RSS Feed

RSS Feed by Calculated Risk on 6/09/2022 08:34:00 AM

Thursday, June 09, 2022

Weekly Initial Unemployment Claims Increase to 229,000

The DOL reported:

In the week ending June 4, the advance figure for seasonally adjusted initial claims was 229,000, an increase of 27,000 from the previous week's revised level. The previous week's level was revised up by 2,000 from 200,000 to 202,000. The 4-week moving average was 215,000, an increase of 8,000 from the previous week's revised average. The previous week's average was revised up by 500 from 206,500 to 207,000.The following graph shows the 4-week moving average of weekly claims since 1971.

emphasis added

Click on graph for larger image.

Click on graph for larger image.The dashed line on the graph is the current 4-week average. The four-week average of weekly unemployment claims increased to 215,000.

The previous week was revised up.

Weekly claims were higher than the consensus forecast.

Wednesday, June 08, 2022

Thursday: Unemployment Claims, Q1 Flow of Funds

by Calculated Risk on 6/08/2022 09:01:00 PM

Thursday:

• At 8:30 AM ET, The initial weekly unemployment claims report will be released. The consensus is for 210 thousand up from 200 thousand last week.

• At 12:00 PM, Q1 Flow of Funds Accounts of the United States from the Federal Reserve.

On COVID (focus on hospitalizations and deaths):

| COVID Metrics | ||||

|---|---|---|---|---|

| Now | Week Ago | Goal | ||

| Percent fully Vaccinated | 66.7% | --- | ≥70.0%1 | |

| Fully Vaccinated (millions) | 221.6 | --- | ≥2321 | |

| New Cases per Day3🚩 | 104,511 | 103,774 | ≤5,0002 | |

| Hospitalized3🚩 | 23,230 | 21,425 | ≤3,0002 | |

| Deaths per Day3🚩 | 291 | 275 | ≤502 | |

| 1 Minimum to achieve "herd immunity" (estimated between 70% and 85%). 2my goals to stop daily posts, 37-day average for Cases, Currently Hospitalized, and Deaths 🚩 Increasing 7-day average week-over-week for Cases, Hospitalized, and Deaths ✅ Goal met. | ||||

Click on graph for larger image.

Click on graph for larger image.This graph shows the daily (columns) and 7-day average (line) of deaths reported.

Average daily deaths bottomed in July 2021 at 214 per day.

Homebuilder Comments in May: “Builder metrics quickly deteriorating"

by Calculated Risk on 6/08/2022 05:12:00 PM

Today, in the Calculated Risk Real Estate Newsletter: Homebuilder Comments in May: “Builder metrics quickly deteriorating"

A brief excerpt:

Read these comments. These are clear signs of a market shift.There is much more in the article. You can subscribe at https://calculatedrisk.substack.com/

Some homebuilder comments courtesy of Rick Palacios Jr., Director of Research at John Burns Real Estate Consulting (a must follow for housing on twitter!):

...

#Austin builder: “Some parts of town where finished homes are now taking a month to sell versus hours. Market is definitely correcting. Incentives are back and seeing some builders cutting prices on inventory.”

...

#Birmingham builder: “Steep decline in sales over past 2 weeks.”

...

#Greenville builder: “Lowest traffic in many months.”

#LosAngeles builder: “Seeing more cancellations due to payment shock for those in backlog that didn't lock rates.”

...

#Portland builder: “Incentives are back in the market.”

Current State of the Housing Market

by Calculated Risk on 6/08/2022 11:00:00 AM

Today, in the Calculated Risk Real Estate Newsletter: Current State of the Housing Market

A brief excerpt:

This is a market overview. There are clear signs of a market shift. A few quotes:There is much more in the article. You can subscribe at https://calculatedrisk.substack.com/

From Denver Metro Association of Realtors® “modest numbers this month became a sign that the market has returned to a semblance of ‘normal.’”

From Las Vegas: “The slowdown in sales and increase in our housing supply are signs that things may be starting to calm down a bit.” [LVR President Brandon] Roberts

From Seattle area: Mike Larson, a member of the board of directors at Northwest Multiple Listing Service described the market as "more balanced and not so crazy”.

...

We have to be patient waiting to see the impact on house prices of the slowdown in sales due to the significant data lags. Meanwhile, Altos Research CEO Mike Simonsen noted this week that “prices reductions” are the story right now.

Note the dark red line on the graph below. The percent of recent price reductions is still below normal for this time of year but increasing quicky - and it is well above last year at this time, and also above the level in 2020. This is an early indicator of the coming slowdown in house price growth.Mike Simonsen tweeted: Price reductions!

"That's the story of the US real estate market now.

While still fewer than normal, more sellers are cutting prices every day."

MBA: Mortgage Applications Decrease in Latest Weekly Survey

by Calculated Risk on 6/08/2022 07:00:00 AM

From the MBA: Mortgage Applications Decrease in Latest MBA Weekly Survey

Mortgage applications decreased 6.5 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending June 3, 2022. This week’s results include an adjustment for the Memorial Day holiday.

... The Refinance Index decreased 6 percent from the previous week and was 75 percent lower than the same week one year ago. The seasonally adjusted Purchase Index decreased 7 percent from one week earlier. The unadjusted Purchase Index decreased 18 percent compared with the previous week and was 21 percent lower than the same week one year ago.

“Weakness in both purchase and refinance applications pushed the market index down to its lowest level in 22 years. The 30-year fixed rate increased to 5.4 percent after three consecutive declines. While rates were still lower than they were four weeks ago, they remained high enough to still suppress refinance activity. Only government refinances saw a slight increase last week,” said Joel Kan, MBA’s Associate Vice President of Economic and Industry Forecasting. “The purchase market has suffered from persistently low housing inventory and the jump in mortgage rates over the past two months. These worsening affordability challenges have been particularly hard on prospective first-time buyers.”

...

The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($647,200 or less) increased to 5.40 percent from 5.33 percent, with points increasing to 0.60 from 0.51 (including the origination fee) for 80 percent loan-to-value ratio (LTV) loans.

emphasis added

Click on graph for larger image.

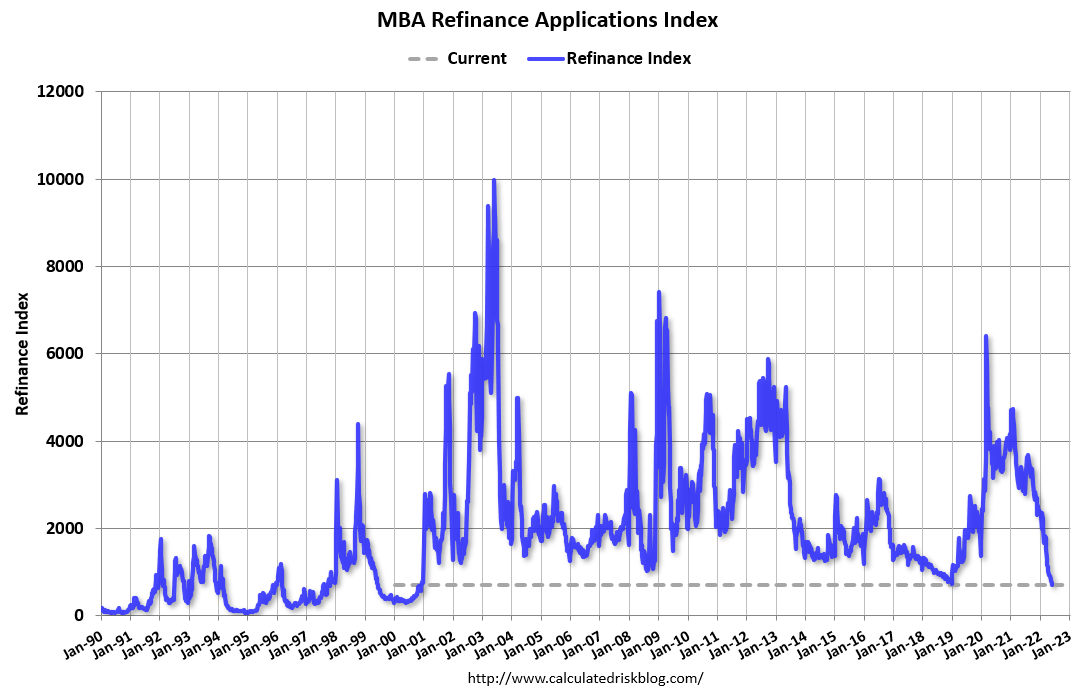

Click on graph for larger image.The first graph shows the refinance index since 1990.

With higher mortgage rates, the refinance index has declined sharply over the last several months.

The refinance index is at the lowest level since the year 2000.

The second graph shows the MBA mortgage purchase index

According to the MBA, purchase activity is down 21% year-over-year unadjusted.

According to the MBA, purchase activity is down 21% year-over-year unadjusted.Note: Red is a four-week average (blue is weekly).

Tuesday, June 07, 2022

Wednesday: Mortgage Purchase Index

by Calculated Risk on 6/07/2022 09:01:00 PM

Wednesday:

• At 7:00 AM ET, The Mortgage Bankers Association (MBA) will release the results for the mortgage purchase applications index.

On COVID (focus on hospitalizations and deaths):

| COVID Metrics | ||||

|---|---|---|---|---|

| Now | Week Ago | Goal | ||

| Percent fully Vaccinated | 66.7% | --- | ≥70.0%1 | |

| Fully Vaccinated (millions) | 221.6 | --- | ≥2321 | |

| New Cases per Day3🚩 | 108,891 | 97,584 | ≤5,0002 | |

| Hospitalized3🚩 | 22,764 | 21,287 | ≤3,0002 | |

| Deaths per Day3 | 287 | 295 | ≤502 | |

| 1 Minimum to achieve "herd immunity" (estimated between 70% and 85%). 2my goals to stop daily posts, 37-day average for Cases, Currently Hospitalized, and Deaths 🚩 Increasing 7-day average week-over-week for Cases, Hospitalized, and Deaths ✅ Goal met. | ||||

Click on graph for larger image.This graph shows the daily (columns) and 7-day average (line) of deaths reported.

Average daily deaths bottomed in July 2021 at 214 per day.

Leading Index for Commercial Real Estate "Shows Gains in May"

by Calculated Risk on 6/07/2022 04:18:00 PM

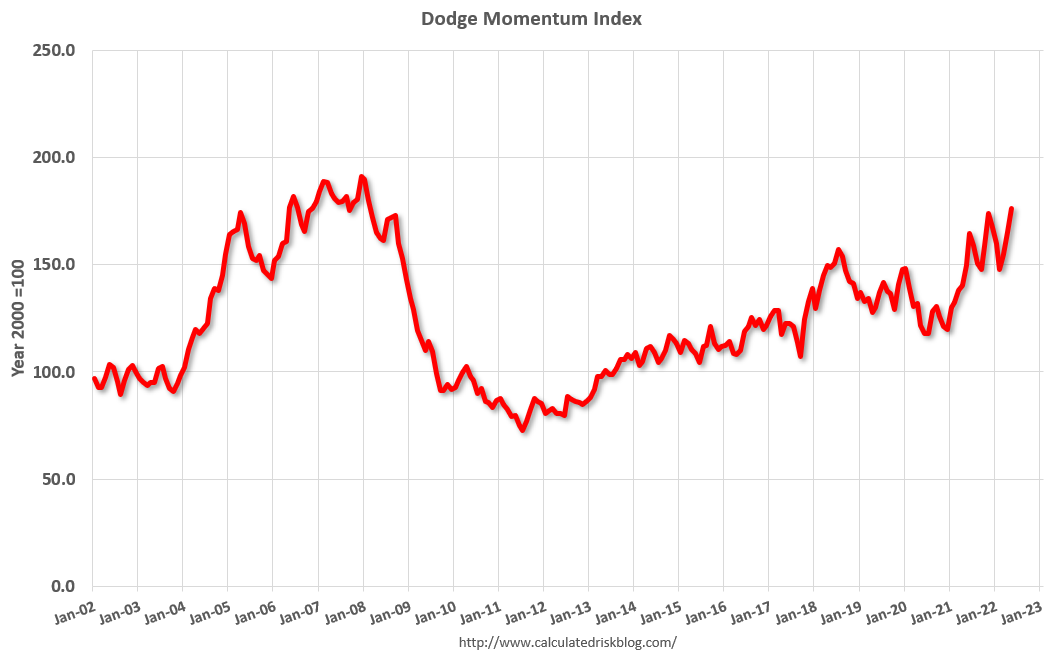

From Dodge Data Analytics: Dodge Momentum Index Shows Gains in May

The Dodge Momentum Index (DMI) jumped 7% in May to 176.2 (2000=100), up from the revised April reading of 165.2. The Momentum Index, issued by Dodge Construction Network, is a monthly measure of the initial report for nonresidential building projects in planning shown to lead construction spending for nonresidential buildings by a full year. In May, the institutional component of the Momentum Index rose 9%, and the commercial component increased 6%.

May’s increase in the Dodge Momentum Index pushed the level of planning above the most recent cyclical high in November 2021. During the month of May, commercial planning was led higher by an increase in office and hotel projects. Institutional planning was boosted by an increase in education and healthcare projects entering planning. On a year-over-year basis, the Momentum Index was 17% higher than in May 2021. The commercial component was 24% higher, and the institutional component was 8% higher than one year ago.

emphasis added

Click on graph for larger image.

Click on graph for larger image.This graph shows the Dodge Momentum Index since 2002. The index was at 176.2 in May, up from 165.2 in April.

According to Dodge, this index leads "construction spending for nonresidential buildings by a full year". This index suggested a decline in Commercial Real Estate construction through most of 2021, but a solid pickup this year and into 2023.

1st Look at Local Housing Markets in May, Inventory up Sharply

by Calculated Risk on 6/07/2022 12:22:00 PM

Today, in the Calculated Risk Real Estate Newsletter: 1st Look at Local Housing Markets in May, Inventory up Sharply

A brief excerpt:

From the Northwest MLS: Western Washington housing market "more balanced, and not so crazy - and that's a good thing"There is much more in the article. You can subscribe at https://calculatedrisk.substack.com/"Home sellers really need to re-think their expectations," suggested Mike Larson, a member of the board of directors at Northwest Multiple Listing Service (NWMLS) when commenting on statistics summarizing May activity. ...Here is a summary of active listings for these housing markets in May. Inventory usually increases seasonally in May, so some month-over-month (MoM) increase is not surprising.

Inventory in these markets were down 28% YoY in February, down 4% YoY in March, up 10% YoY in April, and up 42% YoY in May! So, this is a significant change from earlier this year. This is another step towards a more balanced market, but inventory levels are still historically low.

Notes for all tables:

1) New additions to table in BOLD.

2) Northwest (Seattle) and Santa Clara (San Jose)

Second Home Market: South Lake Tahoe in May

by Calculated Risk on 6/07/2022 10:29:00 AM

With the pandemic, there was a surge in 2nd home buying.

I'm looking at data for some second home markets - and I'm tracking those markets to see if there is an impact from lending changes like the FHFA Targeted Increases to Enterprise Pricing Framework, rising mortgage rates or the easing of the pandemic.

This graph is for South Lake Tahoe since 2004 through May 2022, and shows inventory (blue), and the year-over-year (YoY) change in the median price (12-month average).

Note: The median price is distorted by the mix, but this is the available data.

Click on graph for larger image.

Click on graph for larger image.

Following the housing bubble, prices declined for several years in South Lake Tahoe, with the median price falling about 50% from the bubble peak.

Currently inventory is still very low, but up from the record low set in February 2022, and up 50% year-over-year. Prices are up 16.1% YoY (but the YoY change has been trending down).

This will be interesting to watch, but so far there is little evidence of a 2nd home slowdown in these numbers.

Used Vehicle Wholesale Prices Increased Slightly in May

by Calculated Risk on 6/07/2022 09:15:00 AM

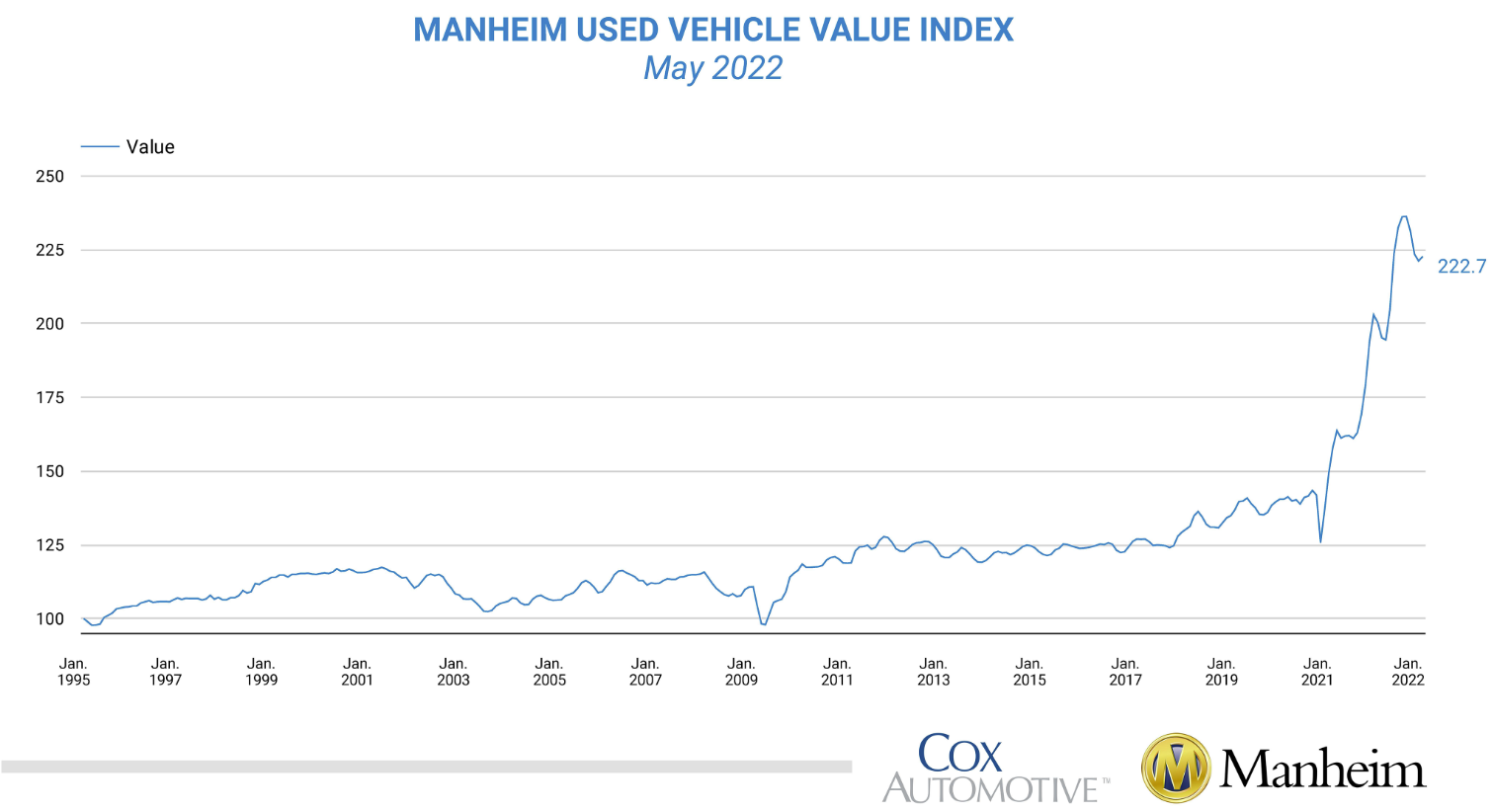

From Manheim Consulting today: Wholesale Used-Vehicle Prices Increase in May

Wholesale used-vehicle prices (on a mix-, mileage-, and seasonally adjusted basis) increased 0.7% in May from April. The Manheim Used Vehicle Value Index rose to 222.7, which was up 9.7% from a year ago. The non-adjusted price change in May was an increase of 1.1% compared to April, leaving the unadjusted average price up 12.1% year over year.

Manheim Market Report (MMR) values saw a shift in price trends in May with prices increasing in the first three weeks but declining over the last two.

emphasis added

Click on graph for larger image.

Click on graph for larger image.This index from Manheim Consulting is based on all completed sales transactions at Manheim’s U.S. auctions.

The Manheim index suggests used car prices increased in May and are up 9.7% year-over-year (YoY).

The YoY change is getting smaller. This index was up 45% YoY in January, up 14% in April, and now up less than 10% YoY.

Trade Deficit decreased to $87.1 Billion in April

by Calculated Risk on 6/07/2022 08:42:00 AM

From the Department of Commerce reported:

The U.S. Census Bureau and the U.S. Bureau of Economic Analysis announced today that the goods and services deficit was $87.1 billion in April, down $20.6 billion from $107.7 billion in March, revised.

April exports were $252.6 billion, $8.5 billion more than March exports. April imports were $339.7 billion, $12.1 billion less than March imports.

emphasis added

Click on graph for larger image.

Click on graph for larger image.Exports increased and imports decreased in April.

Exports are up 22% year-over-year; imports are up 24% year-over-year.

Both imports and exports decreased sharply due to COVID-19, and have now bounced back (imports more than exports),

The second graph shows the U.S. trade deficit, with and without petroleum.

The blue line is the total deficit, and the black line is the petroleum deficit, and the red line is the trade deficit ex-petroleum products.

The blue line is the total deficit, and the black line is the petroleum deficit, and the red line is the trade deficit ex-petroleum products.Note that net, imports and exports of petroleum products are close to zero.

The trade deficit with China increased to $30.6 billion in April, from $25.5 billion a year ago.

The trade deficit was smaller than the consensus forecast, and the deficit for March was revised down.

Monday, June 06, 2022

Tuesday: Trade Deficit

by Calculated Risk on 6/06/2022 09:00:00 PM

From Matthew Graham at Mortgage News Daily: Rates Jump Up To Highest Levels in Nearly a Month

... rates moved quite a bit higher today, as far as single days go. The average lender is at least an eighth of a percent (0.125%) higher than they were on Friday. The average conventional 30yr fixed rate is once again back up to at least 5.5% depending on number of mid-day price changes made by any given lender. [30 year fixed 5.50%]Tuesday:

emphasis added

• At 8:30 AM ET, 8:30 AM: Trade Balance report for April from the Census Bureau. The consensus is the trade deficit to be $89.3 billion. The U.S. trade deficit was at $109.8 Billion in March.

On COVID (focus on hospitalizations and deaths):

| COVID Metrics | ||||

|---|---|---|---|---|

| Now | Week Ago | Goal | ||

| Percent fully Vaccinated | 66.7% | --- | ≥70.0%1 | |

| Fully Vaccinated (millions) | 221.5 | --- | ≥2321 | |

| New Cases per Day3 | 98,513 | 106,339 | ≤5,0002 | |

| Hospitalized3 | 20,771 | 21,110 | ≤3,0002 | |

| Deaths per Day3 | 247 | 320 | ≤502 | |

| 1 Minimum to achieve "herd immunity" (estimated between 70% and 85%). 2my goals to stop daily posts, 37-day average for Cases, Currently Hospitalized, and Deaths 🚩 Increasing 7-day average week-over-week for Cases, Hospitalized, and Deaths ✅ Goal met. | ||||

Click on graph for larger image.

Click on graph for larger image.This graph shows the daily (columns) and 7-day average (line) of deaths reported.

Average daily deaths bottomed in July 2021 at 214 per day.

AAR: May Rail Carloads and Intermodal Down Year-over-year

by Calculated Risk on 6/06/2022 02:14:00 PM

From the Association of American Railroads (AAR) Rail Time Indicators. Graphs and excerpts reprinted with permission.

It was more of the same for U.S. freight rail traffic in May 2022: some commodities did pretty well, some did not so well, and some were in between.

Total carloads on U.S. railroads were down 3.7% in May, their second straight year-over-year decline and the third in the first five months of 2022. ... In May, U.S. intermodal volume averaged 275,640 units per week. That’s the highest weekly average for any month since June 2021 and the third-best weekly average for intermodal for May in history. May 2022 was down 4.3% from May 2021, which was the best May ever for intermodal.

emphasis added

Click on graph for larger image.

Click on graph for larger image.This graph from the Rail Time Indicators report shows the six-week average of U.S. Carloads in 2020, 2021 and 2022:

Originated U.S. rail carloads totaled 928,742 in May 2022, down 3.7% (35,821 carloads) from May 2021. It’s the third year-over-year monthly decline in the first five months of 2022. Total carloads averaged 232,186 per week in May 2022. In our records that go back to 1988, only 2020 had a lower weekly average for May.

The second graph shows the six-week average (not monthly) of U.S. intermodal in 2020, 2021 and 2022: (using intermodal or shipping containers):

The second graph shows the six-week average (not monthly) of U.S. intermodal in 2020, 2021 and 2022: (using intermodal or shipping containers):Intermodal is not included in carloads. In May 2022, U.S. intermodal volume was 1.10 million containers and trailers, an average of 275,640 units per week. That’s the highest weekly average for any month since June 2021 and the third-best weekly average for intermodal for May in history. Still, it was down 4.3% from May 2021, which was the best May ever for intermodal. (May 2018 was also higher than May 2022.)

Black Knight Mortgage Monitor: "Housing costs to current income levels within a whisper of all time high in 2006"

by Calculated Risk on 6/06/2022 11:03:00 AM

Today, in the Calculated Risk Real Estate Newsletter: Black Knight Mortgage Monitor: "Housing costs to current income levels within a whisper of all time high in 2006"

A brief excerpt:

Note: Black Knights data on affordability goes back to 1996. This doesn’t include housing in the 1980 period when 30-year mortgage rates peaked at over 18%.There is much more in the article. You can subscribe at https://calculatedrisk.substack.com/

And on the payment to income ratio:

• May marked the least affordable housing since July 2006, and ranked among the three least affordable months on recordDuring the housing bubble, there were “affordability products” with low teaser rates available. Excluding the bubble years, this is the worst affordability since at least the early ‘90s, maybe ‘80s.

• The monthly payment required to purchase the average price home with 20% down jumped another $100 through mid-May, and is now up nearly $600 (+44%) from the start of the year and $865 (+79%) from the start of the pandemic

• When comparing the rise in housing costs to current income levels, it now takes 33.7% of the median household income to purchase the average priced home, within a whisper of the 34.1% all time high at its peak in June 2006

Housing Inventory June 6th Update: Inventory UP 13.9% Year-over-year

by Calculated Risk on 6/06/2022 09:33:00 AM

Altos reports inventory is up 13.9% year-over-year.

Inventory usually declines in the winter, and then increases in the spring. Inventory bottomed seasonally at the beginning of March 2022 and is now up 56% since then.

Click on graph for larger image in graph gallery.

Click on graph for larger image in graph gallery.

This inventory graph is courtesy of Altos Research.

As of June 3rd, inventory was at 375 thousand (7-day average), compared to 364 thousand the prior week. Inventory was up 3.1% from the previous week.

Inventory is still very low. Compared to the same week in 2021, inventory is up 13.9% from 329 thousand, however compared to the same week in 2020 inventory is down 46.8% from 706 thousand. Compared to 3 years ago, inventory is down 60.0% from 938 thousand.

Inventory is still very low. Compared to the same week in 2021, inventory is up 13.9% from 329 thousand, however compared to the same week in 2020 inventory is down 46.8% from 706 thousand. Compared to 3 years ago, inventory is down 60.0% from 938 thousand.

Here are the inventory milestones I’m watching for with the Altos data:

1. The seasonal bottom (happened on March 4th for Altos) ✅

2. Inventory up year-over-year (happened on May 13th for Altos) ✅

3. Inventory up compared to two years ago (currently down 46.8% according to Altos)

4. Inventory up compared to 2019 (currently down 60.0%).

1. The seasonal bottom (happened on March 4th for Altos) ✅

2. Inventory up year-over-year (happened on May 13th for Altos) ✅

3. Inventory up compared to two years ago (currently down 46.8% according to Altos)

4. Inventory up compared to 2019 (currently down 60.0%).

Here is a graph of the inventory change vs 2021, 2020 (milestone 3 above) and 2019 (milestone 4).

The blue line is the year-over-year data, the red line is compared to two years ago, and dashed purple is compared to 2019.

Two years ago (in 2020) inventory was declining all year, so the two-year comparison will get easier all year. My current guess is inventory will be up in Q4 compared to the same week in 2020.

Mike Simonsen discusses this data regularly on Youtube.

Four High Frequency Indicators for the Economy

by Calculated Risk on 6/06/2022 08:35:00 AM

These indicators are mostly for travel and entertainment. It is interesting to watch these sectors recover as the pandemic subsides. Note: Apple has discontinued "Apple mobility", and restaurant traffic is mostly back to normal.

The TSA is providing daily travel numbers.

This data is as of June 5th.

Click on graph for larger image.

Click on graph for larger image.This data shows the 7-day average of daily total traveler throughput from the TSA for 2019 (Light Blue), 2020 (Black), 2021 (Blue) and 2022 (Red).

The dashed line is the percent of 2019 for the seven-day average.

The 7-day average is down 12.4% from the same day in 2019 87.6% of 2019). (Dashed line)

Air travel has been moving sideways over the last three months, off about 10% from 2019.

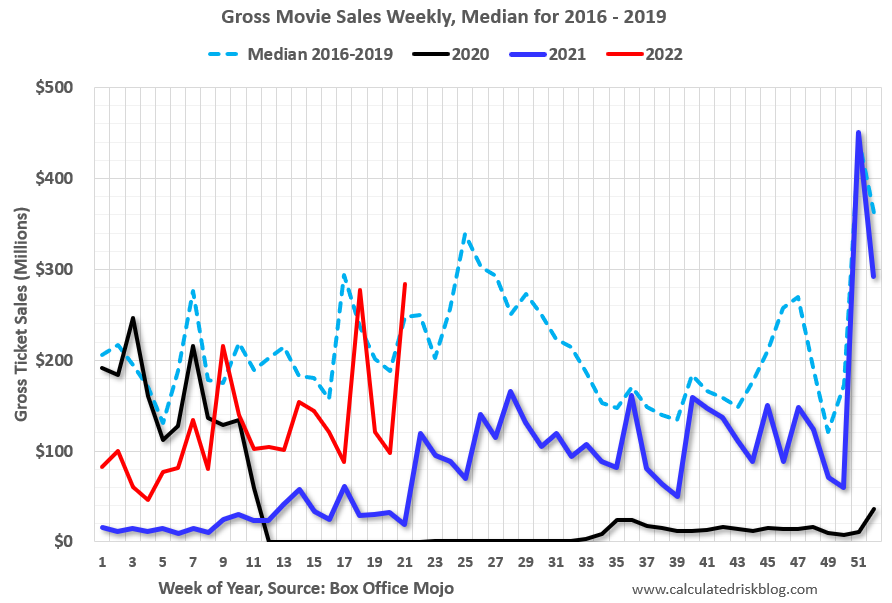

This data shows domestic box office for each week and the median for the years 2016 through 2019 (dashed light blue).

This data shows domestic box office for each week and the median for the years 2016 through 2019 (dashed light blue). Black is 2020, Blue is 2021 and Red is 2022.

The data is from BoxOfficeMojo through June 2nd.

Note that the data is usually noisy week-to-week and depends on when blockbusters are released.

Movie ticket sales were at $284 million last week, up about 15% from the median for the week - due primarily to the release of Top Gun.

Note that the data is usually noisy week-to-week and depends on when blockbusters are released.

Movie ticket sales were at $284 million last week, up about 15% from the median for the week - due primarily to the release of Top Gun.

This graph shows the seasonal pattern for the hotel occupancy rate using the four-week average.

This graph shows the seasonal pattern for the hotel occupancy rate using the four-week average. The red line is for 2022, black is 2020, blue is the median, and dashed light blue is for 2021. Dashed purple is 2019 (STR is comparing to a strong year for hotels).

This data is through May 28th. The occupancy rate was up 3.2% compared to the same week in 2019.

The 4-week average of the occupancy rate is at the median rate for the previous 20 years (Blue).

Notes: Y-axis doesn't start at zero to better show the seasonal change.

Notes: Y-axis doesn't start at zero to better show the seasonal change.

This was the first increase in the occupancy rate compared to the same week in 2019. This was partly due to the timing of Memorial Day, and I expect the occupancy rate to be down compared to 2019 next week.

Here is some interesting data on New York subway usage (HT BR).

This graph is from Todd W Schneider.

This graph is from Todd W Schneider. This graph shows how much MTA traffic has recovered in each borough (Graph starts at first week in January 2020 and 100 = 2019 average).

Manhattan is at about 39% of normal.

This data is through Friday, June 3rd.

He notes: "Data updates weekly from the MTA’s public turnstile data, usually on Saturday mornings".

Sunday, June 05, 2022

Sunday Night Futures

by Calculated Risk on 6/05/2022 06:07:00 PM

Weekend:

• Schedule for Week of June 5, 2022

Monday:

• No major economic releases scheduled.

From CNBC: Pre-Market Data and Bloomberg futures S&P 500 DOW futures are up slightly (fair value).

Oil prices were up over the last week with WTI futures at $118.87 per barrel and Brent at $119.72 per barrel. A year ago, WTI was at $69 and Brent was at $71 - so WTI oil prices are up 70% year-over-year.

Here is a graph from Gasbuddy.com for nationwide gasoline prices. Nationally prices are at $4.86 per gallon. A year ago prices were at $3.04 per gallon, so gasoline prices are up $1.82 per gallon year-over-year.

Vehicle Sales Mix and Heavy Trucks

by Calculated Risk on 6/05/2022 12:13:00 PM

It will be interesting to see if high gasoline prices will lead to a higher percentage of passenger car sales.

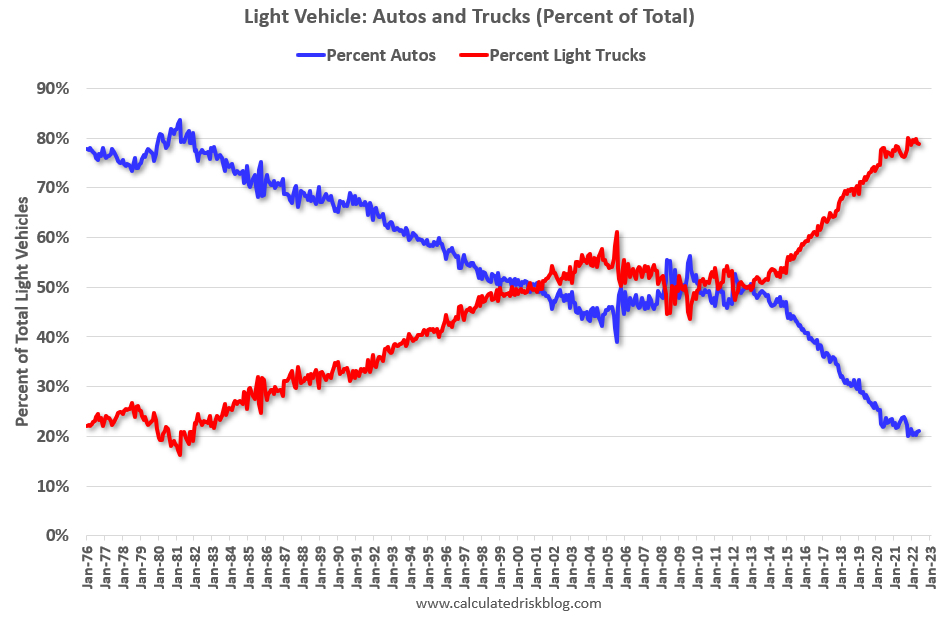

This graph shows the percent of light vehicle sales between passenger cars and trucks / SUVs through May 2022.

Over time the mix has changed more and more towards light trucks and SUVs.

Over time the mix has changed more and more towards light trucks and SUVs.Only when oil prices are high, does the trend slow or reverse.

The percent of light trucks and SUVs was at 78.9% in May 2022 - just below the record high percentage of 80.0% last October.

The second graph shows heavy truck sales since 1967 using data from the BEA. The dashed line is the May 2022 seasonally adjusted annual sales rate (SAAR).

Heavy truck sales really collapsed during the great recession, falling to a low of 180 thousand SAAR in May 2009. Then heavy truck sales increased to a new all-time high of 563 thousand SAAR in September 2019.

Heavy truck sales really collapsed during the great recession, falling to a low of 180 thousand SAAR in May 2009. Then heavy truck sales increased to a new all-time high of 563 thousand SAAR in September 2019.Note: "Heavy trucks - trucks more than 14,000 pounds gross vehicle weight."

Heavy truck sales really declined at the beginning of the pandemic, falling to a low of 299 thousand SAAR in May 2020.

Heavy truck sales were at 450 thousand SAAR in May, up from 442 thousand in April, and down 10% from 501 thousand SAAR in May 2021. If there is a slump in construction, then heavy truck sales will decline.

Saturday, June 04, 2022

Real Estate Newsletter Articles this Week

by Calculated Risk on 6/04/2022 02:11:00 PM

At the Calculated Risk Real Estate Newsletter this week:

• When will House Price Growth Slow?

• Rent Increases Up Sharply Year-over-year, Pace is slowing

• Worst Housing Affordability" since 1991 excluding Bubble

• Case-Shiller National Index up 20.6% Year-over-year in March; New Record Monthly Increase

• Lawler: Large Builders Acquired Lots of Lots over the Last Year

This is usually published 4 to 6 times a week and provides more in-depth analysis of the housing market.

You can subscribe at https://calculatedrisk.substack.com/

Most content is available for free (and no Ads), but please subscribe!

Schedule for Week of June 5, 2022

by Calculated Risk on 6/04/2022 08:11:00 AM

The key report this week is CPI.

Other key reports include the April trade balance and Q1 Flow of Funds.

No major economic releases scheduled.

8:30 AM: Trade Balance report for April from the Census Bureau.

8:30 AM: Trade Balance report for April from the Census Bureau. The consensus is the trade deficit to be $89.3 billion. The U.S. trade deficit was at $109.8 Billion in March.

7:00 AM ET: The Mortgage Bankers Association (MBA) will release the results for the mortgage purchase applications index.

8:30 AM: The initial weekly unemployment claims report will be released. The consensus is for 210 thousand up from 200 thousand last week.

12:00 PM: Q1 Flow of Funds Accounts of the United States from the Federal Reserve.

8:30 AM: The Consumer Price Index for May from the BLS. The consensus is for 0.7% increase in CPI, and a 0.5% increase in core CPI.

10:00 AM: University of Michigan's Consumer sentiment index (Preliminary for June).