RSS Feed

RSS Feed by Calculated Risk on 6/03/2022 09:01:00 PM

Friday, June 03, 2022

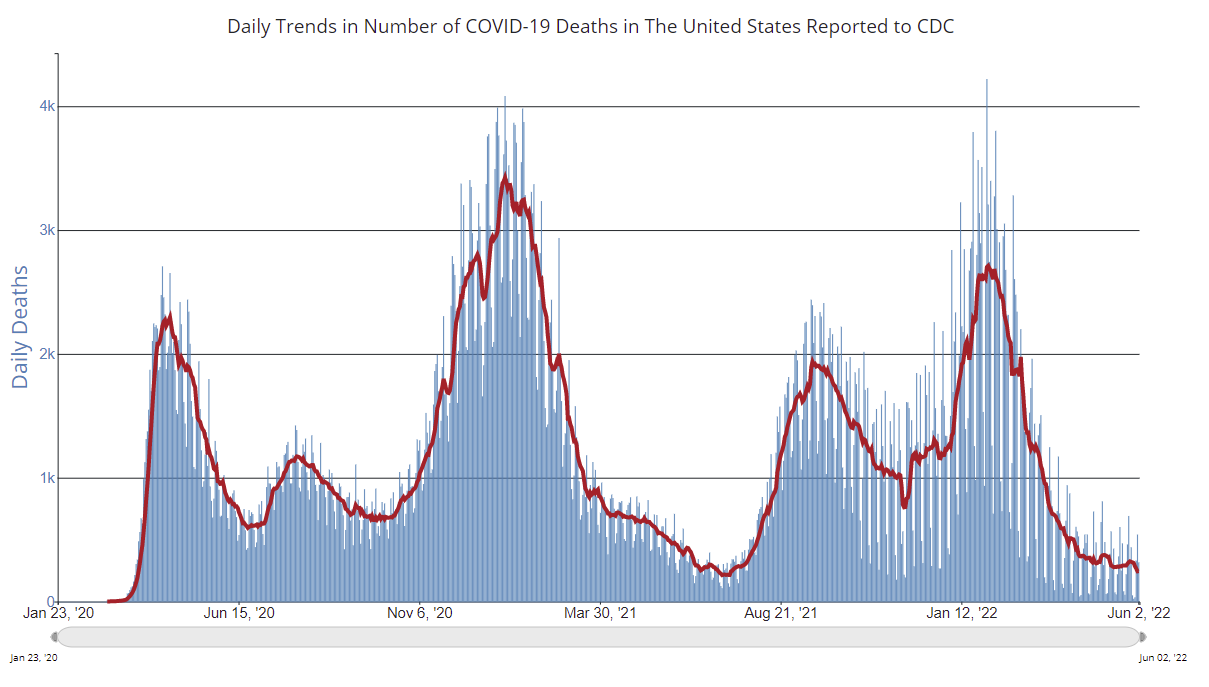

COVID June 3, 2022: Hospitalizations Increasing

On COVID (focus on hospitalizations and deaths):

| COVID Metrics | ||||

|---|---|---|---|---|

| Now | Week Ago | Goal | ||

| Percent fully Vaccinated | 66.7% | --- | ≥70.0%1 | |

| Fully Vaccinated (millions) | 221.4 | --- | ≥2321 | |

| New Cases per Day3 | 99,289 | 110,387 | ≤5,0002 | |

| Hospitalized3🚩 | 21,765 | 20,521 | ≤3,0002 | |

| Deaths per Day3 | 246 | 325 | ≤502 | |

| 1 Minimum to achieve "herd immunity" (estimated between 70% and 85%). 2my goals to stop daily posts, 37-day average for Cases, Currently Hospitalized, and Deaths 🚩 Increasing 7-day average week-over-week for Cases, Hospitalized, and Deaths ✅ Goal met. | ||||

Click on graph for larger image.

Click on graph for larger image.This graph shows the daily (columns) and 7-day average (line) of deaths reported.

Average daily deaths bottomed in July 2021 at 214 per day.

Realtor.com Reports Weekly Inventory Up 11% Year-over-year

by Calculated Risk on 6/03/2022 03:14:00 PM

Realtor.com has monthly and weekly data on the existing home market. Here is their weekly report released this morning from Chief Economist Danielle Hale: Weekly Housing Trends View — Data Week Ending May 28, 2022. Note: They have data on list prices, new listings and more, but this focus is on inventory.

• Active inventory continued to grow, rising 11% above one year ago. In a few short weeks, we’ve observed a significant turnaround in the number of homes available for sale, going from essentially flat at the beginning of May weeks ago to +11% in this data from the last week of the month. This is helping to rebalance the housing market, but the trend must be understood in context. Our May Housing Trends Report showed that the active listings count remained nearly 50 percent below its level at the beginning of the pandemic. In other words, home shoppers continue to see a historically low number of homes for sale.

Here is a graph of the year-over-year change in inventory according to realtor.com. Note: I corrected a sign error in the data for Feb 26, 2022.

Here is a graph of the year-over-year change in inventory according to realtor.com. Note: I corrected a sign error in the data for Feb 26, 2022.Note the rapid increase in the YoY change, from down 30% at the beginning of the year, to up 11% YoY now. It will be important to watch if that trend continues.

The second graph is from the May Housing Trends Report referenced above.

This shows realtor.com's estimate of active inventory over the last six years.

Note that inventory was declining rapidly for most of 2020, and it is very likely that inventory will be up compared to 2020 later this year.

Q2 GDP Forecasts: Around 3.0%

by Calculated Risk on 6/03/2022 03:00:00 PM

From BofA:

We continue to track 3.0% qoq saar growth for 2Q. Weaker than expected vehicle sales were offset by better inventories and capex spending [June 3 estimate]From Goldman:

emphasis added

We boosted our Q2 GDP tracking estimate by 0.2pp to +3.0% (qoq ar). [June 1 estimate]And from the Altanta Fed: GDPNow

The GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the second quarter of 2022 is 1.3 percent on June 1, down from 1.9 percent on May 27. [June 1 estimate]

When will House Price Growth Slow?

by Calculated Risk on 6/03/2022 12:32:00 PM

Today, in the Calculated Risk Real Estate Newsletter: When will House Price Growth Slow?

A brief excerpt:

Most analysts expect house price growth to slow sharply in coming months. For example, a few weeks ago, I wrote: What will Happen with House Prices?Some answers in the article. You can subscribe at https://calculatedrisk.substack.com/

However, the most recent Case-Shiller report showed house prices were up a record 20.6% year-over-year (YoY). This report was for March (a three-month average of January, February and March prices).

And, according to Zillow research, house prices will be up even more YoY in the April Case-Shiller National Index (to be released on June 28th. The Zillow forecast is for the YoY change for the Case-Shiller National index to be a record 20.8% in April.

...

Why are prices still up sharply year-over-year?

Comments on May Employment Report

by Calculated Risk on 6/03/2022 09:31:00 AM

The headline jobs number in the May employment report was above expectations, however employment for the previous two months was revised down by 22,000. The participation rate and the employment-population ratio both increased slightly, and the unemployment rate was unchanged at 3.6%.

Excluding leisure and hospitality, the economy has more than added back all the jobs lost at the beginning of the pandemic. Leisure and hospitality gained 84 thousand jobs in May. At the beginning of the pandemic, in March and April of 2020, leisure and hospitality lost 8.20 million jobs, and are now down 1.35 million jobs since February 2020. So, leisure and hospitality has now added back about 84% all of the jobs lost in March and April 2020.

Construction employment increased 36 thousand and is now 40 thousand above the pre-pandemic level.

Manufacturing added 18 thousand jobs and is just 17 thousand below the pre-pandemic level.

Earlier: May Employment Report: 390 thousand Jobs, 3.6% Unemployment Rate

In May, the year-over-year employment change was 6.5 million jobs.

Permanent Job Losers

Click on graph for larger image.

Click on graph for larger image.

This graph shows permanent job losers as a percent of the pre-recession peak in employment through the report today.

In May, the year-over-year employment change was 6.5 million jobs.

Permanent Job Losers

Click on graph for larger image.

Click on graph for larger image.This graph shows permanent job losers as a percent of the pre-recession peak in employment through the report today.

This data is only available back to 1994, so there is only data for three recessions.

In May, the number of permanent job losers was unchanged at 1.386 million from 1.386 million in the previous month.

In May, the number of permanent job losers was unchanged at 1.386 million from 1.386 million in the previous month.

These jobs were likely the hardest to recover, so it is a positive that the number of permanent job losers is essentially back to pre-recession levels.

Prime (25 to 54 Years Old) Participation

Since the overall participation rate has declined due to cyclical (recession) and demographic (aging population, younger people staying in school) reasons, here is the employment-population ratio for the key working age group: 25 to 54 years old.

Since the overall participation rate has declined due to cyclical (recession) and demographic (aging population, younger people staying in school) reasons, here is the employment-population ratio for the key working age group: 25 to 54 years old.The 25 to 54 participation rate increased in May to 82.6% from 82.4% in April, and the 25 to 54 employment population ratio increased to 80.0% from 79.9% the previous month.

Both are slightly below the pre-pandemic levels and indicate almost all of the prime age workers have returned to the labor force.

Part Time for Economic Reasons

From the BLS report:

From the BLS report:

These workers are included in the alternate measure of labor underutilization (U-6) that increased to 7.1% from 7.0% in the previous month. This is down from the record high in April 22.9% for this measure since 1994. This measure is close to the 7.0% in February 2020 (pre-pandemic).

Unemployed over 26 Weeks

This graph shows the number of workers unemployed for 27 weeks or more.

This graph shows the number of workers unemployed for 27 weeks or more.

According to the BLS, there are 1.356 million workers who have been unemployed for more than 26 weeks and still want a job, down from 1.483 million the previous month.

This does not include all the people that left the labor force.

Summary:

The headline monthly jobs number was above expectations; however, the previous two months were revised down by 22,000 combined.

Part Time for Economic Reasons

From the BLS report:

From the BLS report:"The number of persons employed part time for economic reasons increased by 295,000 to 4.3 million in May, reflecting an increase in the number of persons whose hours were cut due to slack work or business conditions. The number of persons employed part time for economic reasons is little different from its February 2020 level. These individuals, who would have preferred full-time employment, were working part time because their hours had been reduced or they were unable to find full-time jobs."The number of persons working part time for economic reasons increased in May to 4.328 million from 4.033 million in April. This is at pre-recession levels.

These workers are included in the alternate measure of labor underutilization (U-6) that increased to 7.1% from 7.0% in the previous month. This is down from the record high in April 22.9% for this measure since 1994. This measure is close to the 7.0% in February 2020 (pre-pandemic).

Unemployed over 26 Weeks

This graph shows the number of workers unemployed for 27 weeks or more.

This graph shows the number of workers unemployed for 27 weeks or more. According to the BLS, there are 1.356 million workers who have been unemployed for more than 26 weeks and still want a job, down from 1.483 million the previous month.

This does not include all the people that left the labor force.

Summary:

The headline monthly jobs number was above expectations; however, the previous two months were revised down by 22,000 combined.

The headline unemployment rate was unchanged at 3.6%.

There are still 0.8 million fewer jobs than prior to the recession.

Overall, this was another strong report.

May Employment Report: 390 thousand Jobs, 3.6% Unemployment Rate

by Calculated Risk on 6/03/2022 08:44:00 AM

From the BLS:

Total nonfarm payroll employment rose by 390,000 in May, and the unemployment rate remained at 3.6 percent, the U.S. Bureau of Labor Statistics reported today. Notable job gains occurred in leisure and hospitality, in professional and business services, and in transportation and warehousing. Employment in retail trade declined.

...

The change in total nonfarm payroll employment for March was revised down by 30,000, from +428,000 to +398,000, and the change for April was revised up by 8,000, from +428,000 to +436,000. With these revisions, employment in March and April combined is 22,000 lower than previously reported.

emphasis added

Click on graph for larger image.

Click on graph for larger image.The first graph shows the job losses from the start of the employment recession, in percentage terms.

The current employment recession was by far the worst recession since WWII in percentage terms.

However, 27 months after the onset of the current employment recession, almost all of the jobs have returned.

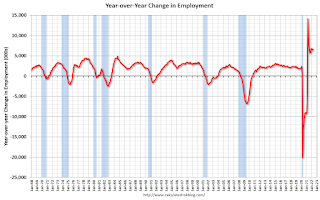

The second graph shows the year-over-year change in total non-farm employment since 1968.

The second graph shows the year-over-year change in total non-farm employment since 1968.

In May, the year-over-year change was 6.5 million jobs. This was up significantly year-over-year.

Total payrolls increased by 390 thousand in May. Private payrolls increased by 333 thousand, and public payrolls increased 57 thousand.

Payrolls for March and April were revised down 22 thousand, combined.

The third graph shows the employment population ratio and the participation rate.

The Labor Force Participation Rate increased to 62.3% in May, from 62.2% in April. This is the percentage of the working age population in the labor force.

The Labor Force Participation Rate increased to 62.3% in May, from 62.2% in April. This is the percentage of the working age population in the labor force.

The Employment-Population ratio increased to 60.1% from 60.0% (blue line).

I'll post the 25 to 54 age group employment-population ratio graph later.

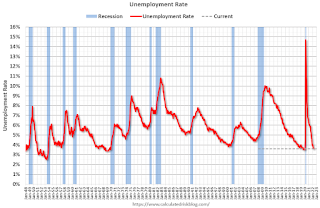

The fourth graph shows the unemployment rate.

The fourth graph shows the unemployment rate.

The unemployment rate was unchanged in May at 3.6% from 3.6% in April.

This was above consensus expectations; however, March and April payrolls were revised down by 22,000 combined.

The second graph shows the year-over-year change in total non-farm employment since 1968.

The second graph shows the year-over-year change in total non-farm employment since 1968.In May, the year-over-year change was 6.5 million jobs. This was up significantly year-over-year.

Total payrolls increased by 390 thousand in May. Private payrolls increased by 333 thousand, and public payrolls increased 57 thousand.

Payrolls for March and April were revised down 22 thousand, combined.

The third graph shows the employment population ratio and the participation rate.

The Labor Force Participation Rate increased to 62.3% in May, from 62.2% in April. This is the percentage of the working age population in the labor force.

The Labor Force Participation Rate increased to 62.3% in May, from 62.2% in April. This is the percentage of the working age population in the labor force. The Employment-Population ratio increased to 60.1% from 60.0% (blue line).

I'll post the 25 to 54 age group employment-population ratio graph later.

The fourth graph shows the unemployment rate.

The fourth graph shows the unemployment rate. The unemployment rate was unchanged in May at 3.6% from 3.6% in April.

This was above consensus expectations; however, March and April payrolls were revised down by 22,000 combined.

I'll have more later ...

Thursday, June 02, 2022

Friday: Employment Report

by Calculated Risk on 6/02/2022 09:01:00 PM

My May Employment Preview

Goldman May Payrolls Preview

Friday:

• At 8:30 AM ET, Employment Report for May. The consensus is for 320,000 jobs added, and for the unemployment rate to decline to 3.5%.

• At 10:00 AM, the ISM Services Index for May. The consensus is for a reading of 56.4, down from 57.1.

On COVID (focus on hospitalizations and deaths):

| COVID Metrics | ||||

|---|---|---|---|---|

| Now | Week Ago | Goal | ||

| Percent fully Vaccinated | 66.7% | --- | ≥70.0%1 | |

| Fully Vaccinated (millions) | 221.4 | --- | ≥2321 | |

| New Cases per Day3 | 100,683 | 110,080 | ≤5,0002 | |

| Hospitalized3🚩 | 21,306 | 20,290 | ≤3,0002 | |

| Deaths per Day3 | 244 | 318 | ≤502 | |

| 1 Minimum to achieve "herd immunity" (estimated between 70% and 85%). 2my goals to stop daily posts, 37-day average for Cases, Currently Hospitalized, and Deaths 🚩 Increasing 7-day average week-over-week for Cases, Hospitalized, and Deaths ✅ Goal met. | ||||

Click on graph for larger image.

Click on graph for larger image.This graph shows the daily (columns) and 7-day average (line) of deaths reported.

Average daily deaths bottomed in July 2021 at 214 per day.

Goldman May Payrolls Preview

by Calculated Risk on 6/02/2022 04:25:00 PM

A few brief excerpts from a note by Goldman Sachs economist Spencer Hill:

We estimate nonfarm payrolls rose by 225k in May (mom sa), a slowdown from the +428k pace in both of the previous two months and below consensus of +323k. ... We estimate a one-tenth drop in the unemployment rate to 3.5%—in line with consensusCR Note: The consensus is for 320 thousand jobs added, and for the unemployment rate to decline to 3.5%.

emphasis added

Hotels: Occupancy Rate Up 3.2% Compared to Same Week in 2019

by Calculated Risk on 6/02/2022 03:50:00 PM

This was the first increase in the occupancy rate compared to the same week in 2019. This was partly due to the timing of Memorial Day, and I expect the occupancy rate to be down compared to 2019 next week.

U.S. hotel performance dipped slightly from the previous week, according to STR‘s latest data through May 28.The following graph shows the seasonal pattern for the hotel occupancy rate using the four-week average.

May 22-28, 2022 (percentage change from comparable week in 2019*):

• Occupancy: 66.5% (+3.2%)

• Average daily rate (ADR): $151.73 (+22.2%)

• Revenue per available room (RevPAR): $100.97 (+26.2%)

*Due to the pandemic impact, STR is measuring recovery against comparable time periods from 2019.

emphasis added

Click on graph for larger image.

Click on graph for larger image.The red line is for 2022, black is 2020, blue is the median, and dashed light blue is for 2021. Dashed purple is 2019 (STR is comparing to a strong year for hotels).

The 4-week average of the occupancy rate is above the median rate for the previous 20 years (Blue).

Note: Y-axis doesn't start at zero to better show the seasonal change.

The 4-week average of the occupancy rate will now mostly move sideways seasonally until the summer.

May Employment Preview

by Calculated Risk on 6/02/2022 12:34:00 PM

On Friday at 8:30 AM ET, the BLS will release the employment report for May. The consensus is for 320,000 jobs added, and for the unemployment rate to decline to 3.5%.

Click on graph for larger image.

Click on graph for larger image.• First, currently there are still about 1.2 million fewer jobs than in February 2020 (the month before the pandemic).

This graph shows the job losses from the start of the employment recession, in percentage terms.

The current employment recession was by far the worst recession since WWII in percentage terms. However, the current employment recession, 26 months after the onset, has recovered quicker than the previous two recessions.

• ADP Report: The ADP employment report showed a gain of 128,000 private sector jobs, well below the consensus estimates of 280,000 jobs added. The ADP report hasn't been very useful in predicting the BLS report, but this suggests a weaker than expected BLS report.

• ISM Surveys: Note that the ISM services are diffusion indexes based on the number of firms hiring (not the number of hires). The ISM® manufacturing employment index decreased in May to 49.6%, down from 50.9% last month. This would suggest 20,000 jobs lost in manufacturing. ADP showed 22,000 manufacturing jobs added.

The ISM® Services employment index for May will be released tomorrow.

• Unemployment Claims: The weekly claims report showed an increase in the number of initial unemployment claims during the reference week (includes the 12th of the month) from 185,000 in April to 218,000 in May. This would usually suggest a few more layoffs in May than in April. In general, weekly claims were close to expectations in May.

• Permanent Job Losers: Something to watch in the employment report will be "Permanent job losers". This graph shows permanent job losers as a percent of the pre-recession peak in employment through the April report.

• Permanent Job Losers: Something to watch in the employment report will be "Permanent job losers". This graph shows permanent job losers as a percent of the pre-recession peak in employment through the April report.This data is only available back to 1994, so there is only data for three recessions. In April, the number of permanent job losers decreased to 1.386 million from 1.392 million in the previous month.

These jobs will likely be the hardest to recover, so it is a positive that the number of permanent job losers is declining fairly rapidly.

• COVID: As far as the pandemic, the number of daily cases during the reference week in May was around 90,000, up triple the 30,000 in April. This is a possible negative for the May report.

• Conclusion: The consensus is for job growth to slow to 320,000 jobs added in May. Overall, the ADP report was below expectations, the ISM manufacturing employment was negative, and unemployment claims increased during the reference week. This suggests a weaker than expected employment report for May.

Rent Increases Up Sharply Year-over-year, Pace is slowing

by Calculated Risk on 6/02/2022 09:11:00 AM

Today, in the Calculated Risk Real Estate Newsletter: Rent Increases Up Sharply Year-over-year, Pace is slowing

A brief excerpt:

Here is a graph of the year-over-year (YoY) change for these measures since January 2015. All of these measures are through April 2022 (Apartment List through May 2022).There is much more in the article. You can subscribe at https://calculatedrisk.substack.com/

Note that new lease measures (Zillow, Apartment List) dipped early in the pandemic, whereas the BLS measures were steady. Then new leases took off, and the BLS measures are picking up.

...

The Zillow measure is up 16.4% YoY in April, down from 17.0% YoY in March. This is down from a peak of 17.2% YoY in February.

The ApartmentList measure is up 15.3% YoY as of May, down from 16.4% in April. This is down from the peak of 17.9% YoY last November.

Clearly rents are still increasing, and we should expect this to continue to spill over into measures of inflation in 2022. The Owners’ Equivalent Rent (OER) was up 4.8% YoY in April, from 4.5% YoY in March - and will likely increase further in the coming months.

My suspicion is rent increases will slow over the coming months as the pace of household formation slows, and more supply comes on the market.

Weekly Initial Unemployment Claims Decrease to 200,000

by Calculated Risk on 6/02/2022 08:34:00 AM

The DOL reported:

In the week ending May 28, the advance figure for seasonally adjusted initial claims was 200,000, a decrease of 11,000 from the previous week's revised level. The previous week's level was revised up by 1,000 from 210,000 to 211,000. The 4-week moving average was 206,500, a decrease of 500 from the previous week's revised average. The previous week's average was revised up by 250 from 206,750 to 207,000.The following graph shows the 4-week moving average of weekly claims since 1971.

emphasis added

Click on graph for larger image.

Click on graph for larger image.The dashed line on the graph is the current 4-week average. The four-week average of weekly unemployment claims decreased to 206,500.

The previous week was revised up.

Weekly claims were lower than the consensus forecast.

ADP: Private Employment Increased 128,000 in May

by Calculated Risk on 6/02/2022 08:19:00 AM

Private sector employment increased by 128,000 jobs from April to May according to the May ADP® National Employment ReportTM. Broadly distributed to the public each month, free of charge, the ADP National Employment Report is produced by the ADP Research Institute® in collaboration with Moody’s Analytics. The report, which is derived from ADP’s actual data of those who are on a company’s payroll, measures the change in total nonfarm private employment each month on a seasonally-adjusted basisThis was below the consensus forecast of 280,000 for this report.

“Under a backdrop of a tight labor market and elevated inflation, monthly job gains are closer to pre-pandemic levels,” said Nela Richardson, chief economist, ADP. “The job growth rate of hiring has tempered across all industries, while small businesses remain a source of concern as they struggle to keep up with larger firms that have been booming as of late.”

emphasis added

The BLS report will be released Friday, and the consensus is for 320 thousand non-farm payroll jobs added in April. The ADP report has not been very useful in predicting the BLS report, but this suggests a weaker than expected BLS report.

Wednesday, June 01, 2022

Thursday: ADP Employment, Unemployment Claims

by Calculated Risk on 6/01/2022 09:14:00 PM

Thursday:

• At 8:15 AM ET, The ADP Employment Report for May. This report is for private payrolls only (no government). The consensus is for 280,000 payroll jobs added in May, up from 247,000 in April.

• At 8:30 AM, The initial weekly unemployment claims report will be released. The consensus is for 210 thousand unchanged from 210 thousand last week.

On COVID (focus on hospitalizations and deaths):

| COVID Metrics | ||||

|---|---|---|---|---|

| Now | Week Ago | Goal | ||

| Percent fully Vaccinated | 66.7% | --- | ≥70.0%1 | |

| Fully Vaccinated (millions) | 221.4 | --- | ≥2321 | |

| New Cases per Day3 | 103,686 | 108,692 | ≤5,0002 | |

| Hospitalized3🚩 | 20.984 | 20.011 | ≤3,0002 | |

| Deaths per Day3 | 264 | 303 | ≤502 | |

| 1 Minimum to achieve "herd immunity" (estimated between 70% and 85%). 2my goals to stop daily posts, 37-day average for Cases, Currently Hospitalized, and Deaths 🚩 Increasing 7-day average week-over-week for Cases, Hospitalized, and Deaths ✅ Goal met. | ||||

Click on graph for larger image.

Click on graph for larger image.This graph shows the daily (columns) and 7-day average (line) of deaths reported.

Average daily deaths bottomed in July 2021 at 214 per day.

Vehicles Sales Decreased to 12.68 million SAAR in May

by Calculated Risk on 6/01/2022 05:28:00 PM

Wards Auto released their estimate of light vehicle sales for May. Wards Auto estimates sales of 12.68 million SAAR in May 2022 (Seasonally Adjusted Annual Rate), down 11.2% from the April sales rate, and down 24.9% from May 2021.

Click on graph for larger image.

Click on graph for larger image.This graph shows light vehicle sales since 2006 from the BEA (blue) and Wards Auto's estimate for May (red).

The impact of COVID-19 was significant, and April 2020 was the worst month. After April 2020, sales increased, and were close to sales in 2019 (the year before the pandemic).

However, sales decreased late last year due to supply issues. It appears the "supply chain bottom" was in September 2021.

The second graph shows light vehicle sales since the BEA started keeping data in 1967.

The second graph shows light vehicle sales since the BEA started keeping data in 1967. Sales in May were below the consensus forecast of 14.5 million SAAR.

Fed's Beige Book: "Residential real estate contacts observed weakness"

by Calculated Risk on 6/01/2022 02:08:00 PM

Fed's Beige Book "This report was prepared at the Federal Reserve Bank of Philadelphia based on information collected on or before May 23, 2022."

All twelve Federal Reserve Districts have reported continued economic growth since the prior Beige Book period, with a majority indicating slight or modest growth; four Districts indicated moderate growth. Four Districts explicitly noted that the pace of growth had slowed since the prior period. Contacts in most Districts reported ongoing growth in manufacturing. Retail contacts noted some softening as consumers faced higher prices, and residential real estate contacts observed weakness as buyers faced high prices and rising interest rates. Contacts tended to cite labor market difficulties as their greatest challenge, followed by supply chain disruptions. Rising interest rates, general inflation, the Russian invasion of Ukraine, and disruptions from COVID-19 cases (especially in the Northeast) round out the key concerns impacting household and business plans. Eight Districts reported that expectations of future growth among their contacts had diminished; contacts in three Districts specifically expressed concerns about a recession.

...

Most Districts reported that employment rose modestly or moderately in a labor market that all Districts described as tight. One District explicitly reported that the pace of job growth had slowed, but some firms in most of the coastal Districts noted hiring freezes or other signs that market tightness had begun to ease. However, worker shortages continued to force many firms to operate below capacity. In response, firms continued to deploy automation, offer greater job flexibility, and raise wages. In a majority of Districts, firms reported strong wage growth, whereas most others reported moderate growth. However, in a few Districts, firms noted that wage rate increases were leveling off or edging down. Moreover, while firms throughout the country generally anticipate wages to rise further over the next year, one District indicated that its firms' expected rate of wage growth has fallen for two consecutive quarters.

emphasis added

Worst Housing Affordability" since 1991 excluding Bubble; Real House Prices and Price-to-Rent Ratio in March

by Calculated Risk on 6/01/2022 11:47:00 AM

Today, in the Calculated Risk Real Estate Newsletter: Worst Housing Affordability" since 1991 excluding Bubble

Excerpt:

I’ve put together my own affordability index - since 1976 - that is similar to the FirstAm approach (more of a house price index adjusted by mortgage rates and the median household income).

I used median income from the Census Bureau (estimated 2021 and 2022), assumed a 15% down payment, and used a 2% estimate for property taxes, insurance and maintenance. This is probably low for high property tax states like New Jersey and Texas, and too high for lower property tax states. If we were including condos, we’d also include HOA fees too (this is excluded).

For house prices, I used the Case-Shiller National Index, Seasonally Adjusted (SA). Also, for the down payment - there wasn’t a significant difference between 15% and 20%. For mortgage rates, I used the Freddie Mac PMMS (30-year fixed rates).

So here is what the index looks like (lower is more affordable like the FirstAm index):

Note that by this index, during the early ‘80s, homes were very unaffordable due to the very high mortgage rates. During the housing bubble, houses were also less affordable using 30-year mortgage rates, however, during the bubble, there were many “affordability products” that allowed borrowers to be qualified at the teaser rate (usually around 1%) that made houses seem more affordable.

In general, this would suggest houses are the least affordable since the housing bubble. And excluding the bubble - with all the “affordability products” - this is the worst affordability since 1991.

Look down to the second graph below (real house prices) and look what happened after 1991. House prices were mostly down or flat for the next 5 years in real terms.

Also, in March, the average 30-year mortgage rates were around 4.2%, and currently mortgage rates are close to 5.4% - so we already know the “Affordability Price Index” will increase further over the next couple of months (meaning houses are even less affordable).

There is much more in the article. You can subscribe at https://calculatedrisk.substack.com/

Construction Spending Increased 0.2% in April

by Calculated Risk on 6/01/2022 11:34:00 AM

From the Census Bureau reported that overall construction spending increased:

Construction spending during April 2022 was estimated at a seasonally adjusted annual rate of $1,744.8 billion, 0.2 percent above the revised March estimate of $1,740.6 billion. The April figure is 12.3 percent above the April 2021 estimate of $1,553.5 billion.Private spending increased and public spending decreased:

emphasis added

Spending on private construction was at a seasonally adjusted annual rate of $1,394.7 billion, 0.5 percent above the revised March estimate of $1,387.9 billion. ...

In April, the estimated seasonally adjusted annual rate of public construction spending was $350.1 billion, 0.7 percent below the revised March estimate of $352.7 billion.

Click on graph for larger image.

Click on graph for larger image.This graph shows private residential and nonresidential construction spending, and public spending, since 1993. Note: nominal dollars, not inflation adjusted.

Residential (red) spending is 31% above the bubble peak (in nominal terms - not adjusted for inflation).

Non-residential (blue) spending is 21% above the bubble era peak in January 2008 (nominal dollars).

Public construction spending is 8% above the peak in March 2009.

The second graph shows the year-over-year change in construction spending.

The second graph shows the year-over-year change in construction spending.On a year-over-year basis, private residential construction spending is up 18.4%. Non-residential spending is up 10.1% year-over-year. Public spending is up 1.8% year-over-year.

This was below consensus expectations of a 0.5% increase in spending; however, construction spending for the previous two months was revised up slightly.

BLS: Job Openings Decreased to 11.4 million in April

by Calculated Risk on 6/01/2022 10:13:00 AM

From the BLS: Job Openings and Labor Turnover Summary

The number of job openings decreased to 11.4 million on the last business day of April, the U.S. Bureau of Labor Statistics reported today. Hires and total separations were little changed at 6.6 million and 6.0 million, respectively. Within separations, quits were little changed at 4.4 million, while layoffs and discharges edged down to a series low of 1.2 million.The following graph shows job openings (yellow line), hires (dark blue), Layoff, Discharges and other (red column), and Quits (light blue column) from the JOLTS.

emphasis added

This series started in December 2000.

Note: The difference between JOLTS hires and separations is similar to the CES (payroll survey) net jobs headline numbers. This report is for April, the employment report this Friday will be for May.

Click on graph for larger image.

Click on graph for larger image.Note that hires (dark blue) and total separations (red and light blue columns stacked) are usually pretty close each month. This is a measure of labor market turnover. When the blue line is above the two stacked columns, the economy is adding net jobs - when it is below the columns, the economy is losing jobs.

The spike in layoffs and discharges in March 2020 is labeled, but off the chart to better show the usual data.

Jobs openings decreased in April to 11.400 million from 11.855 million in March.

The number of job openings (yellow) were up 23% year-over-year.

Quits were up 10% year-over-year. These are voluntary separations. (See light blue columns at bottom of graph for trend for "quits").

ISM® Manufacturing index Increased to 56.1% in May

by Calculated Risk on 6/01/2022 10:06:00 AM

(Posted with permission). The ISM manufacturing index indicated expansion. The PMI® was at 56.1% in May, up from 55.4% in April. The employment index was at 49.6%, down from 50.9% last month, and the new orders index was at 55.1%, up from 53.5%.

From ISM: Manufacturing PMI® at 56.1% May 2022 Manufacturing ISM® Report On Business®

Economic activity in the manufacturing sector grew in May, with the overall economy achieving a 24th consecutive month of growth, say the nation’s supply executives in the latest Manufacturing ISM® Report On Business®.This suggests manufacturing expanded at a faster pace in May than in April. This was above the consensus forecast, although the employment index was weak in May.

The report was issued today by Timothy R. Fiore, CPSM, C.P.M., Chair of the Institute for Supply Management® (ISM®) Manufacturing Business Survey Committee:

“The May Manufacturing PMI® registered 56.1 percent, an increase of 0.7 percentage point from the reading of 55.4 percent in April. This figure indicates expansion in the overall economy for the 24th month in a row after a contraction in April and May 2020. This is the second-lowest Manufacturing PMI® reading since September 2020, when it registered 55.4 percent. The New Orders Index reading of 55.1 percent is 1.6 percentage points higher than the 53.5 percent recorded in April. The Production Index reading of 54.2 percent is a 0.6-percentage point increase compared to April’s figure of 53.6 percent. The Prices Index registered 82.2 percent, down 2.4 percentage points compared to the April figure of 84.6 percent. The Backlog of Orders Index registered 58.7 percent, 2.7 percentage points higher than the April reading of 56 percent. The Employment Index went into contraction territory at 49.6 percent, 1.3 percentage points lower than the 50.9 percent recorded in April. The Supplier Deliveries Index reading of 65.7 percent is 1.5 percentage points lower than the April figure of 67.2 percent. The Inventories Index registered 55.9 percent, 4.3 percentage points higher than the April reading of 51.6 percent. The New Export Orders Index reading of 52.9 percent is up 0.2 percentage point compared to April’s figure of 52.7 percent. The Imports Index fell into contraction territory, decreasing 2.7 percentage points to 48.7 percent from 51.4 percent in April.”

emphasis added