of Mirae Bank are protected by the FDIC. The FDIC has accepted a bid from Wilshire State Bank to assume all branch deposits and significantly all the assets of Mirae Bank.

Truck Tonnage Index Increased in May, Off 11% from May 2008

by Calculated Risk on 6/26/2009 08:16:00 PM

From the American Trucking Association: ATA Truck Tonnage Index Increased 3.2 Percent in May Click on graph for larger image in new window.

Click on graph for larger image in new window.

The American Trucking Associations’ advance seasonally adjusted (SA) For-Hire Truck Tonnage Index rose for the first time since February 2009, gaining 3.2 percent in May. May’s increase, which raised the SA index to 102.3, wasn’t large enough to offset the March through April cumulative reduction of 6.7 percent. ...

Compared with May 2008, tonnage contracted 11 percent, which was the best year-over-year result in three months. Despite the improvement from April’s 13.2 percent plunge, May’s decrease is still historically large.

ATA Chief Economist Bob Costello said the month-to-month improvement was encouraging, but cautioned that tonnage is unlikely to surge anytime soon. “I am hopeful that the worst is behind us, but I just don’t see anything on the economic horizon that suggests freight transportation is ready to explode,” Costello said. “The consumer is still facing too many headwinds, including employment losses, tight credit, rising fuel prices, and falling home values, to name a few, that will make it very difficult for household spending to jump in the near term.” He also noted that he doesn’t expect tonnage to deteriorate much further and that any growth in tonnage over the next few months is likely to be modest.

Note on the impact of trucking company failures on the index: Each month, ATA asks its membership the amount of tonnage each carrier hauled, including all types of freight. The indexes are calculated based on those responses. The sample includes an array of trucking companies, ranging from small fleets to multi-billion dollar carriers. When a company in the sample fails, we include its final month of operation and zero it out for the following month, with the assumption that the remaining carriers pick up that freight. As a result, it is close to a net wash and does not end up in a false increase. Nevertheless, some carriers are picking up freight from failures, and it may have boosted the index. Due to our correction mentioned above, however, it should be limited.

Trucking serves as a barometer of the U.S. economy, representing nearly 69 percent of tonnage carried by all modes of domestic freight transportation, including manufactured and retail goods ...

Bank Failures #43 & #44: MetroPacific Bank, Irvine, CA, Horizon Bank, Pine City, Minnesota

by Calculated Risk on 6/26/2009 07:28:00 PM

Local to CR, Soylent

Big Irvine implode.

Debt, Destruction, De-Leverage

A cliff dive too far.

both by Soylent Green is People

From the FDIC: Stearns Bank, National Association, St. Cloud, Minnesota, Assumes All of the Deposits of Horizon Bank, Pine City, Minnesota

Horizon Bank, Pine City, Minnesota, was closed today by the Minnesota Department of Commerce, which appointed the Federal Deposit Insurance Corporation (FDIC) as receiver. ...From the FDIC: Sunwest Bank, Tustin, California, Assumes All of the Deposits of MetroPacific Bank, Irvine, California

As of March 31, 2009, Horizon Bank had total assets of $87.6 million and total deposits of approximately $69.4 million. ...

The FDIC estimates that the cost to the Deposit Insurance Fund (DIF) will be $33.5 million. Stearns Bank's, N.A. acquisition of all the deposits was the "least costly" resolution for the FDIC's DIF compared to alternatives. Horizon Bank is the 43rd FDIC-insured institution to fail in the nation this year, and the first in Minnesota.

MetroPacific Bank, Irvine, California was closed today by the California Department of Financial Institutions, which appointed the Federal Deposit Insurance Corporation (FDIC) as receiver. ...Four down today ...

As of June 8, 2009, MetroPacific Bank had total assets of $80 million and total deposits of approximately $73 million. ...

The FDIC estimates that the cost to the Deposit Insurance Fund (DIF) will be $29 million. Sunwest Bank's acquisition of all the deposits was the "least costly" resolution for the FDIC's DIF compared to alternatives. MetroPacific is the 44th FDIC-insured institution to fail in the nation this year, and the fifth in California.

Bank Failure #42: Neighborhood Community Bank, Newnan, Georgia

by Calculated Risk on 6/26/2009 06:28:00 PM

Fertile soil for bank failure

Bumper crop this year.

by Soylent Green is People

From the FDIC: CharterBank, West Point, Georgia Assumes All of the Deposits of Neighborhood Community Bank, Newnan, Georgia

Neighborhood Community Bank, Newnan, Georgia, was closed today by the Georgia Department of Banking and Finance, which appointed the Federal Deposit Insurance Corporation (FDIC) as receiver. ...Newnan ... (or "Noonan") ... for you Caddyshack fans.

As of March 31, 2009, Neighborhood Community Bank had total assets of $221.6 million and total deposits of approximately $191.3 million. ...

The FDIC and CharterBank entered into a loss-share transaction on approximately $178.5 million of Neighborhood Community Bank's assets. ...

The FDIC estimates that the cost to the Deposit Insurance Fund (DIF) will be $66.7 million. CharterBank's acquisition of all the deposits was the "least costly" resolution for the FDIC's DIF compared to alternatives. Neighborhood Community Bank is the 42nd FDIC-insured institution to fail in the nation this year

Bank Failure #41: Community Bank of West Georgia, Villa Rica, Georgia

by Calculated Risk on 6/26/2009 05:46:00 PM

Zero rest for the wicked,

Neither for Blair's crew.

by Soylent Green is People

From the FDIC: FDIC Approves the Payout of Insured Deposits of Community Bank of West Georgia, Villa Rica, Georgia

Community Bank of West Georgia, Villa Rica, Georgia, was closed today by the Georgia Department of Banking and Finance, which appointed the FDIC as receiver. To protect the depositors, the Federal Deposit Insurance Corporation (FDIC) will mail checks to insured depositors for their insured funds on Monday morning, June 29th.This is another closing without a buyer - I think the third this year.

...

As of May 15, 2009, Community Bank of West Georgia had total assets of $199.4 million and total deposits of $182.5 million.

...

The FDIC estimates the cost of the failure to its Deposit Insurance Fund to be approximately $85 million. Community Bank of West Georgia is the 41st FDIC-insured institution to fail in the nation this year, and the eighth in Georgia.

JPMorgan, Citi Expanding Jumbo Lending

by Calculated Risk on 6/26/2009 03:32:00 PM

From Bloomberg: JPMorgan, Citigroup Expand in ‘Jumbo’ Home Mortgages

JPMorgan resumed buying new jumbo loans made by other lenders this month, after halting purchases in March, spokesman Tom Kelly said. ... Citigroup is again offering the loans through independent mortgage brokers, spokesman Mark Rodgers said.This will help a little - but the standards are pretty tight and there more problems coming for the mid-to-high end (like Option ARM recasts and few move-up buyers).

...

New jumbo lending, which includes refinancing as well as debt for home buyers, totaled $348 billion in 2007, before dropping to $98 billion last year as mortgage companies tightened standards, according to newsletter Inside Mortgage Finance. Jumbo lending slowed in the fourth quarter to $11 billion, or 4 percent of the mortgage market, the lowest quarterly amount since Inside Mortgage Finance started tracking that data in 1990.

...

Bank of America Corp. was the largest jumbo lender in the first quarter, with almost $9 billion in new loans, followed by Citigroup ...

More than 7 percent of prime-jumbo loans backing securities sold in 2006 and 2007 were at least 90 days late, Standard & Poor’s said yesterday.

Freddie Mac: Portfolio Shrinks, Delinquencies Rise

by Calculated Risk on 6/26/2009 02:02:00 PM

Click on graph for large image.

Click on graph for large image.

This graph shows the Freddie Mac single family delinquency rate since January 2005.

Here is the Freddie Mac portfolio data.

From Reuters: Freddie Mac May portfolio shrank annualized 9.9 pct (ht Ron)

Freddie Mac ... said its mortgage investment portfolio shrank by an annualized 9.9 percent rate in May, while delinquencies on loans it guarantees accelerated.

The portfolio decreased to $823.4 billion, for an annualized 5.6 percent increase year to date, the McLean, Virginia-based company said in its monthly volume summary.

In May 2008, the portfolio was $770.4 billion.

Delinquencies ... jumped to 2.62 percent of its book of business in May from 2.44 percent in April and 0.86 percent in May 2008.

...

Freddie Mac said refinance-loan purchase volume was $40.3 billion in May, down from April's $43.3 billion. March's $52 billion was its largest refinance month since 2003.

FDIC: 104 Cease and Desist Orders through May

by Calculated Risk on 6/26/2009 11:43:00 AM

The FDIC has been very busy issuing Cease and Desist orders this year. Through May, the FDIC has issued 104 Cease and Desist orders and this does not include any orders by the OCC or OTS. (ht Terry)

Most of these oreders are very similar - here is an excerpt:

IT IS HEREBY ORDERED, that the Bank, its institution-affiliated parties, as that term is defined in section 3(u) of the Act, 12 U.S.C. § 1813(u), and its successors and assigns, cease and desist from the following unsafe and unsound banking practices, as more fully set forth in the FDIC's Report of Visitation ...:All of these institutions are ordered to make changes - and some do, and then the cease and desist order is terminated (15 orders have been teriminated). The remaining are BFF candidates.

a) operating with management whose policies and practices are detrimental to the Bank and jeopardize the safety of its deposits;

(b) operating with a board of directors which has failed to provide adequate supervision over and direction to the active management of the Bank;

(c) operating with a large volume of poor quality loans;

(d) engaging in unsatisfactory lending and collection practices;

(e) operating in such a manner as to produce operating losses; and

(f) operating with inadequate provisions for liquidity.

emphasis added

Here are the FDIC press releases this year:

May Cease and Desist Orders (23)

April Cease and Desist Orders (24)

March Cease and Desist Orders (23)

February Cease and Desist Orders (21)

January Cease and Desist Orders (13)

NY Fed and AIG Deal

by Calculated Risk on 6/26/2009 10:22:00 AM

From the WaPo: N.Y. Fed to Trim AIG Debt, Receive $25 Billion Stake in Two Subsidiaries

American International Group announced yesterday that it has reached a deal to reduce its debt to the Federal Reserve Bank of New York by $25 billion.The Fed is now in the insurance business ...

[AIG] said that it would give the New York Fed preferred stakes in ... Asian-based American International Assurance, or AIA, and American Life Insurance Co., or Alico, which operates in more than 50 countries.

Under the agreement, AIG will split off AIA and Alico into separate company-owned entities called "special purpose vehicles," or SPVs. The New York Fed will receive preferred shares now valued at $25 billion -- $16 billion in AIA and $9 billion in Alico -- and in exchange will forgive an equal amount of AIG debt.

Personal Income and Outlays Boosted by Stimulus

by Calculated Risk on 6/26/2009 08:30:00 AM

From the BEA: Personal Income and Outlays, April 2009

Personal income increased $167.1 billion, or 1.4 percent, and disposable personal income (DPI) increased $178.1 billion, or 1.6 percent, in May, according to the Bureau of Economic Analysis. Personal consumption expenditures (PCE) increased $25.1 billion, or 0.3 percent. In April, personal income increased $78.3 billion, or 0.7 percent, DPI increased $140.0 billion, or 1.3 percent, and PCE increased $1.0 billion, or less than 0.1 percent, based on revised estimates. The pattern of changes in personal income and in DPI reflect, in part, the pattern of increased government social benefit payments associated with the American Recovery and Reinvestment Act of 2009.The May numbers were impacted by the American Recovery and Reinvestment Act of 2009. As an example, payments to seniors increased sharply and “Personal Current Transfers,” increased by $165 billion (annual rate). This boosted personal income.

...

Real PCE -- PCE adjusted to remove price changes -- increased 0.2 percent in May, in contrast to a decrease of 0.1 percent in April.

...

Personal saving -- DPI less personal outlays -- was $768.8 billion in May, compared with $608.5 billion in April. Personal saving as a percentage of disposable personal income was 6.9 percent in May, compared with 5.6 percent in April.

This also pushed up the saving rate sharply to the highest rate since Dec 1993 (but this is a temporary boost).

A couple points:

Click on graph for large image.

Click on graph for large image.This graph shows the saving rate starting in 1959 (using a three month centered average for smoothing) through the April Personal Income report. The saving rate was 6.9% in April. (6.3% with average)

The saving rate was boosted by the stimulus package, but this suggests households are saving substantially more than during the last few years (when the saving rate was close to zero). The saving rate will probably dip - the stimulus boost is unsustainable - but then continue to rise (an aging population usually pushes the saving rate higher) and a rising saving rate will repair household balance sheets, but this will also keep pressure on personal consumption.

The following graph shows real Personal Consumption Expenditures (PCE) through May (2000 dollars). Note that the y-axis doesn't start at zero to better show the change.

PCE declined sharply in Q3 and Q4 2008, and rebounded slightly in Q1 2009.

PCE declined sharply in Q3 and Q4 2008, and rebounded slightly in Q1 2009.Although PCE increased in May (compared to April), Q2 2009 is off to a somewhat weak start, with PCE in both April and May slightly below the levels of Q1. Although it is possible that PCE will pick up in June, it seems likely that PCE will be flat to slightly negative in Q2 (although not the cliff diving of the 2nd half of 2008). The two-month estimate suggests a real PCE decline of 0.7% in Q2 2009.

Usually PCE and Residential Investment (RI) lead the economy out of recession, and right now both remain weak. As households increase their savings rate to repair their balance sheets, it seems unlikely that PCE will increase significantly any time soon.

Song Parody: "Where Credit is Due"

by Calculated Risk on 6/26/2009 12:45:00 AM

From Versusplus - a little credit card music!

Thursday, June 25, 2009

The Leveraged Loan "Wall of Worry"

by Calculated Risk on 6/25/2009 11:51:00 PM

From the WSJ: Rates Low, Firms Race to Refinance Their Debts

[C]ompanies are seeking to sidestep what is likely to be the biggest-ever wave of loan refinancing among risky companies as $440 billion in debt comes due in a span of three years [from 2012 to 2014]. That is about 85% of the $518 billion in current leveraged loans outstanding ...The looming credit problems are not just Option ARMs and CRE loans; there are about $75 billion in leveraged coming due in 2012, another $150 billion in 2013 and close to $215 billion in 2014.

Some firms [are negotiating extensions]. Others are issuing junk bonds or stock, using the cash raised to repay some of their loans well ahead of schedule.

The pre-emptive moves demonstrate rising concern about the massive bubble of lending that developed from 2005 to 2007.

The credit bubble: the gift that keeps on giving.

CRE: Office Building sold in Denver

by Calculated Risk on 6/25/2009 08:05:00 PM

This is an interesting transaction for several reasons:

From the Denver Post: 17th Street Plaza sale is biggest in Denver this year

A Massachusetts-based real-estate investment trust has paid $135 million in cash for 17th Street Plaza in the largest real-estate deal done in Denver this year.A few months ago, CoStar noted that Class A office space average actual cap rates had risen from 6.1% in Q4 2007 to 7.9% in Q4 2008. And this sale suggests cap rates have risen further ... as CRE prices fall.

HRPT Properties Trust bought the 32-story building at 1225 17th St. from J.P. Morgan, which was represented by brokers Mary Sullivan and Tim Swan of CB Richard Ellis.

Sullivan declined to reveal the sale price, but people in the real-estate community pegged the deal at $135 million.

...

"It's substantially below the replacement cost to build that building," [Todd Roebken, managing director of Jones Lang LaSalle] said.

House Committee on Oversight Releases BofA Merrill Documents

by Calculated Risk on 6/25/2009 06:22:00 PM

The Committee on Oversight and Government Reform released a couple of interesting documents this afternoon.

The first document contains some Federal Reserve emails and documents.

See page 2 you will find an overview of Merrill's legacy portfolio.

How about this message from a Senior Fed Vice President on 12/20/2008 (page 8):

Some very preliminary thoughts on getting a pound of flesh out of Ken Lewis. Should we do this as part of the agreement to bail them out or just let them know we will be contacting them with a board resolution/mou in January. Your thoughtsAnd many other memos.

And another document of interest. There is an interesting discussion on PDF pages 11 through 16 on the financial system that was apparently prepared by the Federal Reserve staff.

There will be quiz later ...

Market and LO Quiz

by Calculated Risk on 6/25/2009 04:11:00 PM

A few stories too ... a major auto supplier is near bankruptcy ...

From Dow Jones: Lear Corp. Working On Prepackaged Bankruptcy - Sources

Lear Corp. (LEA), a maker of automotive seats and interior electronics, is working on a pre-packaged bankruptcy five days before it must make a $38 million interest payment on two of its bonds ... If the prepackaged bankruptcy deal falls apart, Lear could file for a traditonal-style bankruptcy next week ... The company has also lined up debtor-in-possession financing with its lenders ...From MarketWatch: Fitch downgrades California to A-minus

Fitch Ratings downgraded the California's general obligation credit rating on Thursday to A-minus from A, based on the magnitude of the state's financial challenges and persistent weakening economy.

Click on graph for larger image in new window.

Click on graph for larger image in new window.This graph is from Doug Short of dshort.com (financial planner): "Four Bad Bears".

Note that the Great Depression crash is based on the DOW; the three others are for the S&P 500.

And Jillayne Schlicke (of CEForward.com) brings us a few sample questions provided by the National Mortgage Licensing System for the new national loan originator exam: Will the New National Loan Originator Exam be Too Easy?. Here are the first two of six questions she posted:

If an applicant works 40 hours every week and is paid $13.52 per hour, what is the applicant’s monthly income?Take the test.

(A) $2,163.20

(B) $2,343.47

(C) $2,379.52

(D) $2,487.68

The requirement for private mortgage insurance is generally discounted when the loan-to-value ratio falls below:

(A) 20%

(B) 50%

(C) 80%

(D) 90%

New BankUnited CEO John Kanas: No Green Shoots

by Calculated Risk on 6/25/2009 03:04:00 PM

From CNBC interview (video here, comments start at 6:40) (ht Brian)

Q: You've said in some cases what appears to be a green shoot might actually end up being moss - moss growing on a rock ...There is a discussion on the saving rate too and the impact on consumption. The personal income and outlays (and saving rate) for May will be released tomorrow.

Kanas: Actually what I said is I hope it's not mold growing on a stagnant economy. But frankly I understand that there are - I hate the term green shoots, and we all talk about it every day - but I don't see it that much. I'm on main street every day, and I'm in a lot of different markets - I'm in New York half the week, and Florida half the week, and were dealing with thousands of people and hundreds of businesses every day and there are very limited green shoots from my perspective.

Hotel RevPAR off 20.5 Percent

by Calculated Risk on 6/25/2009 02:07:00 PM

From HotelNewsNow.com: STR posts US results for 14-20 June 2009

In year-over-year measurements, the industry’s occupancy fell 11.5 percent to end the week at 63.0 percent. Average daily rate dropped 10.1 percent to finish the week at US$96.78. Revenue per available room [RevPAR] for the week decreased 20.5 percent to finish at US$61.01.The report also includes some hightlights on the performance for the top 25 markets. As an example, occupancy is off almost 20% in Dallas and Phoenix, and the Average daily rate (ADR) is off 30% and RevPAR off 35% in New York. Ouch.

No wonder more and more hotels are defaulting ...

Click on graph for larger image in new window.

Click on graph for larger image in new window.This graph shows the YoY change in the occupancy rate (3 week trailing average).

The three week average is off 12.1% from the same period in 2008.

The average daily rate is down 10.1%, so RevPAR is off 20.5% from the same week last year.

Note: some readers might notice the occupancy rate has risen to 63% - but that is just seasonal. The hotel occupancy rate is usually the highest during the peak vacation months of June, July and August.

Fed Extends Some Emergency Lending Facilities, Trims Others

by Calculated Risk on 6/25/2009 12:52:00 PM

The Federal Reserve on Thursday announced extensions of and modifications to a number of its liquidity programs. Conditions in financial markets have improved in recent months, but market functioning in many areas remains impaired and seems likely to be strained for some time. As a consequence, to promote financial stability and support the flow of credit to households and businesses, the Federal Reserve is extending a number of facilities through early 2010. At the same time, in light of the improvement in financial conditions and reduced usage of some facilities, the Federal Reserve is trimming the size and changing the terms of some facilities.The TSLF lent Treasury securities to primary dealers, secured by certain other securities, for a term of 28 days rather than the usual overnight. Suspending that program seems like a minor change, but it does show the panic has subsided.

Specifically, the Board of Governors approved extension through February 1, 2010, of the Asset-Backed Commercial Paper Money Market Mutual Fund Liquidity Facility (AMLF), the Commercial Paper Funding Facility (CPFF), the Primary Dealer Credit Facility (PDCF), and the Term Securities Lending Facility (TSLF). The expiration date for the Term Asset-Backed Securities Loan Facility (TALF) currently remains set at December 31, 2009. The Term Auction Facility (TAF) does not have a fixed expiration date.

The extension of the TSLF also required the approval of the Federal Open Market Committee (FOMC), as that facility is established under the joint authority of the Board and the FOMC.

In addition, the temporary reciprocal currency arrangements (swap lines) between the Federal Reserve and other central banks have been extended to February 1. The Federal Reserve action to extend the swap lines was taken by the FOMC.

The Federal Reserve also announced changes to certain liquidity programs in light of the improvement in financial conditions and the associated reduction in usage of some facilities. Specifically, the Federal Reserve trimmed the size of upcoming TAF auctions, because the amount of credit extended under that facility has been well below the offered amount. In view of very weak demand at TSLF Schedule 1 auctions and TSLF Options Program auctions over recent months, auctions under these programs will be suspended. The frequency of Schedule 2 TSLF auctions will be reduced to one every four weeks and the offered amount will be reduced. The authorization for the Money Market Investor Funding Facility (MMIFF) was not extended, and an additional administrative criterion was established for use of the AMLF. If necessary in view of evolving market conditions, the Federal Reserve will increase the size of TAF auctions and resume TSLF operations that have been suspended.

WSJ Real Time Economics: Housing Bubble and Consumer Spending

by Calculated Risk on 6/25/2009 11:00:00 AM

Earlier this week, Charles W. Calomiris, Stanley D. Longhofer and William Miles wrote in Real Time Economics that the wealth effect from housing on consumption should be small. Atif Mian and Amir Sufi of the University of Chicago Booth School of Business respond that their data indicate the opposite.I commented on the Calomiris et. al. piece here: The Housing Wealth Effect? and I noted that Mian and Sufi disagreed.

Here are excerpts from Atif Mian and Amir Sufi's piece today:

... In the June 22nd entry for Real Time Economics, Calomiris, Longhofer, and Miles argue that ... “the reaction of consumption to housing wealth changes is probably very small.”

Findings in our research suggest the exact opposite: the rise in house prices from 2002 to 2006 was a main driver of economic growth during this time period, and the subsequent collapse of house prices is likely a main contributor to the historic consumption decline over the past year.

We agree with two key points made by Calomiris, Longhofer, and Miles. First, from the perspective of economic theory, it is not obvious that housing wealth should affect consumption. Second, it is difficult to measure the causal effect of housing wealth on consumption because other economic factors confound the relation. ...

These factors highlight the importance of quality data and sound methodology to estimate the effect of house prices on real economic activity. Our study samples 70,000 consumers in 1998 who were already homeowners at the time. We then follow the borrowing decisions of these households for eleven years until the end of 2008. Our data set represents a major advantage over prior studies; it allows us to see exactly how existing homeowners respond to increases in house prices.

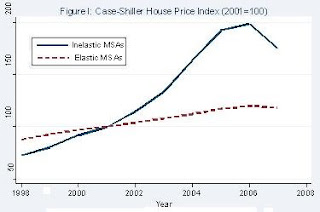

In order to isolate the effect of house prices on consumption, we rely on a simple insight: in response to an equivalent increase in local housing demand, house prices will increase more in cities where, due to geography based factors, the cost of building a house is high. For example, consider a homeowner living in San Francisco and a homeowner living in Atlanta as of 1998. From 2002 to 2006, house prices rose sharply in San Francisco where it is difficult to build additional houses because of the limited geography. In contrast, in Atlanta, where home construction is cheaper, house price growth was moderate. In economics jargon, cities where housing supply is relatively “inelastic” will experience larger movement in house prices relative to “elastic” cities (see Figure I).

Our experimental design exploits this insight in order to test how house prices affect borrowing behavior. The “treatment” group consists of homeowners in inelastic housing supply cities (e.g., San Francisco) that experienced a sharp increase and subsequent collapse of house prices. The “control” group consists of homeowners in elastic housing supply cities (e.g., Atlanta) that experienced little change in house prices.

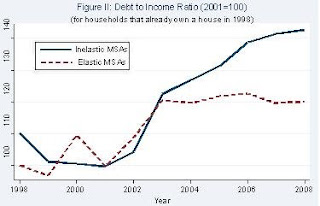

Using this methodology, we find striking results: from 2002 to 2006, homeowners borrowed $0.25 to $0.30 for every $1 increase in their home equity. Our microeconomic estimates suggest a large macroeconomic impact: withdrawals of home equity by households accounted for 2.3% of GDP each year from 2002 to 2006. Figure II illustrates the sharp increase in household leverage for homeowners living in inelastic cities.

A concern with our interpretation is that there are inherently different economic conditions in inelastic versus elastic housing supply cities that may have been responsible for the borrowing patterns we observe. However, several facts suggest that this is not a valid concern. First, inelastic cities do not experience a stronger income growth shock (i.e., a larger shock to their “permanent income”) during the housing boom. Second, the increase in debt among homeowners in high house price growth areas is concentrated in mortgage and home equity related debt.The results of Atif Mian and Amir Sufi fit with what I've observed.

Third, renters in inelastic areas did not experience a larger growth in their total debt. Finally, the effect of house prices on homeowner borrowing is isolated to homeowners with low credit scores and high credit card utilization rates. These “credit-constrained” households respond aggressively to house price growth, whereas the highest credit quality borrowers do not respond at all.

Our results demonstrate that homeowners in high house price areas borrowed heavily against the rise in home equity from 2002 to 2006. We also provide evidence that real outlays were a likely use of borrowed funds. Money withdrawn from home equity was not used to buy new homes, buy investment properties, or invest in financial assets. In fact, homeowners did not even use home equity withdrawals to pay down expensive credit card debt! These facts suggest that consumption and home improvement were the most likely use of borrowed funds, which is consistent with Federal Reserve survey evidence suggesting home equity extraction is used for real outlays.

...

Our analysis of the microeconomic data has led us to the conclusion that the severity of this economic downturn is rooted in the household leverage crisis, which in turn is closely related to the housing market. If the housing market continues to deteriorate, then further de-leveraging of the household sector will likely keep a lid on any rebound in consumption. In other words, the future of consumption and house prices are closely linked.

Bernanke to Testify on BofA and Merrill Lynch at 10 AM ET

by Calculated Risk on 6/25/2009 09:42:00 AM

Fed Chairman Ben Bernanke is to provide testimony before the House Committee on Oversight and Government Reform regarding the Bank of America's acquisition of Merrill Lynch. Might be interesting ...

UPDATE: Here is Bernanke's prepared testimony.

I appreciate the opportunity to discuss the Federal Reserve's role in the acquisition by the Bank of America Corporation of Merrill Lynch & Co., Inc. I believe that the Federal Reserve acted with the highest integrity throughout its discussions with Bank of America regarding that company's acquisition of Merrill Lynch. I will attempt in this testimony to respond to some of the questions that have been raised.Here is the CNBC feed.

And a live feed from C-SPAN.