RSS Feed

RSS Feed by Calculated Risk on 6/13/2022 08:48:00 PM

Monday, June 13, 2022

Goldman Expects 75bp Rate Hike

From Goldman Sachs chief economist Jan Hatzius

"We have revised our forecast to include 75bp hikes in June and July. This would quickly reset the level of the funds rate at 2.25-2.5%, the FOMC’s median estimate of the neutral rate."Tuesday:

emphasis added

• At 6:00 AM ET, NFIB Small Business Optimism Index for May.

• At 8:30 AM, The Producer Price Index for May from the BLS. The consensus is for a 0.8% increase in PPI, and a 0.6% increase in core PPI.

On COVID (focus on hospitalizations and deaths):

| COVID Metrics | ||||

|---|---|---|---|---|

| Now | Week Ago | Goal | ||

| Percent fully Vaccinated | 66.8% | --- | ≥70.0%1 | |

| Fully Vaccinated (millions) | 221.7 | --- | ≥2321 | |

| New Cases per Day3🚩 | 103,821 | 99,621 | ≤5,0002 | |

| Hospitalized3 | 21,746 | 22,956 | ≤3,0002 | |

| Deaths per Day3🚩 | 276 | 266 | ≤502 | |

| 1 Minimum to achieve "herd immunity" (estimated between 70% and 85%). 2my goals to stop daily posts, 37-day average for Cases, Currently Hospitalized, and Deaths 🚩 Increasing 7-day average week-over-week for Cases, Hospitalized, and Deaths ✅ Goal met. | ||||

Click on graph for larger image.

Click on graph for larger image.This graph shows the daily (columns) and 7-day average (line) of deaths reported.

Average daily deaths bottomed in July 2021 at 214 per day.

30-Year Mortgage Rates Increase to 6.13%

by Calculated Risk on 6/13/2022 03:21:00 PM

From Matthew Graham at MortgageNewsDaily: MBS Live Morning: From Bad to Worse as CPI Reaction Continues

From Matthew Graham at MortgageNewsDaily: MBS Live Morning: From Bad to Worse as CPI Reaction Continues

Bonds are in the midst of a full-blown capitulation move with 10yr yields currently up over 16bps at 3.32%. MBS are down roughly a full point. These aren't the biggest losses we've ever seen in a day, but they're extraordinarily big losses to be experiencing at the top of trend that has already covered as much ground as the one seen so far in 2022.

...

Long story short, the market is freaked out about what Friday means for the policy outlook. Wednesday continues to be one of the biggest flashpoints for bond volatility we've seen in a long time.

Click on graph for larger image.

Click on graph for larger image.This is a graph from Mortgage News Daily (MND) showing 30-year fixed rates from three sources (MND, MBA, Freddie Mac) over the last year.

The 30-year fixed rate for top tier scenarios was 6.13% today, up from 5.55% last Thursday.

Go to MND and you can adjust the graph for different time periods.

2nd Look at Local Housing Markets in May, New Listings picking up

by Calculated Risk on 6/13/2022 12:10:00 PM

Today, in the Calculated Risk Real Estate Newsletter: 2nd Look at Local Housing Markets in May, New Listings picking up

A brief excerpt:

This is the second look at local markets in May. I’m tracking about 35 local housing markets in the US. Some of the 35 markets are states, and some are metropolitan areas. I’ll update these tables throughout the month as additional data is released.There is much more in the article. You can subscribe at https://calculatedrisk.substack.com/

We are seeing a significant change in inventory, and maybe a pickup in new listings. So far, most of the increase in inventory has been due to softer demand - likely because of higher mortgage rates - but we need to keep an eye on new listings too.

On a national basis, we saw record low inventory levels over the Winter. Last year, inventory didn’t bottom seasonally until early April. This year inventory bottomed in February (normal seasonal timing), and recent data from Altos Research and Realtor.com, indicate active inventory was up year-over-year in May. I expect the local market reports will show inventory up year-over-year in May too.

...

And here is a table for new listings in May. For these areas, new listings were up 5.0% YoY. Last month, new listings in these markets were down 6.2% YoY. This could be a significant change, and the first sign of a pickup in new listings. If new listings increase, combined with less demand, we will see active inventory increase quickly.Notes for all tables:

1) New additions to table in BOLD.

2) Northwest (Seattle), North Texas (Dallas) and Santa Clara (San Jose), Mid-Florida (Tampa, Orlando), Jacksonville, Source: Northeast Florida Association of REALTORS®

3) Totals do not include Denver or Atlanta (included in state totals).

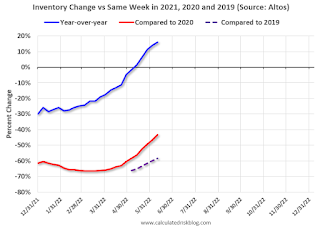

Housing Inventory June 13th Update: Inventory up 15.9% Year-over-year

by Calculated Risk on 6/13/2022 09:53:00 AM

Altos reports inventory is up 15.9% year-over-year.

Inventory usually declines in the winter, and then increases in the spring. Inventory bottomed seasonally at the beginning of March 2022 and is now up 64% since then.

Click on graph for larger image in graph gallery.

Click on graph for larger image in graph gallery.

This inventory graph is courtesy of Altos Research.

As of June 10th, inventory was at 396 thousand (7-day average), compared to 375 thousand the prior week. Inventory was up 5.6% from the previous week.

Inventory is still very low. Compared to the same week in 2021, inventory is up 15.9% from 342 thousand, however compared to the same week in 2020 inventory is down 43.2% from 698 thousand. Compared to 3 years ago, inventory is down 58.3% from 950 thousand.

Inventory is still very low. Compared to the same week in 2021, inventory is up 15.9% from 342 thousand, however compared to the same week in 2020 inventory is down 43.2% from 698 thousand. Compared to 3 years ago, inventory is down 58.3% from 950 thousand.

Here are the inventory milestones I’m watching for with the Altos data:

1. The seasonal bottom (happened on March 4th for Altos) ✅

2. Inventory up year-over-year (happened on May 13th for Altos) ✅

3. Inventory up compared to two years ago (currently down 43.2% according to Altos)

4. Inventory up compared to 2019 (currently down 58.2%).

1. The seasonal bottom (happened on March 4th for Altos) ✅

2. Inventory up year-over-year (happened on May 13th for Altos) ✅

3. Inventory up compared to two years ago (currently down 43.2% according to Altos)

4. Inventory up compared to 2019 (currently down 58.2%).

Here is a graph of the inventory change vs 2021, 2020 (milestone 3 above) and 2019 (milestone 4).

The blue line is the year-over-year data, the red line is compared to two years ago, and dashed purple is compared to 2019.

Two years ago (in 2020) inventory was declining all year, so the two-year comparison will get easier all year. My current guess is inventory will be up in Q4 compared to the same week in 2020.

Mike Simonsen discusses this data regularly on Youtube.

Five High Frequency Indicators for the Economy

by Calculated Risk on 6/13/2022 08:26:00 AM

These indicators are mostly for travel and entertainment. It is interesting to watch these sectors recover as the pandemic subsides. Notes: I've added back gasoline supplied to see if there is an impact from higher gasoline prices. Apple has discontinued "Apple mobility", and restaurant traffic is mostly back to normal.

The TSA is providing daily travel numbers.

This data is as of June 12th.

Click on graph for larger image.

Click on graph for larger image.This data shows the 7-day average of daily total traveler throughput from the TSA for 2019 (Light Blue), 2020 (Black), 2021 (Blue) and 2022 (Red).

The dashed line is the percent of 2019 for the seven-day average.

The 7-day average is down 12.6% from the same day in 2019 87.4% of 2019). (Dashed line)

Air travel has been moving sideways over the last several months, off about 10% from 2019.

This data shows domestic box office for each week and the median for the years 2016 through 2019 (dashed light blue).

This data shows domestic box office for each week and the median for the years 2016 through 2019 (dashed light blue). Black is 2020, Blue is 2021 and Red is 2022.

The data is from BoxOfficeMojo through June 9th.

Note that the data is usually noisy week-to-week and depends on when blockbusters are released.

Movie ticket sales were at $185 million last week, down about 26% from the median for the week.

Note that the data is usually noisy week-to-week and depends on when blockbusters are released.

Movie ticket sales were at $185 million last week, down about 26% from the median for the week.

This graph shows the seasonal pattern for the hotel occupancy rate using the four-week average.

This graph shows the seasonal pattern for the hotel occupancy rate using the four-week average. The red line is for 2022, black is 2020, blue is the median, and dashed light blue is for 2021. Dashed purple is 2019 (STR is comparing to a strong year for hotels).

This data is through June 4th. The occupancy rate was down 12.1% compared to the same week in 2019.

The 4-week average of the occupancy rate is slightly above the median rate for the previous 20 years (Blue).

Notes: Y-axis doesn't start at zero to better show the seasonal change.

Notes: Y-axis doesn't start at zero to better show the seasonal change.

This graph, based on weekly data from the U.S. Energy Information Administration (EIA), shows gasoline supplied compared to the same week of 2019.

This graph, based on weekly data from the U.S. Energy Information Administration (EIA), shows gasoline supplied compared to the same week of 2019.Blue is for 2020. Purple is for 2021, and Red is for 2022.

As of June 3rd, gasoline supplied was down 2.6% compared to the same week in 2019.

Recently gasoline supplied has been running somewhat below 2019 levels.

Here is some interesting data on New York subway usage (HT BR).

This graph is from Todd W Schneider.

This graph is from Todd W Schneider. This graph shows how much MTA traffic has recovered in each borough (Graph starts at first week in January 2020 and 100 = 2019 average).

Manhattan is at about 39% of normal.

This data is through Friday, June 10th.

He notes: "Data updates weekly from the MTA’s public turnstile data, usually on Saturday mornings".

Sunday, June 12, 2022

Sunday Night Futures

by Calculated Risk on 6/12/2022 07:09:00 PM

Weekend:

• Schedule for Week of June 12, 2022

Monday:

• No major economic releases scheduled.

From CNBC: Pre-Market Data and Bloomberg futures S&P 500 futures are down 37, and DOW futures are down 156 (fair value).

Oil prices were mixed over the last week with WTI futures at $118.73 per barrel and Brent at $120.00 per barrel. A year ago, WTI was at $69 and Brent was at $71 - so WTI oil prices are up 70% year-over-year.

Here is a graph from Gasbuddy.com for nationwide gasoline prices. Nationally prices are at $5.01 per gallon. A year ago prices were at $3.07 per gallon, so gasoline prices are up $1.94 per gallon year-over-year.

FOMC Preview: 50bp Hike

by Calculated Risk on 6/12/2022 09:41:00 AM

Update: From Goldman Sachs chief economist Jan Hatzius

"We have revised our forecast to include 75bp hikes in June and July. This would quickly reset the level of the funds rate at 2.25-2.5%, the FOMC’s median estimate of the neutral rate."Expectations are the FOMC will announce a 50bp rate increase in the federal funds rate at the meeting this week.

emphasis added

From Merrill Lynch:

1 Projections of change in real GDP and inflation are from the fourth quarter of the previous year to the fourth quarter of the year indicated.

The unemployment rate was at 3.6% in May. The question is: Will the slowdown in economic growth push up the unemployment rate? Or will the rate continue to decline? The projections for the unemployment rate will likely be mostly unchanged.

2 Projections for the unemployment rate are for the average civilian unemployment rate in the fourth quarter of the year indicated.

As of April 2022, PCE inflation was up 6.3% from April 2021. This was below the cycle high of 6.6%. Based on recent readings, inflation might stay elevated longer than expected. PCE inflation will likely be revised up for 2022.

PCE core inflation was up 4.9% in April year-over-year. This was below the cycle high of 5.3%. Core PCE inflation will also likely be revised up.

"We don’t expect major fireworks at the June FOMC meeting. Chair Powell and the Fed has communicated that they are likely to hike by 50bp at this meeting (as well as at the next meeting in July) and we expect them to deliver. What will be of interest will be the updated Summary of Economic Projections (SEP) and dot plot.Update: From Goldman Sachs:

...

In the press conference, we expect Chair Powell to reiterate that labor market momentum is still too strong, inflation remains a big problem, and that the Fed is committed to restoring price stability. We don’t expect any concrete forward guidance beyond the next meeting, with Powell noting a reassessment in the path of hikes in September dependent on convincing signs that inflation is slowing. If asked about a pause in September, he is likely to outright dismiss the idea."

The FOMC is likely to respond to the firmer inflation print and the rise in long-term inflation expectations with a resolutely hawkish message at the June meeting, in addition to the 50bp rate hike it is set to deliver. This should come across clearly in the statement, the economic projections, and the dots.

We expect the FOMC to revise the policy guidance in its statement to say that the Committee “anticipates that raising the target range expeditiously will be appropriate until it sees clear and convincing evidence that inflation is moderating,” implying a high bar for reverting to 25bp hikes.

Analysts will be looking for comments on the size of future rate hikes.

Projections will be released at this meeting. For review, here are the March projections. In March, most participants expected seven rate hikes in 2022. It appears the FOMC will reach seven 25bp hikes by July, and still have three more meetings to go.

Wall Street forecasts are being revised down for 2022 due to the ongoing negative impacts from the pandemic and the war in Ukraine. So, GDP for 2022 will likely be revised down.

Wall Street forecasts are being revised down for 2022 due to the ongoing negative impacts from the pandemic and the war in Ukraine. So, GDP for 2022 will likely be revised down.

| GDP projections of Federal Reserve Governors and Reserve Bank presidents, Change in Real GDP1 | ||||

|---|---|---|---|---|

| Projection Date | 2022 | 2023 | 2024 | |

| Mar 2022 | 2.5 to 3.0 | 2.1 to 2.5 | 1.8 to 2.0 | |

The unemployment rate was at 3.6% in May. The question is: Will the slowdown in economic growth push up the unemployment rate? Or will the rate continue to decline? The projections for the unemployment rate will likely be mostly unchanged.

| Unemployment projections of Federal Reserve Governors and Reserve Bank presidents, Unemployment Rate2 | ||||

|---|---|---|---|---|

| Projection Date | 2022 | 2023 | 2024 | |

| Mar 2022 | 3.4 to 3.6 | 3.3 to 3.6 | 3.2 to 3.7 | |

As of April 2022, PCE inflation was up 6.3% from April 2021. This was below the cycle high of 6.6%. Based on recent readings, inflation might stay elevated longer than expected. PCE inflation will likely be revised up for 2022.

| Inflation projections of Federal Reserve Governors and Reserve Bank presidents, PCE Inflation1 | ||||

|---|---|---|---|---|

| Projection Date | 2022 | 2023 | 2024 | |

| Mar 2022 | 4.1 to 4.7 | 2.3 to 3.0 | 2.1 to 2.4 | |

PCE core inflation was up 4.9% in April year-over-year. This was below the cycle high of 5.3%. Core PCE inflation will also likely be revised up.

| Core Inflation projections of Federal Reserve Governors and Reserve Bank presidents, Core Inflation1 | ||||

|---|---|---|---|---|

| Projection Date | 2022 | 2023 | 2024 | |

| Mar 2022 | 3.9 to 4.4 | 2.4 to 3.0 | 2.1 to 2.4 | |

Saturday, June 11, 2022

Real Estate Newsletter Articles this Week

by Calculated Risk on 6/11/2022 02:11:00 PM

At the Calculated Risk Real Estate Newsletter this week:

• 1st Look at Local Housing Markets in May, Inventory up Sharply

• Current State of the Housing Market

• Homebuilder Comments in May: “Builder metrics quickly deteriorating"

• The Home ATM Still Open in Q1 2022; Closing Soon

• 30-Year Mortgage Rates increase to 5.85%

• Black Knight Mortgage Monitor: "Housing costs to current income levels within a whisper of all time high in 2006"

This is usually published 4 to 6 times a week and provides more in-depth analysis of the housing market.

You can subscribe at https://calculatedrisk.substack.com/

Most content is available for free (and no Ads), but please subscribe!

Schedule for Week of June 12, 2022

by Calculated Risk on 6/11/2022 08:11:00 AM

The key reports this week are May Retail sales and Housing Starts.

For manufacturing, Industrial Production, and the NY and Philly Fed manufacturing surveys, will be released this week.

The FOMC meets this week, and they are expected to raise rates 50bp.

No major economic releases scheduled.

6:00 AM ET: NFIB Small Business Optimism Index for May.

8:30 AM: The Producer Price Index for May from the BLS. The consensus is for a 0.8% increase in PPI, and a 0.6% increase in core PPI.

7:00 AM ET: The Mortgage Bankers Association (MBA) will release the results for the mortgage purchase applications index.

8:30 AM: Retail sales for May is scheduled to be released. The consensus is for a 0.2% increase in retail sales.

8:30 AM: Retail sales for May is scheduled to be released. The consensus is for a 0.2% increase in retail sales.This graph shows retail sales since 1992. This is monthly retail sales and food service, seasonally adjusted (total and ex-gasoline).

8:30 AM: The New York Fed Empire State manufacturing survey for June. The consensus is for a reading of 4.5, up from -11.6.

10:00 AM: The June NAHB homebuilder survey. The consensus is for a reading of 68, down from 69 last month. Any number below 50 indicates that more builders view sales conditions as poor than good.

2:00 PM: FOMC Meeting Announcement. The FOMC is expected to raise the Fed Funds rate by 50bp at this meeting.

2:00 PM: FOMC Forecasts This will include the Federal Open Market Committee (FOMC) participants' projections of the appropriate target federal funds rate along with the quarterly economic projections.

2:30 PM: Fed Chair Jerome Powell holds a press briefing following the FOMC announcement.

8:30 AM: The initial weekly unemployment claims report will be released. The consensus is for 215 thousand down from 229 thousand last week.

8:30 AM ET: Housing Starts for May.

8:30 AM ET: Housing Starts for May. This graph shows single and total housing starts since 1968.

The consensus is for 1.700 million SAAR, down from 1.724 million SAAR in April.

8:30 AM: the Philly Fed manufacturing survey for June. The consensus is for a reading of 5.3, up from 2.6.

9:15 AM: The Fed will release Industrial Production and Capacity Utilization for May.

9:15 AM: The Fed will release Industrial Production and Capacity Utilization for May.This graph shows industrial production since 1967.

The consensus is for a 0.4% increase in Industrial Production, and for Capacity Utilization to increase to 79.2%.

10:00 AM: State Employment and Unemployment (Monthly) for May 2022

Friday, June 10, 2022

COVID June 10, 2022: Cases, Hospitalizations and Deaths Increasing

by Calculated Risk on 6/10/2022 09:12:00 PM

On COVID (focus on hospitalizations and deaths):

| COVID Metrics | ||||

|---|---|---|---|---|

| Now | Week Ago | Goal | ||

| Percent fully Vaccinated | 66.7% | --- | ≥70.0%1 | |

| Fully Vaccinated (millions) | 221.6 | --- | ≥2321 | |

| New Cases per Day3🚩 | 106,874 | 99,715 | ≤5,0002 | |

| Hospitalized3🚩 | 23,292 | 22,043 | ≤3,0002 | |

| Deaths per Day3🚩 | 291 | 262 | ≤502 | |

| 1 Minimum to achieve "herd immunity" (estimated between 70% and 85%). 2my goals to stop daily posts, 37-day average for Cases, Currently Hospitalized, and Deaths 🚩 Increasing 7-day average week-over-week for Cases, Hospitalized, and Deaths ✅ Goal met. | ||||

Click on graph for larger image.

Click on graph for larger image.This graph shows the daily (columns) and 7-day average (line) of deaths reported.

Average daily deaths bottomed in July 2021 at 214 per day.

30-Year Mortgage Rates increase to 5.85%

by Calculated Risk on 6/10/2022 03:42:00 PM

Today, in the Calculated Risk Real Estate Newsletter: 30-Year Mortgage Rates increase to 5.85%

A brief excerpt:

Mortgagenewsdaily.com reports that as of today, average 30-year fixed mortgage rates are at 5.85% for top tier scenarios. Rates increased today as a result of the inflation report released this morning. Here is a graph from Mortgagenewsdaily.com that shows the 30-year mortgage rate over the last 5 years.There is much more in the article. You can subscribe at https://calculatedrisk.substack.com/

It is the sharp increase in monthly payments - due to sharply higher mortgage rates - that is impacting the housing market.

...

Yesterday, Sam Ro tweeted some analysis from Goldman Sachs on the median monthly payment. This analysis was before the sharp jump in rates today."The median monthly payment of a 30-year mortgage is up 56% year-over-year"

Q2 GDP Forecasts: Close to 3.0%

by Calculated Risk on 6/10/2022 02:29:00 PM

From BofA:

We revised down our 2Q qoq saar growth from 3.0% to 2.5%. [June 10 estimate]From Goldman:

emphasis added

We left our Q2 GDP tracking estimate unchanged at +3.0% (qoq ar). [June 7 estimate]And from the Altanta Fed: GDPNow

The GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the second quarter of 2022 is 0.9 percent on June 8, unchanged from June 7 after rounding. [June 8 estimate]

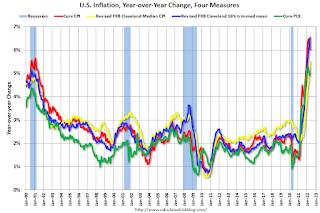

Cleveland Fed: Median CPI increased 0.6% and Trimmed-mean CPI increased 0.8% in May

by Calculated Risk on 6/10/2022 12:13:00 PM

The Cleveland Fed released the median CPI and the trimmed-mean CPI this morning:

According to the Federal Reserve Bank of Cleveland, the median Consumer Price Index rose 0.6% in May. The 16% trimmed-mean Consumer Price Index increased 0.8% in May. "The median CPI and 16% trimmed-mean CPI are measures of core inflation calculated by the Federal Reserve Bank of Cleveland based on data released in the Bureau of Labor Statistics’ (BLS) monthly CPI report".

Note: The Cleveland Fed released the median CPI details here: "Fuel oil and other fuels" increased at 339% annualized rate in May!

Note that Owners' Equivalent Rent and Rent of Primary Residence account for almost 1/3 of median CPI, and these measures were up around 7% annualized in May.

Click on graph for larger image.

Click on graph for larger image.

This graph shows the year-over-year change for these four key measures of inflation.

Click on graph for larger image.

Click on graph for larger image.This graph shows the year-over-year change for these four key measures of inflation.

On a year-over-year basis, the median CPI rose 5.5%, the trimmed-mean CPI rose 6.5%, and the CPI less food and energy rose 6.0%. Core PCE is for April and increased 4.9% year-over-year.

Realtor.com Reports Weekly Inventory Up 13% Year-over-year

by Calculated Risk on 6/10/2022 09:43:00 AM

Realtor.com has monthly and weekly data on the existing home market. Here is their weekly report released yesterday from Chief Economist Danielle Hale: Weekly Housing Trends View — Data Week Ending June 4, 2022. Note: They have data on list prices, new listings and more, but this focus is on inventory.

• Active inventory continued to grow, rising 13% above one year ago. The turnaround in the number of homes for sale continues and year over year growth signals that this is more than just a seasonal improvement. Inventory was roughly on par with last year’s levels at the beginning of May and is now up 13% at the beginning of June. Nevertheless, our May Housing Trends Report showed that the active listings count remained nearly 50 percent below its level at the beginning of the pandemic. In other words, we’re starting to add more options, but home shoppers continue to see a relatively low number of homes for sale.

Here is a graph of the year-over-year change in inventory according to realtor.com. Note: I corrected a sign error in the data for Feb 26, 2022.

Here is a graph of the year-over-year change in inventory according to realtor.com. Note: I corrected a sign error in the data for Feb 26, 2022.Note the rapid increase in the YoY change, from down 30% at the beginning of the year, to up 13% YoY now. It will be important to watch if that trend continues.

BLS: CPI increased 1.0% in May; Core CPI increased 0.6%

by Calculated Risk on 6/10/2022 08:32:00 AM

The Consumer Price Index for All Urban Consumers (CPI-U) increased 1.0 percent in May on a seasonally adjusted basis after rising 0.3 percent in April, the U.S. Bureau of Labor Statistics reported today. Over the last 12 months, the all items index increased 8.6 percent before seasonal adjustment.The consensus was for 0.7% increase in CPI, and a 0.5% increase in core CPI. Both were above expectations. I'll post a graph later today after the Cleveland Fed releases the median and trimmed-mean CPI.

The increase was broad-based, with the indexes for shelter, gasoline, and food being the largest contributors. After declining in April, the energy index rose 3.9 percent over the month with the gasoline index rising 4.1 percent and the other major component indexes also increasing. The food index rose 1.2 percent in May as the food at home index increased 1.4 percent.

The index for all items less food and energy rose 0.6 percent in May, the same increase as in April. While almost all major components increased over the month, the largest contributors were the indexes for shelter, airline fares, used cars and trucks, and new vehicles. The indexes for medical care, household furnishings and operations, recreation, and apparel also increased in May.

The all items index increased 8.6 percent for the 12 months ending May, the largest 12-month increase since the period ending December 1981. The all items less food and energy index rose 6.0 percent over the last 12 months. The energy index rose 34.6 percent over the last year, the largest 12-month increase since the period ending September 2005. The food index increased 10.1 percent for the 12-months ending May, the first increase of 10 percent or more since the period ending March 1981.

emphasis added

Thursday, June 09, 2022

Friday: CPI

by Calculated Risk on 6/09/2022 09:11:00 PM

Friday:

• At 8:30 AM ET, The Consumer Price Index for May from the BLS. The consensus is for 0.7% increase in CPI, and a 0.5% increase in core CPI.

• At 10:00 AM, University of Michigan's Consumer sentiment index (Preliminary for June).

On COVID (focus on hospitalizations and deaths):

| COVID Metrics | ||||

|---|---|---|---|---|

| Now | Week Ago | Goal | ||

| Percent fully Vaccinated | 66.7% | --- | ≥70.0%1 | |

| Fully Vaccinated (millions) | 221.6 | --- | ≥2321 | |

| New Cases per Day3🚩 | 109,032 | 100,915 | ≤5,0002 | |

| Hospitalized3🚩 | 23,341 | 21,693 | ≤3,0002 | |

| Deaths per Day3🚩 | 306 | 258 | ≤502 | |

| 1 Minimum to achieve "herd immunity" (estimated between 70% and 85%). 2my goals to stop daily posts, 37-day average for Cases, Currently Hospitalized, and Deaths 🚩 Increasing 7-day average week-over-week for Cases, Hospitalized, and Deaths ✅ Goal met. | ||||

Click on graph for larger image.

Click on graph for larger image.This graph shows the daily (columns) and 7-day average (line) of deaths reported.

Average daily deaths bottomed in July 2021 at 214 per day.

Hotels: Occupancy Rate Down 12.1% Compared to Same Week in 2019

by Calculated Risk on 6/09/2022 04:17:00 PM

Note: This was lowered by the timing of the holiday.

Reflecting an expected post-Memorial Day holiday slowdown, U.S. hotel performance fell from the previous week, according to STR‘s latest data through June 4.The following graph shows the seasonal pattern for the hotel occupancy rate using the four-week average.

May 29 through June 4, 2022 (percentage change from comparable week in 2019*):

• Occupancy: 63.2% (-12.1%)

• Average daily rate (ADR): $147.35 (+11.3%)

• Revenue per available room (RevPAR): $93.16 (-2.2%)

*Due to the pandemic impact, STR is measuring recovery against comparable time periods from 2019.

emphasis added

Click on graph for larger image.The red line is for 2022, black is 2020, blue is the median, and dashed light blue is for 2021. Dashed purple is 2019 (STR is comparing to a strong year for hotels).

The 4-week average of the occupancy rate is above the median rate for the previous 20 years (Blue).

Note: Y-axis doesn't start at zero to better show the seasonal change.

The 4-week average of the occupancy rate will now mostly move sideways seasonally until the summer.

The Home ATM Still Open in Q1 2022; Closing Soon

by Calculated Risk on 6/09/2022 01:37:00 PM

Today, in the Real Estate Newsletter: The Home ATM Still Open in Q1 2022; Closing Soon

Excerpt:

First, here is the quarterly increase in mortgage debt from the Federal Reserve’s report since 2000. In the mid ‘00s, there was a large increase in mortgage debt associated with the housing bubble.There is much more in the article. You can subscribe at https://calculatedrisk.substack.com/ (All ad free, most content free).

In Q1 2022, mortgage debt increased $222 billion, slightly lower than the three previous quarters. Note the almost 7 years of declining mortgage debt as distressed sales (foreclosures and short sales) wiped out a significant amount of debt.

However, some of this debt is being used to increase the housing stock (purchase new homes), so this isn’t all MEW.

...

The bottom line is the recent increase in MEW is not concerning - it is far less as a percent of disposable personal income than during the bubble, and most homeowners have substantial equity.

Also, it is very likely that MEW will decrease sharply in 2022 as refinance activity declines due to higher mortgage rates. I expect significantly lower levels of MEW in the last three quarters of2022.

Fed's Flow of Funds: Household Net Worth Decreased $0.55 Trillion in Q1

by Calculated Risk on 6/09/2022 12:22:00 PM

The Federal Reserve released the Q1 2022 Flow of Funds report today: Financial Accounts of the United States.

The net worth of households and nonprofits fell to $149.3 trillion during the first quarter of 2022. The value of directly and indirectly held corporate equities decreased $3.0 trillion and the value of real estate increased $1.7 trillion.

...

Household debt increased 8.3 percent at an annual rate in the first quarter of 2022. Consumer credit grew at an annual rate of 8.7 percent, while mortgage debt (excluding charge-offs) grew at an annual rate of 8.6 percent.

Click on graph for larger image.

Click on graph for larger image.The first graph shows Households and Nonprofit net worth as a percent of GDP.

Net worth as a percent of GDP is down slightly from the all-time high in Q4.

This includes real estate and financial assets (stocks, bonds, pension reserves, deposits, etc) net of liabilities (mostly mortgages). Note that this does NOT include public debt obligations.

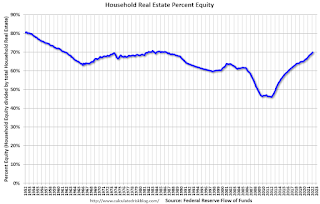

This graph shows homeowner percent equity since 1952.

This graph shows homeowner percent equity since 1952.

Household percent equity (as measured by the Fed) collapsed when house prices fell sharply in 2007 and 2008.

In Q1 2022, household percent equity (of household real estate) was at 69.9% - up from 69.2% in Q4, 2021. This is the highest percent equity since the 1980s.

Note: This includes households with no mortage debt.

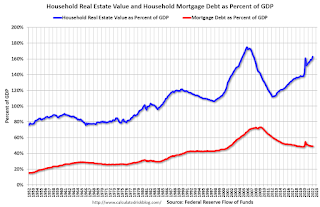

The third graph shows household real estate assets and mortgage debt as a percent of GDP. Note this graph was impacted by the sharp decline in Q2 2020 GDP.

The third graph shows household real estate assets and mortgage debt as a percent of GDP. Note this graph was impacted by the sharp decline in Q2 2020 GDP.

Mortgage debt increased by $222 billion in Q1.

Mortgage debt is up $1.27 trillion from the peak during the housing bubble, but, as a percent of GDP is at 49.1% - up from Q4 - and down from a peak of 73.3% of GDP during the housing bust.

The value of real estate, as a percent of GDP, increased in Q1, and is well above the average of the last 30 years.

This graph shows homeowner percent equity since 1952.

This graph shows homeowner percent equity since 1952. Household percent equity (as measured by the Fed) collapsed when house prices fell sharply in 2007 and 2008.

In Q1 2022, household percent equity (of household real estate) was at 69.9% - up from 69.2% in Q4, 2021. This is the highest percent equity since the 1980s.

Note: This includes households with no mortage debt.

The third graph shows household real estate assets and mortgage debt as a percent of GDP. Note this graph was impacted by the sharp decline in Q2 2020 GDP.

The third graph shows household real estate assets and mortgage debt as a percent of GDP. Note this graph was impacted by the sharp decline in Q2 2020 GDP.Mortgage debt increased by $222 billion in Q1.

Mortgage debt is up $1.27 trillion from the peak during the housing bubble, but, as a percent of GDP is at 49.1% - up from Q4 - and down from a peak of 73.3% of GDP during the housing bust.

The value of real estate, as a percent of GDP, increased in Q1, and is well above the average of the last 30 years.

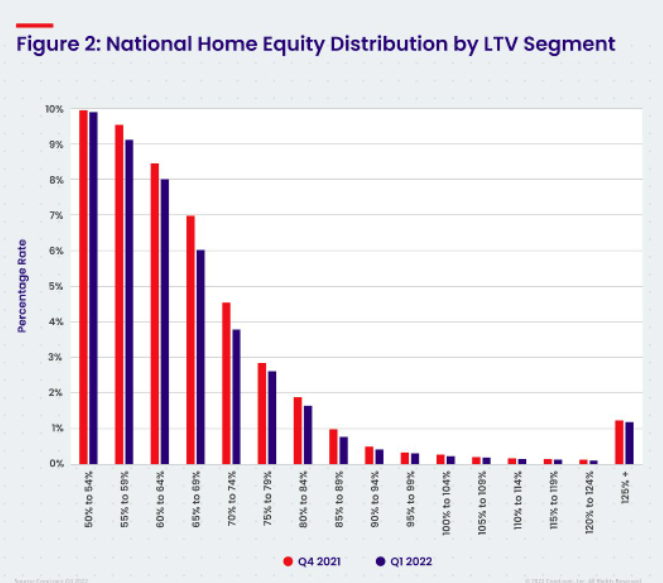

CoreLogic: 1.1 million Homeowners with Negative Equity in Q1 2022

by Calculated Risk on 6/09/2022 10:38:00 AM

From CoreLogic: US Homeowners Gained Over $60,000 in Equity Per Borrower in Q1 2022 as Historic Home Price Growth Continues, CoreLogic Reports

CoreLogic® ... today released the Homeowner Equity Report (HER) for the first quarter of 2022. The report shows U.S. homeowners with mortgages (which account for roughly 62% of all properties) have seen their equity increase by 32.2% year over year, representing a collective equity gain of $3.8 trillion, and an average gain of $63,600 per borrower, since the first quarter of 2021.

...

“Price growth is the key ingredient for the creation of home equity wealth,” said Patrick Dodd, president and CEO at CoreLogic. “Home prices were up by 20% in March compared to one year earlier in CoreLogic’s national Home Price Index. This has led to the largest one-year gain in average home equity wealth for owners and is expected to spur a record amount of home-improvement spending this year.”

Negative equity, also referred to as underwater or upside-down mortgages, applies to borrowers who owe more on their mortgages than their homes are currently worth. As of the first quarter of 2022, the quarterly and annual changes in negative equity were:

• Quarterly change: From the fourth quarter of 2021 to the first quarter of 2022, the total number of mortgaged homes in negative equity decreased by 5.3% to 1.1 million homes, or 2% of all mortgaged properties.

• Annual change: In the first quarter of 2021, 1.4 million homes, or 2.6% of all mortgaged properties, were in negative equity. This number decreased by 23%, or approximately 300,000 properties, in the first quarter of 2022.

Because home equity is affected by home price changes, borrowers with equity positions near (+/- 5%) the negative equity cutoff are most likely to move out of or into negative equity as prices change, respectively. Looking at the first quarter of 2022 book of mortgages, if home prices increase by 5%, 130,000 homes would regain equity; if home prices decline by 5%, 167,000 properties would fall underwater.

emphasis added

Click on graph for larger image.

Click on graph for larger image.This graph from CoreLogic compares Q1 2022 to Q4 2021 equity distribution by LTV. There are still a few properties with LTV over 125%. But most homeowners have a significant amount of equity. This is a very different picture than at the start of the housing bust when many homeowners had little equity.

On a year-over-year basis, the number of homeowners with negative equity has declined from 1.4 million to 1.1 million.