RSS Feed

RSS Feed by Calculated Risk on 5/12/2022 10:32:00 AM

Thursday, May 12, 2022

Realtor.com Reports Weekly Inventory Up Slightly Year-over-year; First Year-over-year Increase Since 2019

Today, in the Calculated Risk Real Estate Newsletter: Realtor.com Reports Weekly Inventory Up Slightly Year-over-year

Excerpt:

Realtor.com has monthly and weekly data on the existing home market. Here is their weekly report released this morning from Chief Economist Danielle Hale: Weekly Housing Trends View — Data Week Ending May 7, 2022. Note: They have data on list prices, new listings and more, but this focus is on inventory.• Active inventory grew for the first time since 2019. While the size of the improvement rounded to 0%, this week’s data [marks] the first time that inventory figures weren’t lower than the previous year since June 2019. Our April Housing Trends Report showed that the active listings count remained 60 percent below its level right at the onset of the pandemic. This means that for every 5 homes available for sale in the earlier period, today there are just 2. In other words, homes for sale are still limited. However, the switch to growth after nearly 3 years of decline is a step in the right direction, even though inventory continues to lag pre-pandemic normal.Here is a graph of the year-over-year change in inventory according to realtor.com. Note: I corrected a sign error in the data for Feb 26, 2022.

Note the rapid increase in the YoY change, from down 30% at the beginning of the year, to unchanged YoY now. It will be important to watch if that trend continues.

The previous week, inventory was down 3.4% YoY according to Realtor.com. That is close to the 1.6% decline that Altos reported for the similar period. I expect Altos to report a year-over-year increase in inventory on Monday.

There is much more in the article. You can subscribe at https://calculatedrisk.substack.com/

Weekly Initial Unemployment Claims Increase to 203,000

by Calculated Risk on 5/12/2022 08:35:00 AM

The DOL reported:

In the week ending May 7, the advance figure for seasonally adjusted initial claims was 203,000, an increase of 1,000 from the previous week's revised level. The previous week's level was revised up by 2,000 from 200,000 to 202,000. The 4-week moving average was 192,750, an increase of 4,250 from the previous week's revised average. The previous week's average was revised up by 500 from 188,000 to 188,500.The following graph shows the 4-week moving average of weekly claims since 1971.

emphasis added

Click on graph for larger image.

Click on graph for larger image.The dashed line on the graph is the current 4-week average. The four-week average of weekly unemployment claims increased to 192,750.

The previous week was revised up.

Weekly claims were lower than the consensus forecast.

Wednesday, May 11, 2022

Thursday: PPI, Unemployment Claims

by Calculated Risk on 5/11/2022 08:50:00 PM

Thursday:

• At 8:30 AM ET, the initial weekly unemployment claims report will be released. The consensus is for 210 thousand up from 200 thousand last week.

• At 8:30 AM, The Producer Price Index for April from the BLS. The consensus is for a 0.5% increase in PPI, and a 0.6% increase in core PPI.

On COVID (focus on hospitalizations and deaths):

| COVID Metrics | ||||

|---|---|---|---|---|

| Now | Week Ago | Goal | ||

| Percent fully Vaccinated | 66.3% | --- | ≥70.0%1 | |

| Fully Vaccinated (millions) | 220.3 | --- | ≥2321 | |

| New Cases per Day3🚩 | 78,236 | 61,715 | ≤5,0002 | |

| Hospitalized3🚩 | 14,104 | 12,291 | ≤3,0002 | |

| Deaths per Day3 | 326 | 332 | ≤502 | |

| 1 Minimum to achieve "herd immunity" (estimated between 70% and 85%). 2my goals to stop daily posts, 37-day average for Cases, Currently Hospitalized, and Deaths 🚩 Increasing 7-day average week-over-week for Cases, Hospitalized, and Deaths ✅ Goal met. | ||||

Click on graph for larger image.

Click on graph for larger image.This graph shows the daily (columns) and 7-day average (line) of deaths reported.

Average daily deaths bottomed in July 2021 at 214 per day.

2nd Look at Local Housing Markets in April; Inventory increasing, No Surge in New Listings

by Calculated Risk on 5/11/2022 12:48:00 PM

Today, in the Calculated Risk Real Estate Newsletter: 2nd Look at Local Housing Markets in April

A brief excerpt:

Here is a summary of active listings for these housing markets in April. Note: Inventory usually increases seasonally in April, so some month-over-month (MoM) increase is not surprising.There is much more in the article. You can subscribe at https://calculatedrisk.substack.com/

Inventory was up 17.9% in April MoM from March, and up 4.9% year-over-year (YoY). Eight of 15 markets were up YoY.

Active inventory in these markets were down 19% YoY in February, and down 4.8% YoY in March, so this is a significant change from February and March. This is another step towards a more balanced market, but inventory levels are still very low.

Notes for all tables:

1) New additions to table in BOLD.

2) Northwest (Seattle), North Texas (Dallas) and Santa Clara (San Jose), Jacksonville, Source: Northeast Florida Association of REALTORS®

3) Totals do not include Atlanta (included in state total).

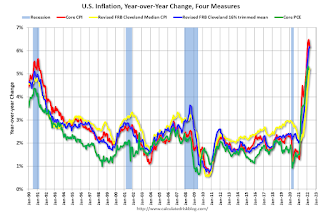

Cleveland Fed: Median CPI increased 0.5% and Trimmed-mean CPI increased 0.4% in April

by Calculated Risk on 5/11/2022 11:18:00 AM

The Cleveland Fed released the median CPI and the trimmed-mean CPI this morning:

According to the Federal Reserve Bank of Cleveland, the median Consumer Price Index rose 0.5% in April. The 16% trimmed-mean Consumer Price Index increased 0.4% in April. "The median CPI and 16% trimmed-mean CPI are measures of core inflation calculated by the Federal Reserve Bank of Cleveland based on data released in the Bureau of Labor Statistics’ (BLS) monthly CPI report".

Note: The Cleveland Fed released the median CPI details here: "Used Cars" were down slightly annualized in April, and this will likely show further declines in coming months. Motor fuel was down 51% annualized in April after increasing sharply in March

Note that Owners' Equivalent Rent and Rent of Primary Residence account for almost 1/3 of median CPI, and these measures were up around 5% to 6% annualized in April.

Click on graph for larger image.

Click on graph for larger image.

This graph shows the year-over-year change for these four key measures of inflation.

Click on graph for larger image.

Click on graph for larger image.This graph shows the year-over-year change for these four key measures of inflation.

On a year-over-year basis, the median CPI rose 5.2%, the trimmed-mean CPI rose 6.2%, and the CPI less food and energy rose 6.2%. Core PCE is for March and increased 5.2% year-over-year.

BLS: CPI increased 0.3% in April; Core CPI increased 0.6%

by Calculated Risk on 5/11/2022 08:33:00 AM

The Consumer Price Index for All Urban Consumers (CPI-U) increased 0.3 percent in April on a seasonally adjusted basis after rising 1.2 percent in March, the U.S. Bureau of Labor Statistics reported today. Over the last 12 months, the >all items index increased 8.3 percent before seasonal adjustment.The consensus was for 0.2% increase in CPI (up 8.1% YoY), and a 0.4% increase in core CPI (up 6.1% YoY). Both were above expectations. I'll post a graph later today after the Cleveland Fed releases the median and trimmed-mean CPI.

Increases in the indexes for shelter, food, airline fares, and new vehicles were the largest contributors to the seasonally adjusted all items increase. The food index rose 0.9 percent over the month as the food at home index rose 1.0 percent. The energy index declined in April after rising in recent months. The index for gasoline fell 6.1 percent over the month, offsetting increases in the indexes for natural gas and electricity.

The index for all items less food and energy rose 0.6 percent in April following a 0.3-percent advance in March. Along with indexes for shelter, airline fares, and new vehicles, the indexes for medical care, recreation, and household furnishings and operations all increased in April. The indexes for apparel, communication, and used cars and trucks all declined over the month.

The all items index increased 8.3 percent for the 12 months ending April, a smaller increase than the 8.5-percent figure for the period ending in March. The all items less food and energy index rose 6.2 percent over the last 12 months. The energy index rose 30.3 percent over the last year, and the food index increased 9.4 percent, the largest 12-month increase since the period ending April 1981.

emphasis added

MBA: Mortgage Applications Increase in Latest Weekly Survey

by Calculated Risk on 5/11/2022 07:00:00 AM

From the MBA: Mortgage Applications Increase in Latest MBA Weekly Survey

Mortgage applications increased 2.0 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending May 6, 2022.

... The Refinance Index decreased 2 percent from the previous week and was 72 percent lower than the same week one year ago. The seasonally adjusted Purchase Index increased 5 percent from one week earlier. The unadjusted Purchase Index increased 5 percent compared with the previous week and was 8 percent lower than the same week one year ago.

“The increase in mortgage applications last week was driven by a strong gain in application activity for conventional and government purchase loans, even as mortgage rates rose to their highest level – 5.53 percent – since 2009. Despite a slow start to this year’s spring home buying season, prospective buyers are showing some resiliency to higher rates. Purchase activity has now increased for two straight weeks,” said Joel Kan, MBA’s Associate Vice President of Economic and Industry Forecasting. “More borrowers continue to utilize ARMs to combat higher rates. The share of ARMs increased to 11 percent of overall loans and to 19 percent by dollar volume.”

Added Kan, “The rapid rise in mortgages rates continues to hit the refinance market, with activity 70 percent below a year ago. Most homeowners refinanced to lower rates in the past two years.”

...

The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($647,200 or less) increased to 5.53 percent from 5.36 percent, with points increasing to 0.73 from 0.63 (including the origination fee) for 80 percent loan-to-value ratio (LTV) loans

emphasis added

Click on graph for larger image.

Click on graph for larger image.The first graph shows the refinance index since 1990.

With higher mortgage rates, the refinance index has declined sharply over the last several months.

The refinance index just above last week, and that was the lowest level since December 2018.

The second graph shows the MBA mortgage purchase index

According to the MBA, purchase activity is down 8% year-over-year unadjusted.

According to the MBA, purchase activity is down 8% year-over-year unadjusted.Note: Red is a four-week average (blue is weekly).

Tuesday, May 10, 2022

Wednesday: CPI

by Calculated Risk on 5/10/2022 09:00:00 PM

Wednesday:

• At 7:00 AM ET, The Mortgage Bankers Association (MBA) will release the results for the mortgage purchase applications index.

• At 8:30 AM, The Consumer Price Index for April from the BLS. The consensus is for 0.2% increase in CPI (up 8.1% YoY), and a 0.4% increase in core CPI (up 6.1% YoY).

On COVID (focus on hospitalizations and deaths):

| COVID Metrics | ||||

|---|---|---|---|---|

| Now | Week Ago | Goal | ||

| Percent fully Vaccinated | 66.3% | --- | ≥70.0%1 | |

| Fully Vaccinated (millions) | 220.2 | --- | ≥2321 | |

| New Cases per Day3🚩 | 74,712 | 60,554 | ≤5,0002 | |

| Hospitalized3🚩 | 13,538 | 12,047 | ≤3,0002 | |

| Deaths per Day3 | 323 | 331 | ≤502 | |

| 1 Minimum to achieve "herd immunity" (estimated between 70% and 85%). 2my goals to stop daily posts, 37-day average for Cases, Currently Hospitalized, and Deaths 🚩 Increasing 7-day average week-over-week for Cases, Hospitalized, and Deaths ✅ Goal met. | ||||

Click on graph for larger image.

Click on graph for larger image.This graph shows the daily (columns) and 7-day average (line) of deaths reported.

Average daily deaths bottomed in July 2021 at 214 per day.

Mortgage Originations by Credit Score and Age

by Calculated Risk on 5/10/2022 12:01:00 PM

Today, in the Calculated Risk Real Estate Newsletter: Mortgage Originations by Credit Score and Age

A brief excerpt:

The NY Fed released the Q1 Quarterly Report on Household Debt and Credit this morning. Here are a couple of charts from the report.There is much more in the article. You can subscribe at https://calculatedrisk.substack.com/

The first graph shows mortgage originations by credit score (this includes both purchase and refinance). Look at the difference in credit scores in the recent period compared to the during the bubble years (2003 through 2006). Recently there have been almost no originations for borrowers with credit scores below 620, and few below 660. A significant majority of recent originations have been to borrowers with credit score above 760.

Solid underwriting is a key reason I’ve argued Don't Compare the Current Housing Boom to the Bubble and Bust, Look instead at the 1978 to 1982 period for lessons.

From the NY Fed:

Mortgage originations, measured as appearances of new mortgages on consumer credit reports and which include refinances, were at $859 billion in 2022Q1. This represented a decrease from the high volumes seen during 2021, but still was $197 billion higher than the volume seen in 2020Q1, just before the pandemic hit.

The median credit score of newly originated mortgages declined again, to 776, down from a series high in 2021Q1 of 788. Yet, credit scores on newly originated mortgages remain very high and reflect continuing high lending standards.

NY Fed Q1 Report: Total Household Debt Increases to $15.8 trillion

by Calculated Risk on 5/10/2022 11:10:00 AM

From the NY Fed: Total Household Debt Increases in Q1 2022, Driven by Mortgage and Auto Balances

The Federal Reserve Bank of New York’s Center for Microeconomic Data today issued its Quarterly Report on Household Debt and Credit. The Report shows a solid increase in total household debt in the first quarter of 2022, increasing by $266 billion (1.7%) to $15.84 trillion. Balances now stand $1.7 trillion higher than at the end of 2019, before the COVID-19 pandemic. The report is based on data from the New York Fed’s nationally representative Consumer Credit Panel.

Mortgage balances rose by $250 billion in the first quarter of 2022 and stood at $11.18 trillion at the end of March. In line with seasonal trends typically seen at the start of the year, credit card balances declined by $15 billion. Credit card balances are still $71 billion higher than Q1 2021 and represent a substantial year-over-year increase. Auto loan balances increased by $11 billion in the first quarter, while student loan balances increased by $14 billion and now stand at $1.59 trillion. In total, non-housing balances grew by $17 billion.

Mortgage and auto loan originations both declined in the first quarter, after historically high volumes in 2021. Mortgage originations were at $859 billion, representing a decline from the high volumes seen during 2021, yet still $197 billion higher than in Q1 2020, right before the pandemic hit the United States. The volume of newly originated auto loans was $177 billion during the first quarter, primarily reflecting an increase in auto prices. Aggregate limits on credit card accounts increased by $64 billion and now stand at $4.12 trillion–$224 billion above the pre-pandemic level.

emphasis added

Click on graph for larger image.

Click on graph for larger image.Here are three graphs from the report:

The first graph shows aggregate consumer debt increased in Q1. Household debt previously peaked in 2008 and bottomed in Q3 2013. Unlike following the great recession, there wasn't a huge decline in debt during the pandemic.

From the NY Fed:

Aggregate household debt balances increased by $266 billion in the first quarter of 2022, a 1.7% rise from 2021Q4. Balances now stand at $15.84 trillion, $1.7 trillion higher than at the end of 2019, just before the Covid pandemic.

The second graph shows the percent of debt in delinquency.

The second graph shows the percent of debt in delinquency.The overall delinquency rate was unchanged in Q1. From the NY Fed:

Aggregate delinquency rates were unchanged in the first quarter of 2022 and remain very low, after declining sharply through the beginning of the pandemic. Delinquency rates have been low in part due to forbearances (provided by both the CARES Act and voluntarily offered by lenders), which protect borrowers’ credit records from the reporting of skipped or deferred payments. Although these forbearances have ended for most types of debts, the pause on student loan payments remains in place. As of late March, 2.7% of outstanding debt was in some stage of delinquency, a 2.0 percentage point decrease from the fourth quarter of 2019, just before the COVID-19 pandemic hit the United States.There is much more in the report.

Second Home Market: South Lake Tahoe in April

by Calculated Risk on 5/10/2022 08:11:00 AM

With the pandemic, there was a surge in 2nd home buying.

I'm looking at data for some second home markets - and I'm tracking those markets to see if there is an impact from lending changes like the recent FHFA Targeted Increases to Enterprise Pricing Framework, rising mortgage rates or the easing of the pandemic.

This graph is for South Lake Tahoe since 2004 through April 2022, and shows inventory (blue), and the year-over-year (YoY) change in the median price (12-month average).

Note: The median price is distorted by the mix, but this is the available data.

Click on graph for larger image.

Click on graph for larger image.

Following the housing bubble, prices declined for several years in South Lake Tahoe, with the median price falling about 50% from the bubble peak.

Currently inventory is still very low, but up from the record low set in February 2022, and up slightly year-over-year. Prices are up 12.7% YoY (but the YoY change has been trending down).

This will be interesting to watch, but so far there isn't little evidence of a 2nd home slowdown in these numbers.

Monday, May 09, 2022

Tuesday: Q1 Quarterly Report on Household Debt and Credit

by Calculated Risk on 5/09/2022 09:10:00 PM

From Matthew Graham at Mortgage News Daily: Rates Start High, But Improved Significantly By The Afternoon

2022 has been the year of volatility for mortgage rates with most of the swings resulting in successive runs to long-term highs. Every now and then, however, rates have a good day. Today was one of those days. [30 year fixed 5.52%]Tuesday:

emphasis added

• At 6:00 AM ET, NFIB Small Business Optimism Index for April.

• At 11:00 AM, NY Fed: Q1 Quarterly Report on Household Debt and Credit

On COVID (focus on hospitalizations and deaths):

| COVID Metrics | ||||

|---|---|---|---|---|

| Now | Week Ago | Goal | ||

| Percent fully Vaccinated | 66.3% | --- | ≥70.0%1 | |

| Fully Vaccinated (millions) | 220.2 | --- | ≥2321 | |

| New Cases per Day3🚩 | 66,564 | 58,569 | ≤5,0002 | |

| Hospitalized3🚩 | 12,466 | 11,823 | ≤3,0002 | |

| Deaths per Day3 | 323 | 324 | ≤502 | |

| 1 Minimum to achieve "herd immunity" (estimated between 70% and 85%). 2my goals to stop daily posts, 37-day average for Cases, Currently Hospitalized, and Deaths 🚩 Increasing 7-day average week-over-week for Cases, Hospitalized, and Deaths ✅ Goal met. | ||||

Click on graph for larger image.

Click on graph for larger image.This graph shows the daily (columns) and 7-day average (line) of deaths reported.

Average daily deaths bottomed in July 2021 at 214 per day.

Homebuilder Comments in April: “Demand is slowing", "Investors pulling back"

by Calculated Risk on 5/09/2022 03:09:00 PM

Today, in the Calculated Risk Real Estate Newsletter: Homebuilder Comments in April: “Demand is slowing", "Investors pulling back"

A brief excerpt:

Read these comments. These are clear signs of a slowdown.There is much more in the article. You can subscribe at https://calculatedrisk.substack.com/

Some homebuilder comments courtesy of Rick Palacios Jr., Director of Research at John Burns Real Estate Consulting (a must follow for housing on twitter!):

...

#Dallas builder: “Interest lists are shrinking or buyers are truly pausing.”

...

#SanAntonio builder: “Traffic has been cut in half since the hike in rates.”

#Raleigh builder: “Investor activity has slowed dramatically.”

...

Allentown builder: “Double hit of higher home prices and higher mortgage interest rates clearly has reduced the number of qualified buyers. Our waiting list is almost zero as of April 30th.”

#Philadelphia builder: “Between higher interest rates and higher sales prices, along with high gas prices and a volatile stock market, we’re seeing a pullback in our sales.”

#Tampa builder: “We’ve seen a significant shift in buyer behavior in the last 30 days. Florida was on fire and pricing has really come to a high point, and people are not willing to pay the prices anymore.”

#Indianapolis builder: “Traffic has significantly declined and people have paused on moving forward with purchases.”

Fed Survey: Banks reported Eased Standards, Weaker Demand for Residential Real Estate Loans

by Calculated Risk on 5/09/2022 02:06:00 PM

From the Federal Reserve: The April 2022 Senior Loan Officer Opinion Survey on Bank Lending Practices

The April 2022 Senior Loan Officer Opinion Survey on Bank Lending Practices addressed changes in the standards and terms on, and demand for, bank loans to businesses and households over the past three months, which generally correspond to the first quarter of 2022.

Regarding loans to businesses, respondents to the survey reported, on balance, unchanged standards for commercial and industrial (C&I) loans to firms of all sizes, after having eased them over the previous four quarters, while demand strengthened over the first quarter. Meanwhile, banks reported unchanged standards and demand for most commercial real estate (CRE) loan categories except for those secured by multifamily residential properties, for which they eased standards and demand strengthened on net.

Banks also responded to a set of special questions about changes in lending policies and demand for CRE loans over the past year. Banks reportedly eased some lending terms across all CRE loan categories, including the maximum loan size and maturity, the spread of loan rates over their cost of funds, the length of interest-only periods, and the market areas served.

For loans to households, banks eased standards across most categories of residential real estate (RRE) loans and home equity lines of credit (HELOCs) over the first quarter, while also reporting weaker demand for all types of RRE loans but stronger demand for HELOCs on net. In addition, banks eased standards for card loans and auto loans, while demand reportedly strengthened for all consumer loan types over the first quarter

emphasis added

Click on graph for larger image.

Click on graph for larger image.This graph on Residential Real Estate lending is from the Senior Loan Officer Survey Charts.

This shows that banks have eased standards for residential real estate.

The second graph shows demand for residential real estate.

This was was Q1. Demand is probably dropping sharply in Q2.

This was was Q1. Demand is probably dropping sharply in Q2.

Housing Market: Where it's at. Where it's going. May 2022 Update

by Calculated Risk on 5/09/2022 11:08:00 AM

Today, in the Calculated Risk Real Estate Newsletter: Housing Market: Where it's at. Where it's going.

A brief excerpt:

House prices are up 20% year-over-year. Inventory is near record lows. And real estate agents are still selling homes well above list price. And on credit, lending standards have been reasonably solid, and mortgage delinquencies are very low.There is much more in the article. You can subscribe at https://calculatedrisk.substack.com/

However, mortgage rates are up sharply (from 3% six months ago to 5.64% today), and we are starting to see an increase in inventory levels. House prices are too high based on fundamentals like price-to-income and price-to-rent. And some investors appear to be pulling back due to higher cap rates, and some builders are reporting buyers actually want to negotiate on price!

...

On mortgage rates, it is the change in monthly payments that impacts housing. Monthly payments include principal, interest, taxes, insurance (PITI), and sometimes HOA fees (Homeowners Association). We could also include maintenance, utilities and other costs. The following graph shows the year-over-year change in principal & interest (P&I) assuming a fixed loan amount since 1977. Currently P&I is up about 35% year-over-year for a fixed amount (this doesn’t take into account the change in house prices).

The last time we saw an increase like this in monthly payments was in the ‘78 to’82 period. This is one reason I’ve been suggesting Housing: Don't Compare the Current Housing Boom to the Bubble and Bust, Look instead at the 1978 to 1982 period for lessons.

Housing Inventory May 9th Update: Inventory Down 1.6% Year-over-Year

by Calculated Risk on 5/09/2022 09:00:00 AM

Tracking existing home inventory is very important in 2022.

Inventory usually declines in the winter, and then increases in the spring. Inventory bottomed seasonally at the beginning of March 2022 and is now up 27% since then.

Click on graph for larger image in graph gallery.

Click on graph for larger image in graph gallery.

This inventory graph is courtesy of Altos Research.

As of May 6th, inventory was at 305 thousand (7-day average), compared to 292 thousand the prior week. Inventory was up 4.5% from the previous week.

Last year inventory bottomed seasonally in April 2021 - very late in the year. This year, by this measure, inventory bottomed seasonally at the beginning of March.

Inventory is still very low. Compared to the same week in 2021, inventory is down 1.6% from 310 thousand, but compared to the same week in 2020, and inventory is down 58.3% from 732 thousand. Compared to 3 years ago, inventory is down 66.1% from 902 thousand.

Last year inventory bottomed seasonally in April 2021 - very late in the year. This year, by this measure, inventory bottomed seasonally at the beginning of March.

Inventory is still very low. Compared to the same week in 2021, inventory is down 1.6% from 310 thousand, but compared to the same week in 2020, and inventory is down 58.3% from 732 thousand. Compared to 3 years ago, inventory is down 66.1% from 902 thousand.

Here are the inventory milestones I’m watching for with the Altos data:

1. The seasonal bottom (already happened on March 4th for Altos)✅

2. Inventory up year-over-year (likely next week)

3. Inventory up compared to two years ago (currently down 58% according to Altos)

4. Inventory back to 1999 levels (currently down 66%).

For the second milestone, here is a table of the year-over-year change by week since the beginning of the year.

1. The seasonal bottom (already happened on March 4th for Altos)✅

2. Inventory up year-over-year (likely next week)

3. Inventory up compared to two years ago (currently down 58% according to Altos)

4. Inventory back to 1999 levels (currently down 66%).

For the second milestone, here is a table of the year-over-year change by week since the beginning of the year.

| Week Ending | YoY Change |

|---|---|

| 12/31/2021 | -30.0% |

| 1/7/2022 | -26.0% |

| 1/14/2022 | -28.6% |

| 1/21/2022 | -27.1% |

| 1/28/2022 | -25.9% |

| 2/4/2022 | -27.9% |

| 2/11/2022 | -27.5% |

| 2/18/2022 | -25.8% |

| 2/25/2022 | -24.9% |

| 3/4/2022 | -24.2% |

| 3/11/2022 | -21.7% |

| 3/18/2022 | -21.7% |

| 3/25/2022 | -19.0% |

| 4/1/2022 | -17.6% |

| 4/8/2022 | -14.8% |

| 4/15/2022 | -13.1% |

| 4/22/2022 | -11.2% |

| 4/29/2022 | -4.9% |

| 5/6/2022 | -1.6% |

Here is a graph of the year-over-year change in the Altos data.

The blue trend line is from the beginning of the year, and the red trend line is over the last 8 weeks.

Currently it appears inventory will be up year-over-year next week.

Mike Simonsen discusses this data regularly on Youtube.

Four High Frequency Indicators for the Economy

by Calculated Risk on 5/09/2022 08:27:00 AM

These indicators are mostly for travel and entertainment. It is interesting to watch these sectors recover as the pandemic subsides. Note: Apple has discontinued "Apple mobility", and restaurant traffic is mostly back to normal.

The TSA is providing daily travel numbers.

This data is as of May 8th.

Click on graph for larger image.

Click on graph for larger image.This data shows the 7-day average of daily total traveler throughput from the TSA for 2019 (Light Blue), 2020 (Black), 2021 (Blue) and 2022 (Red).

The dashed line is the percent of 2019 for the seven-day average.

The 7-day average is down 11.7% from the same day in 2019 88.3% of 2019). (Dashed line)

Air travel has been moving sideways over the last two months, off about 10% from 2019.

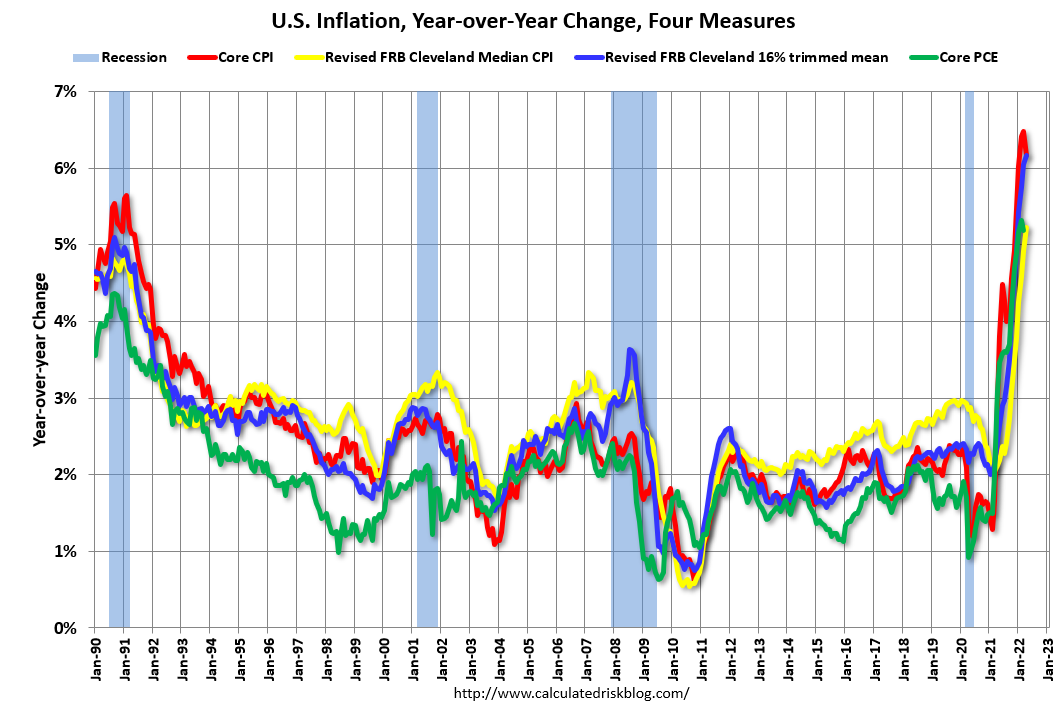

This data shows domestic box office for each week and the median for the years 2016 through 2019 (dashed light blue).

This data shows domestic box office for each week and the median for the years 2016 through 2019 (dashed light blue). Black is 2020, Blue is 2021 and Red is 2022.

The data is from BoxOfficeMojo through May 5th.

Note that the data is usually noisy week-to-week and depends on when blockbusters are released.

Movie ticket sales were at $87 million last week, down about 70% from the median for the week.

Note that the data is usually noisy week-to-week and depends on when blockbusters are released.

Movie ticket sales were at $87 million last week, down about 70% from the median for the week.

This graph shows the seasonal pattern for the hotel occupancy rate using the four-week average.

This graph shows the seasonal pattern for the hotel occupancy rate using the four-week average. The red line is for 2022, black is 2020, blue is the median, and dashed light blue is for 2021.

This data is through April 30th. The occupancy rate was down 3.4% compared to the same week in 2019.

The 4-week average of the occupancy rate is at the median rate for the previous 20 years (Blue).

Notes: Y-axis doesn't start at zero to better show the seasonal change.

Notes: Y-axis doesn't start at zero to better show the seasonal change.

The 4-week average of the occupancy rate will now mostly move sideways seasonally until the summer.

Here is some interesting data on New York subway usage (HT BR).

This graph is from Todd W Schneider.

This graph is from Todd W Schneider. This graph shows how much MTA traffic has recovered in each borough (Graph starts at first week in January 2020 and 100 = 2019 average).

Manhattan is at about 39% of normal.

This data is through Friday, May 6th.

He notes: "Data updates weekly from the MTA’s public turnstile data, usually on Saturday mornings".

Sunday, May 08, 2022

Sunday Night Futures

by Calculated Risk on 5/08/2022 06:40:00 PM

Weekend:

• Schedule for Week of May 8, 2022

Monday:

• At 2:00 PM ET, Senior Loan Officer Opinion Survey on Bank Lending Practices for April.

From CNBC: Pre-Market Data and Bloomberg futures S&P 500 are down 25 and DOW futures are down 170 (fair value).

Oil prices were up over the last week with WTI futures at $109.60 per barrel and Brent at $112.24 per barrel. A year ago, WTI was at $66 and Brent was at $69 - so WTI oil prices are up 70% year-over-year.

Here is a graph from Gasbuddy.com for nationwide gasoline prices. Nationally prices are at $4.31 per gallon. A year ago prices were at $2.95 per gallon, so gasoline prices are up $1.36 per gallon year-over-year.

Vehicle Sales Mix and Heavy Trucks

by Calculated Risk on 5/08/2022 09:49:00 AM

It will be interesting to see if high gasoline prices will lead to a higher percentage of passenger car sales.

This graph shows the percent of light vehicle sales between passenger cars and trucks / SUVs through April 2022.

Over time the mix has changed more and more towards light trucks and SUVs.

Over time the mix has changed more and more towards light trucks and SUVs.Only when oil prices are high, does the trend slow or reverse.

The percent of light trucks and SUVs was at 79.0% in April 2022 - just below the record high percentage of 80.0% last October.

The second graph shows heavy truck sales since 1967 using data from the BEA. The dashed line is the April 2022 seasonally adjusted annual sales rate (SAAR).

Heavy truck sales really collapsed during the great recession, falling to a low of 180 thousand SAAR in May 2009. Then heavy truck sales increased to a new all-time high of 563 thousand SAAR in September 2019.

Heavy truck sales really collapsed during the great recession, falling to a low of 180 thousand SAAR in May 2009. Then heavy truck sales increased to a new all-time high of 563 thousand SAAR in September 2019.Note: "Heavy trucks - trucks more than 14,000 pounds gross vehicle weight."

Heavy truck sales really declined at the beginning of the pandemic, falling to a low of 299 thousand SAAR in May 2020.

Heavy truck sales were at 467 thousand SAAR in April, unchanged from March, and down 3% from 482 thousand SAAR in April 2021.

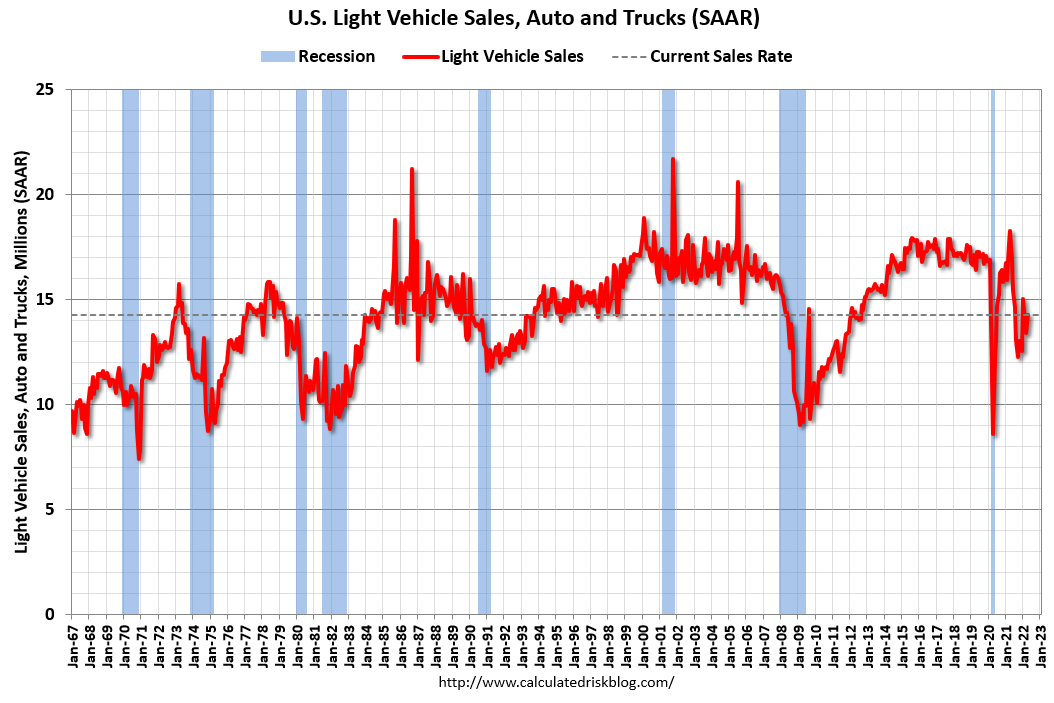

The last graph shows light vehicle sales since the BEA started keeping data in 1967. The BEA reported sales of 14.29 million SAAR in April 2022 (Seasonally Adjusted Annual Rate), up 6.6% from the March sales rate, and down 21.9% from April 2021.

The last graph shows light vehicle sales since the BEA started keeping data in 1967. The BEA reported sales of 14.29 million SAAR in April 2022 (Seasonally Adjusted Annual Rate), up 6.6% from the March sales rate, and down 21.9% from April 2021.The impact of COVID-19 was significant, and April 2020 was the worst month. After April 2020, sales increased, and were close to sales in 2019 (the year before the pandemic).

However, sales decreased late last year due to supply issues. It appears the "supply chain bottom" was in September 2021, and sales in April were above the consensus forecast of 13.8 million SAAR.

Sales are still weak but picking up.

Saturday, May 07, 2022

Real Estate Newsletter Articles this Week

by Calculated Risk on 5/07/2022 02:11:00 PM

At the Calculated Risk Real Estate Newsletter this week:

• Housing: "What Killed the Home ATM in 2006?"

• Black Knight Mortgage Monitor: Record Low Delinquencies, "Home Affordability Nears All-Time Low"

• Rent Increases Up Sharply Year-over-year, Pace may be slowing

• Denver Real Estate in April: Active Inventory up Sharply

• Lawler: Mortgage/Treasury Spreads, Part I

• 1st Look at Local Housing Markets in April Realtor.com shows active inventory down only 3% year-over-year

This is usually published 4 to 6 times a week and provides more in-depth analysis of the housing market.

The blog will continue as always!

You can subscribe at https://calculatedrisk.substack.com/

Most content is available for free (and no Ads), but please subscribe!