RSS Feed

RSS Feed by Calculated Risk on 7/11/2022 10:15:00 AM

Monday, July 11, 2022

Housing Inventory July 11th Update: Up 32% Year-over-year

Inventory is increasing rapidly. Inventory bottomed seasonally at the beginning of March 2022 and is now up 104% since then. More than double!

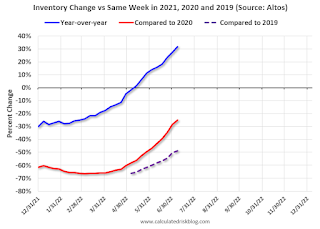

Altos reports inventory is up 31.7% year-over-year and is now 12.3% above the peak last year.

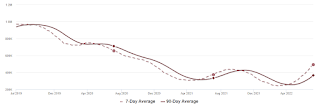

Click on graph for larger image.

Click on graph for larger image.

This inventory graph is courtesy of Altos Research.

Click on graph for larger image.

Click on graph for larger image.This inventory graph is courtesy of Altos Research.

As of July 8th, inventory was at 491 thousand (7-day average), compared to 476 thousand the prior week.

Inventory is usually flat - or declines slightly - over the 4th of July weekend. This year inventory was up 3.2% from the previous week. Inventory is increasing much faster than normal for this time of year (both in percentage terms and in total inventory added).

Inventory is still historically low. Compared to the same week in 2021, inventory is up 31.7% from 373 thousand, however compared to the same week in 2020 inventory is down 25.0% from 654 thousand. Compared to 3 years ago, inventory is down 48.9% from 961 thousand.

Here are the inventory milestones I’m watching for with the Altos data:

1. The seasonal bottom (happened on March 4th for Altos) ✅

2. Inventory up year-over-year (happened on May 13th for Altos) ✅

3. Inventory up compared to two years ago (currently down 25.0% according to Altos)

4. Inventory up compared to 2019 (currently down 48.9%).

1. The seasonal bottom (happened on March 4th for Altos) ✅

2. Inventory up year-over-year (happened on May 13th for Altos) ✅

3. Inventory up compared to two years ago (currently down 25.0% according to Altos)

4. Inventory up compared to 2019 (currently down 48.9%).

Here is a graph of the inventory change vs 2021, 2020 (milestone 3 above) and 2019 (milestone 4).

The blue line is the year-over-year data, the red line is compared to two years ago, and dashed purple is compared to 2019.

Two years ago (in 2020) inventory was declining all year, so the two-year comparison will get easier all year.

Based on the recent increases in inventory, my current estimate is inventory will be up compared to 2020 in late August of this year (in the next couple of months), and back to 2019 levels at the beginning of 2023.

Mike Simonsen discusses this data regularly on Youtube.

Five High Frequency Indicators for the Economy

by Calculated Risk on 7/11/2022 08:30:00 AM

These indicators are mostly for travel and entertainment. It is interesting to watch these sectors recover as the pandemic subsides. Notes: I've added back gasoline supplied to see if there is an impact from higher gasoline prices. Apple has discontinued "Apple mobility", and restaurant traffic is mostly back to normal.

The TSA is providing daily travel numbers.

This data is as of July 10th.

Click on graph for larger image.

Click on graph for larger image.This data shows the 7-day average of daily total traveler throughput from the TSA for 2019 (Light Blue), 2020 (Black), 2021 (Blue) and 2022 (Red).

The dashed line is the percent of 2019 for the seven-day average.

The 7-day average is down 14.4% from the same day in 2019 (85.6% of 2019). (Dashed line)

Air travel - as a percent of 2019 - has been moving sideways over the last several months, off about 10% from 2019 - with some ups and downs, usually related to timing of holidays.

This data shows domestic box office for each week and the median for the years 2016 through 2019 (dashed light blue).

This data shows domestic box office for each week and the median for the years 2016 through 2019 (dashed light blue). Black is 2020, Blue is 2021 and Red is 2022.

The data is from BoxOfficeMojo through July 7th.

Note that the data is usually noisy week-to-week and depends on when blockbusters are released.

Movie ticket sales were at $206 million last week, down about 39% from the median for the week.

Note that the data is usually noisy week-to-week and depends on when blockbusters are released.

Movie ticket sales were at $206 million last week, down about 39% from the median for the week.

This graph shows the seasonal pattern for the hotel occupancy rate using the four-week average.

This graph shows the seasonal pattern for the hotel occupancy rate using the four-week average. The red line is for 2022, black is 2020, blue is the median, and dashed light blue is for 2021. Dashed purple is 2019 (STR is comparing to a strong year for hotels).

This data is through July 2nd. The occupancy rate was up 2.9% compared to the same week in 2019.

The 4-week average of the occupancy rate is at the median rate for the previous 20 years (Blue).

Notes: Y-axis doesn't start at zero to better show the seasonal change.

Notes: Y-axis doesn't start at zero to better show the seasonal change.

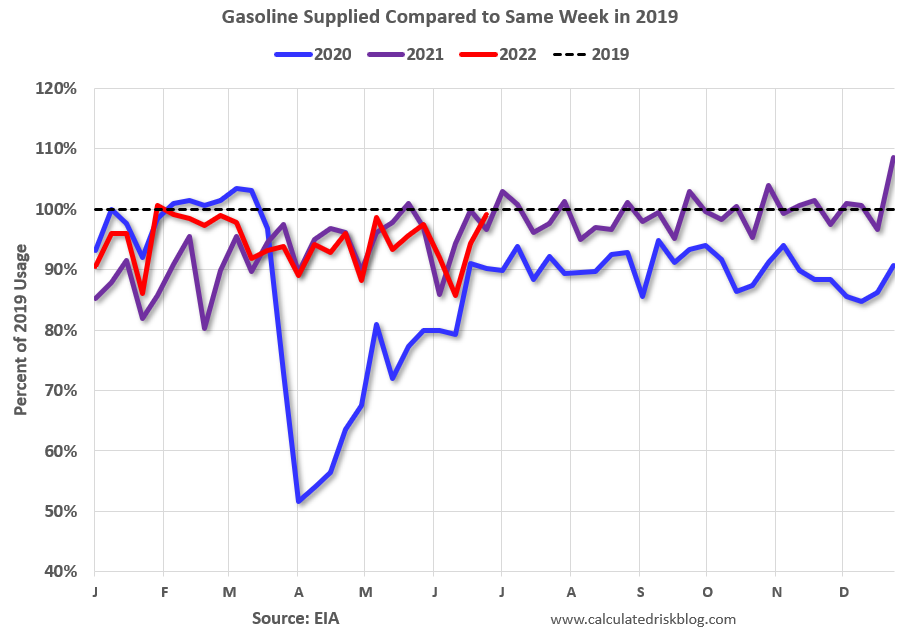

This graph, based on weekly data from the U.S. Energy Information Administration (EIA), shows gasoline supplied compared to the same week of 2019.

Blue is for 2020. Purple is for 2021, and Red is for 2022.

As of July 1st, gasoline supplied was down 0.8% compared to the same week in 2019.

Recently gasoline supplied has been running somewhat below 2019 levels.

Here is some interesting data on New York subway usage (HT BR).

This graph is from Todd W Schneider.

This graph is from Todd W Schneider. This graph shows weekly turnstile entries since 2015.

Currently traffic is less than half of normal.

Currently traffic is less than half of normal.

This data is through Friday, July 8th.

He notes: "Data updates weekly from the MTA’s public turnstile data, usually on Saturday mornings".

Sunday, July 10, 2022

Sunday Night Futures

by Calculated Risk on 7/10/2022 08:19:00 PM

Weekend:

• Schedule for Week of July 10, 2022

Monday:

• No major economic releases scheduled.

From CNBC: Pre-Market Data and Bloomberg futures S&P 500 and DOW futures are down slightly (fair value).

Oil prices were down over the last week with WTI futures at $104.79 per barrel and Brent at $107.02 per barrel. A year ago, WTI was at $75, and Brent was at $77 - so WTI oil prices are up 40% year-over-year.

Here is a graph from Gasbuddy.com for nationwide gasoline prices. Nationally prices are at $4.67 per gallon. A year ago, prices were at $3.12 per gallon, so gasoline prices are up $1.55 per gallon year-over-year.

Hotels: Occupancy Rate Up 2.9% Compared to Same Week in 2019

by Calculated Risk on 7/10/2022 08:11:00 AM

From CoStar: STR: US Hotel Performance Dips Ahead of Independence Day but Outpaces Pre-Pandemic Levels

U.S. hotel performance dipped from the previous week, while indexed comparisons against 2019 improved on the favorable side of a holiday calendar shift, according to STR‘s latest data through July 2.The following graph shows the seasonal pattern for the hotel occupancy rate using the four-week average.

June 26 to July 2, 2022 (percentage change from comparable week in 2019*):

• Occupancy: 67.3% (+2.9%)

• Average daily rate (ADR): $153.32 (+19.7%)

• Revenue per available room (RevPAR): $103.24 (+23.1%)

Given historical trends, the week-over-week decline in demand was normal given the holiday. Since 2000, the Fourth of July or the observance of the holiday (federal holiday) has fallen on a Monday seven times, including last year and in 2016. In every case, occupancy in the week before the holiday fell by more than four percentage points with most of the losses beginning on Wednesday and continuing into the weekend. Occupancy and demand are likely to fall again for this current week before strengthening in the remaining weeks of July.

*Due to the pandemic impact, STR is measuring recovery against comparable time periods from 2019.

emphasis added

Click on graph for larger image.The red line is for 2022, black is 2020, blue is the median, and dashed light blue is for 2021. Dashed purple is 2019 (STR is comparing to a strong year for hotels).

The 4-week average of the occupancy rate is at the median rate for the previous 20 years (Blue).

Note: Y-axis doesn't start at zero to better show the seasonal change.

The 4-week average of the occupancy rate will increase seasonally over the next couple of months.

Saturday, July 09, 2022

Real Estate Newsletter Articles this Week

by Calculated Risk on 7/09/2022 02:11:00 PM

At the Calculated Risk Real Estate Newsletter this week:

• House Price Declines: How Long for Real Prices to Recover?

• 30-Year Mortgage Rates Decrease to 5.50%

• Black Knight Mortgage Monitor: "Early signs of cooling in the housing market"

• 1st Look at Local Housing Markets in June

• Apartment Vacancy Rate Declined in Q2

This is usually published 4 to 6 times a week and provides more in-depth analysis of the housing market.

You can subscribe at https://calculatedrisk.substack.com/

Most content is available for free (and no Ads), but please subscribe!

AAR: June Rail Carloads and Intermodal Down Year-over-year

by Calculated Risk on 7/09/2022 08:11:00 AM

From the Association of American Railroads (AAR) Rail Time Indicators. Graphs and excerpts reprinted with permission.

In June, total U.S. carloads fell 1.5% from last year, their third consecutive monthly decline. ...

U.S intermodal originations in June were down 4.6% from last year, their fifth decline in 2022’s first six months.

emphasis added

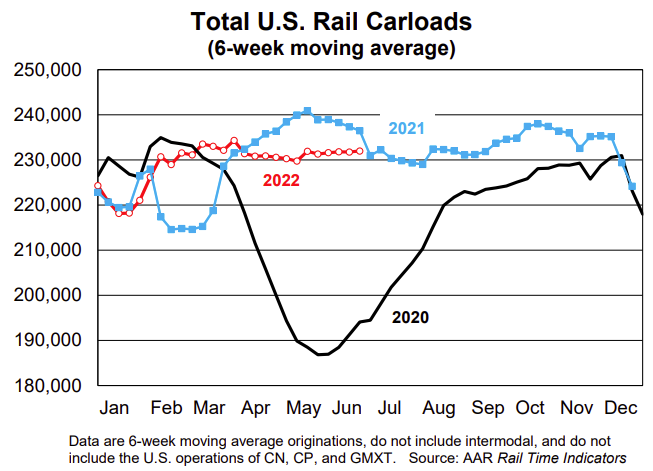

Click on graph for larger image.

Click on graph for larger image.This graph from the Rail Time Indicators report shows the six-week average of U.S. Carloads in 2020, 2021 and 2022:

U.S. railroads originated 1.16 million total carloads in June 2022, down 1.5% from June 2021. It’s the third consecutive year-over-year decline and the fourth in the first six months of 2022. In 2022’s second quarter, total carloads were down 2.7% from last year; in the first half, they were down 0.1%. Since 1988, when our data begin, only 2020 had fewer first-half carloads than 2022.

The second graph shows the six-week average (not monthly) of U.S. intermodal in 2020, 2021 and 2022: (using intermodal or shipping containers):

The second graph shows the six-week average (not monthly) of U.S. intermodal in 2020, 2021 and 2022: (using intermodal or shipping containers):U.S railroads also originated 1.32 million intermodal units in June, down 4.6% from last year. It’s the fifth decline in 2022’s first six months and the 10th in the past 11 months. Intermodal originations averaged 264,624 per week in June 2022, the fewest in four months.

Schedule for Week of July 10, 2022

by Calculated Risk on 7/09/2022 08:11:00 AM

The key reports this week are June CPI and retail sales.

For manufacturing, the June Industrial Production report and the July New York Fed manufacturing survey will be released.

No major economic releases scheduled.

6:00 AM ET: NFIB Small Business Optimism Index for June.

7:00 AM ET: The Mortgage Bankers Association (MBA) will release the results for the mortgage purchase applications index.

8:30 AM: The Consumer Price Index for June from the BLS. The consensus is for a 1.1% increase in CPI, and a 0.6% increase in core CPI. The consensus is for CPI to be up 8.8% year-over-year and core CPI to be up 5.8% YoY.

2:00 PM: the Federal Reserve Beige Book, an informal review by the Federal Reserve Banks of current economic conditions in their Districts.

8:30 AM: The initial weekly unemployment claims report will be released. The consensus is for 230 thousand down from 235 thousand last week.

8:30 AM: The Producer Price Index for June from the BLS. The consensus is for a 0.8% increase in PPI, and a 0.5% increase in core PPI.

8:30 AM: Retail sales for June is scheduled to be released. The consensus is for 0.8% increase in retail sales.

8:30 AM: Retail sales for June is scheduled to be released. The consensus is for 0.8% increase in retail sales.This graph shows retail sales since 1992. This is monthly retail sales and food service, seasonally adjusted (total and ex-gasoline).

Retail sales ex-gasoline were down 0.3% in May.

8:30 AM: The New York Fed Empire State manufacturing survey for July. The consensus is for a reading of -2.6, down from -1.2.

9:15 AM: The Fed will release Industrial Production and Capacity Utilization for June.

9:15 AM: The Fed will release Industrial Production and Capacity Utilization for June.This graph shows industrial production since 1967.

The consensus is for a no change in Industrial Production, and for Capacity Utilization to decrease to 80.4%.

10:00 AM: University of Michigan's Consumer sentiment index (Preliminary for July).

Friday, July 08, 2022

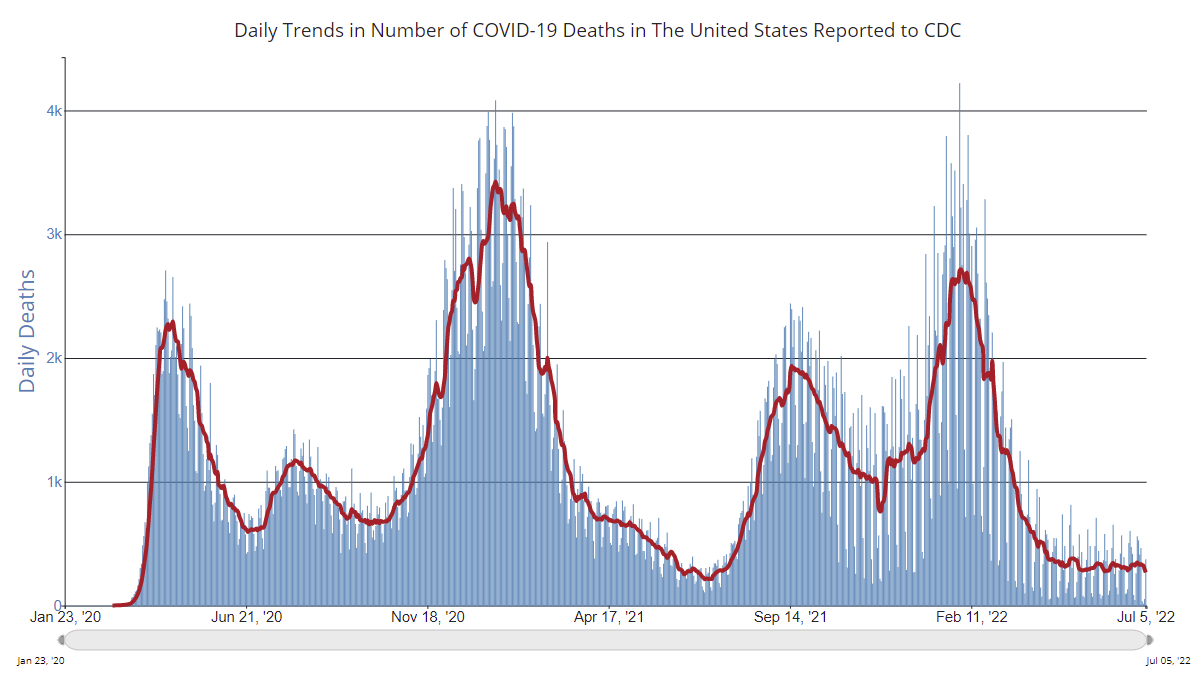

COVID July 8, 2022, Update on Cases, Hospitalizations and Deaths

by Calculated Risk on 7/08/2022 09:27:00 PM

On COVID (focus on hospitalizations and deaths):

| COVID Metrics | ||||

|---|---|---|---|---|

| Now | Week Ago | Goal | ||

| Percent fully Vaccinated | 67.0% | --- | ≥70.0%1 | |

| Fully Vaccinated (millions) | 222.5 | --- | ≥2321 | |

| New Cases per Day3 | 106,021 | 112,330 | ≤5,0002 | |

| Hospitalized3🚩 | 29,327 | 27,322 | ≤3,0002 | |

| Deaths per Day3 | 277 | 341 | ≤502 | |

| 1 Minimum to achieve "herd immunity" (estimated between 70% and 85%). 2my goals to stop daily posts, 37-day average for Cases, Currently Hospitalized, and Deaths 🚩 Increasing 7-day average week-over-week for Cases, Hospitalized, and Deaths ✅ Goal met. | ||||

Click on graph for larger image.

Click on graph for larger image.This graph shows the daily (columns) and 7-day average (line) of deaths reported.

Average daily deaths bottomed in July 2021 at 214 per day.

Used Vehicle Wholesale Prices Decreased 1.3% in June

by Calculated Risk on 7/08/2022 03:23:00 PM

From Manheim Consulting today: Wholesale Used-Vehicle Prices Decrease in June from Seasonal Adjustment

Wholesale used-vehicle prices (on a mix-, mileage-, and seasonally adjusted basis) decreased 1.3% in June from May. The Manheim Used Vehicle Value Index declined to 219.9, up 9.7% from a year ago. The non-adjusted price change in June decreased 1.8% compared to May, leaving the unadjusted average price up 10.7% year over year.

In June, Manheim Market Report (MMR) values saw larger declines over the last two weeks than the prior two weeks.

emphasis added

Click on graph for larger image.

Click on graph for larger image.This index from Manheim Consulting is based on all completed sales transactions at Manheim’s U.S. auctions.

The Manheim index suggests used car prices decreased in June and are up 9.7% year-over-year (YoY).

The YoY change is mostly getting smaller. This index was up 45% YoY in January, and now up less than 10% YoY.

Apartment Vacancy Rate Declined in Q2

by Calculated Risk on 7/08/2022 01:25:00 PM

Today, in the Calculated Risk Real Estate Newsletter: Apartment Vacancy Rate Declined in Q2

A brief excerpt:

Moody’s Analytics Reis reported that the apartment vacancy rate was at 4.5% in Q2 2022, down from 4.7% in Q1, and down from a pandemic peak of 5.4% in both Q1 and Q2 2021.There is more in the article. You can subscribe at https://calculatedrisk.substack.com/

...

This graph shows the apartment vacancy rate starting in 1980. (Annual rate before 1999, quarterly starting in 1999). Note: Moody’s Analytics is just for large cities. ...

Click on graph for larger image.

Moody’s Analytics also reported the effective rents were up 2.8% in Q2 from Q1, and up 17.5% year-over-year. Last week, I posted a graph of the year-over-year change for various measures of rent. The Zillow measure is up 15.9% YoY in May, down from 16.6% YoY in April. This is down from a peak of 17.2% YoY in February. The ApartmentList measure is up 14.1% YoY as of June, down from 15.4% in May. This is down from the peak of 17.8% YoY last December.

Q2 GDP Forecasts: Slightly Negative

by Calculated Risk on 7/08/2022 12:22:00 PM

Note: We've seen two consecutive quarters of negative GDP before without a recession (that isn't the definition). If Q2 is negative, it will mostly be due to inventory and trade issues. No worries. My view is the US economy is not currently in a recession, see: Predicting the Next Recession

From BofA:

We are now tracking -1.2% qoq saar growth for 2Q, down from 0.0% qoq saar previously.From Goldman:

It is reasonable to dismiss some of the signal from the GDP declines that may have taken place in the first two quarters of the year on account of the large negative contributions from net trade and inventories. In addition, there is a larger-than-normal gap between GDP and GDI which, historically, has been resolved by GDP getting revised toward GDI, suggesting that some of the as-reported weakness in activity may get revised away over time. [July 8 estimate]

emphasis added

We left our Q2 GDP tracking estimate unchanged at +0.7% (qoq ar). [July 8 estimate]And from the Altanta Fed: GDPNow

The GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the second quarter of 2022 is -1.2 percent on July 8, up from -1.9 percent on July 7. [July 8 estimate]

Comments on June Employment Report

by Calculated Risk on 7/08/2022 09:27:00 AM

The headline jobs number in the June employment report was above expectations, however employment for the previous two months was revised down by 74,000. The participation rate and the employment-population ratio both decreased slightly, and the unemployment rate was unchanged at 3.6%.

Excluding leisure and hospitality, the economy has 800 thousand more jobs then prior to the pandemic.

Leisure and hospitality gained 67 thousand jobs in June. At the beginning of the pandemic, in March and April of 2020, leisure and hospitality lost 8.20 million jobs, and are now down 1.32 million jobs since February 2020. So, leisure and hospitality has now added back about 84% all of the jobs lost in March and April 2020.

Construction employment increased 13 thousand and is now 46 thousand above the pre-pandemic level.

Manufacturing added 29 thousand jobs and is now 12 thousand above the pre-pandemic level.

Earlier: June Employment Report: 372 thousand Jobs, 3.6% Unemployment Rate

In June, the year-over-year employment change was 6.3 million jobs.

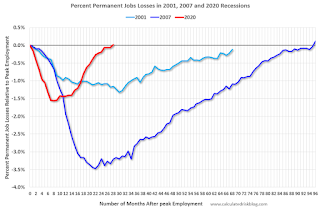

Permanent Job Losers

Click on graph for larger image.

Click on graph for larger image.

This graph shows permanent job losers as a percent of the pre-recession peak in employment through the report today.

In June, the year-over-year employment change was 6.3 million jobs.

Permanent Job Losers

Click on graph for larger image.

Click on graph for larger image.This graph shows permanent job losers as a percent of the pre-recession peak in employment through the report today.

This data is only available back to 1994, so there is only data for three recessions.

In June, the number of permanent job losers declined to 1.273 million from 1.386 million in the previous month.

In June, the number of permanent job losers declined to 1.273 million from 1.386 million in the previous month.

These jobs were likely the hardest to recover, so it is a positive that there are fewer permanent job losers now than prior to the recession.

Prime (25 to 54 Years Old) Participation

Since the overall participation rate has declined due to cyclical (recession) and demographic (aging population, younger people staying in school) reasons, here is the employment-population ratio for the key working age group: 25 to 54 years old.

Since the overall participation rate has declined due to cyclical (recession) and demographic (aging population, younger people staying in school) reasons, here is the employment-population ratio for the key working age group: 25 to 54 years old.The 25 to 54 participation rate decreased in June to 82.3% from 82.6% in May, and the 25 to 54 employment population ratio decreased to 79.8% from 80.0% the previous month.

Both are slightly below the pre-pandemic levels and indicate almost all of the prime age workers have returned to the labor force.

Part Time for Economic Reasons

From the BLS report:

From the BLS report:

These workers are included in the alternate measure of labor underutilization (U-6) that decreased to 6.7% from 7.1% in the previous month. This is down from the record high in April 22.9% for this measure since 1994. This measure is lower than the 7.0% in February 2020 (pre-pandemic).

Unemployed over 26 Weeks

This graph shows the number of workers unemployed for 27 weeks or more.

This graph shows the number of workers unemployed for 27 weeks or more.

According to the BLS, there are 1.336 million workers who have been unemployed for more than 26 weeks and still want a job, down from 1.356 million the previous month.

This does not include all the people that left the labor force.

Summary:

The headline monthly jobs number was above expectations; however, the previous two months were revised down by 74,000 combined.

Part Time for Economic Reasons

From the BLS report:

From the BLS report:"The number of persons employed part time for economic reasons declined by 707,000 to 3.6 million in June and is below its February 2020 level of 4.4 million. These individuals, who would have preferred full-time employment, were working part time because their hours had been reduced or they were unable to find full-time jobs."The number of persons working part time for economic reasons decreased in June to 3.621 million from 4.328 million in May. This is below pre-recession levels.

These workers are included in the alternate measure of labor underutilization (U-6) that decreased to 6.7% from 7.1% in the previous month. This is down from the record high in April 22.9% for this measure since 1994. This measure is lower than the 7.0% in February 2020 (pre-pandemic).

Unemployed over 26 Weeks

This graph shows the number of workers unemployed for 27 weeks or more.

This graph shows the number of workers unemployed for 27 weeks or more. According to the BLS, there are 1.336 million workers who have been unemployed for more than 26 weeks and still want a job, down from 1.356 million the previous month.

This does not include all the people that left the labor force.

Summary:

The headline monthly jobs number was above expectations; however, the previous two months were revised down by 74,000 combined.

The headline unemployment rate was unchanged at 3.6%.

Look at these highlights:

• U-6 is below pre-recession levels, and the lowest level on record (started in 1994).

• There are now fewer permanent job losers than prior to the recession.

• There are fewer part time workers, for economic reasons, than prior to the recession.

However, there are still 524 thousand fewer jobs than prior to the recession.

Overall, this was another strong report.

June Employment Report: 372 thousand Jobs, 3.6% Unemployment Rate

by Calculated Risk on 7/08/2022 08:40:00 AM

From the BLS:

Total nonfarm payroll employment rose by 372,000 in June, and the unemployment rate remained at 3.6 percent, the U.S. Bureau of Labor Statistics reported today. Notable job gains occurred in professional and business services, leisure and hospitality, and health care.

...

The change in total nonfarm payroll employment for April was revised down by 68,000, from +436,000 to +368,000, and the change for May was revised down by 6,000, from +390,000 to +384,000. With these revisions, employment in April and May combined is 74,000 lower than previously reported.

emphasis added

Click on graph for larger image.

Click on graph for larger image.The first graph shows the job losses from the start of the employment recession, in percentage terms.

The current employment recession was by far the worst recession since WWII in percentage terms.

However, 28 months after the onset of the current employment recession, almost all of the jobs have returned.

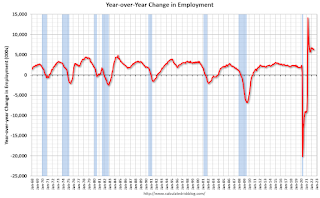

The second graph shows the year-over-year change in total non-farm employment since 1968.

The second graph shows the year-over-year change in total non-farm employment since 1968.

In June, the year-over-year change was 6.3 million jobs. This was up significantly year-over-year.

Total payrolls increased by 372 thousand in June. Private payrolls increased by 381 thousand, and public payrolls decreased 9 thousand.

Payrolls for April and May were revised down 74 thousand, combined.

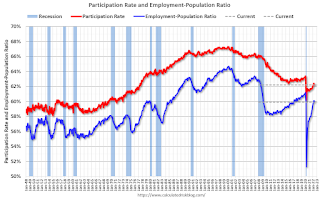

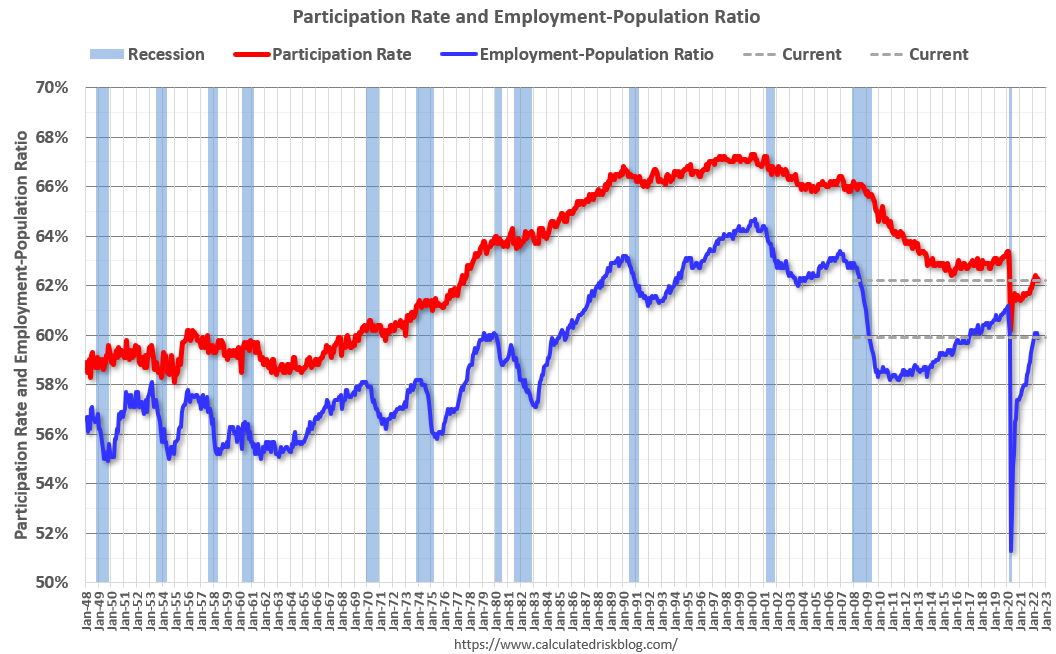

The third graph shows the employment population ratio and the participation rate.

The Labor Force Participation Rate decreased to 62.2% in June, from 62.3% in May. This is the percentage of the working age population in the labor force.

The Labor Force Participation Rate decreased to 62.2% in June, from 62.3% in May. This is the percentage of the working age population in the labor force.

The Employment-Population ratio decreased to 59.9% from 60.1% (blue line).

I'll post the 25 to 54 age group employment-population ratio graph later.

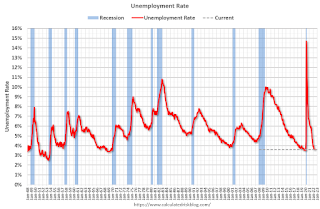

The fourth graph shows the unemployment rate.

The fourth graph shows the unemployment rate.

The unemployment rate was unchanged in June at 3.6% from 3.6% in May.

This was above consensus expectations; however, April and May payrolls were revised down by 74,000 combined.

The second graph shows the year-over-year change in total non-farm employment since 1968.

The second graph shows the year-over-year change in total non-farm employment since 1968.In June, the year-over-year change was 6.3 million jobs. This was up significantly year-over-year.

Total payrolls increased by 372 thousand in June. Private payrolls increased by 381 thousand, and public payrolls decreased 9 thousand.

Payrolls for April and May were revised down 74 thousand, combined.

The third graph shows the employment population ratio and the participation rate.

The Labor Force Participation Rate decreased to 62.2% in June, from 62.3% in May. This is the percentage of the working age population in the labor force.

The Labor Force Participation Rate decreased to 62.2% in June, from 62.3% in May. This is the percentage of the working age population in the labor force. The Employment-Population ratio decreased to 59.9% from 60.1% (blue line).

I'll post the 25 to 54 age group employment-population ratio graph later.

The fourth graph shows the unemployment rate.

The fourth graph shows the unemployment rate. The unemployment rate was unchanged in June at 3.6% from 3.6% in May.

This was above consensus expectations; however, April and May payrolls were revised down by 74,000 combined.

I'll have more later ...

Thursday, July 07, 2022

Friday: Employment Report

by Calculated Risk on 7/07/2022 09:11:00 PM

My June Employment Preview

Goldman June Payrolls Preview

Friday:

• At 8:30 AM ET, Employment Report for June. The consensus is for 270,000 jobs added, and for the unemployment rate to be unchanged at 3.6%

On COVID (focus on hospitalizations and deaths):

| COVID Metrics | ||||

|---|---|---|---|---|

| Now | Week Ago | Goal | ||

| Percent fully Vaccinated | 66.9% | --- | ≥70.0%1 | |

| Fully Vaccinated (millions) | 222.3 | --- | ≥2321 | |

| New Cases per Day3 | 106,549 | 110,875 | ≤5,0002 | |

| Hospitalized3🚩 | 28,891 | 26,959 | ≤3,0002 | |

| Deaths per Day3 | 273 | 345 | ≤502 | |

| 1 Minimum to achieve "herd immunity" (estimated between 70% and 85%). 2my goals to stop daily posts, 37-day average for Cases, Currently Hospitalized, and Deaths 🚩 Increasing 7-day average week-over-week for Cases, Hospitalized, and Deaths ✅ Goal met. | ||||

Click on graph for larger image.

Click on graph for larger image.This graph shows the daily (columns) and 7-day average (line) of deaths reported.

Average daily deaths bottomed in July 2021 at 214 per day.

Goldman June Payrolls Preview

by Calculated Risk on 7/07/2022 03:48:00 PM

A few brief excerpts from a note by Goldman Sachs economist Spencer Hill:

We estimate nonfarm payrolls rose 250k in June ... employment surveys and Big Data employment indicators generally weakened in the month, and the Challenger report showed an increase in job cuts—particularly in real estate, autos, and media. ... We estimate an unchanged unemployment rate at 3.6%—in line with consensus—reflecting a solid rise in household employment offset by a 0.1pp rise in labor force participation to 62.4%.CR Note: The consensus is for 270 thousand jobs added, and for the unemployment rate to be unchanged at 3.6%.

emphasis added

June Employment Preview

by Calculated Risk on 7/07/2022 12:18:00 PM

On Friday at 8:30 AM ET, the BLS will release the employment report for June. The consensus is for 270,000 jobs added, and for the unemployment rate to be unchanged at 3.6%.

Click on graph for larger image.

Click on graph for larger image.• First, currently there are still about 800 thousand fewer jobs than in February 2020 (the month before the pandemic).

This graph shows the job losses from the start of the employment recession, in percentage terms.

The current employment recession was by far the worst recession since WWII in percentage terms. However, the current employment recession, 27 months after the onset, has recovered quicker than the previous two recessions.

• ADP Report: The ADP employment report has been "paused" and is being retooled.

• ISM Surveys: Note that the ISM services are diffusion indexes based on the number of firms hiring (not the number of hires). The ISM® manufacturing employment index decreased in June to 47.3%, down from 50.9% last month. This would suggest 35,000 jobs lost in manufacturing.

The ISM® services employment index decreased in June to 47.4%, down from 50.2% last month. This would suggest service employment was unchanged in June.

Combined, the ISM surveys suggest 35,000 jobs lost in June.

• Unemployment Claims: The weekly claims report showed an increase in the number of initial unemployment claims during the reference week (includes the 12th of the month) from 218,000 in May to 233,000 in June. This would usually suggest a few more layoffs in June than in May. In general, weekly claims were above expectations in June.

• Permanent Job Losers: Something to watch in the employment report will be "Permanent job losers". This graph shows permanent job losers as a percent of the pre-recession peak in employment through the May report.

• Permanent Job Losers: Something to watch in the employment report will be "Permanent job losers". This graph shows permanent job losers as a percent of the pre-recession peak in employment through the May report.This data is only available back to 1994, so there is only data for three recessions. In May, the number of permanent job losers was unchanged at 1.386 million from 1.386 million in the previous month.

These jobs will likely be the hardest to recover, so it is a positive that the number of permanent job losers is declining fairly rapidly.

• COVID: As far as the pandemic, the number of daily cases during the reference week in June was around 105,000, up from 90,000 in May.

• Conclusion: The consensus is for job growth to slow to 270,000 jobs added in June. Overall, the ISM surveys were negative, and unemployment claims increased during the reference week. This suggests a weaker than expected employment report for June.

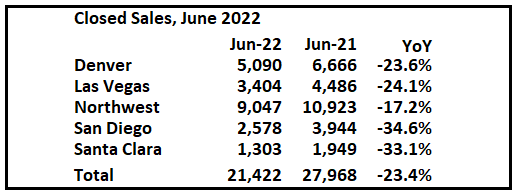

1st Look at Local Housing Markets in June, Sales Down Sharply

by Calculated Risk on 7/07/2022 10:05:00 AM

Today, in the Calculated Risk Real Estate Newsletter: 1st Look at Local Housing Markets in June, Sales Down Sharply

A brief excerpt:

From Denver Metro Association of Realtors® (DMAR): DMAR Real Estate Market Trends ReportThere is much more in the article. You can subscribe at https://calculatedrisk.substack.com/As month-end active inventory skyrockets, the Denver Metro hit a new record for the average price of attached properties at $504,193. At the end of June 2021, Denver Metro ended with 3,122 properties on the market. It has now almost doubled that amount over the year, with a total of 6,057 properties currently sitting on the market. … “The increase in supply will eventually impact pricing, days in the MLS and the relationship between buyers and sellers, which have negatively impacted buyers’ purchasing power,” commented Andrew Abrams, Chair of the DMAR Market Trends Committee and Metro Denver Realtor®. “The stock market, inflation and cryptocurrency have all taken a hit in the last few months. Housing will eventually be a victim to the economy as a whole, but just how much is yet to be seen. It is realistic to see days in the MLS, currently sitting at a historic low of four, increase in the coming months.”

emphasis added... And a table of June sales. Sales in these areas were down 23.4% YoY, Not Seasonally Adjusted (NSA). Contracts for sales in June were mostly signed in April and May, when mortgage rates were lower than in June.

...

Notes for all tables:

1) New additions to table in BOLD.

2) Northwest (Seattle) and Santa Clara (San Jose)

Trade Deficit decreased to $85.5 Billion in May

by Calculated Risk on 7/07/2022 08:46:00 AM

From the Department of Commerce reported:

The U.S. Census Bureau and the U.S. Bureau of Economic Analysis announced today that the goods and services deficit was $85.5 billion in May, down $1.1 billion from $86.7 billion in April, revised.

May exports were $255.9 billion, $3.0 billion more than April exports. May imports were $341.4 billion, $1.9 billion more than April imports.

emphasis added

Click on graph for larger image.

Click on graph for larger image.Both exports and imports increased in May.

Exports are up 22% year-over-year; imports are up 23% year-over-year.

Both imports and exports decreased sharply due to COVID-19, and have now bounced back (imports more than exports),

The second graph shows the U.S. trade deficit, with and without petroleum.

The blue line is the total deficit, and the black line is the petroleum deficit, and the red line is the trade deficit ex-petroleum products.

The blue line is the total deficit, and the black line is the petroleum deficit, and the red line is the trade deficit ex-petroleum products.Note that net, imports and exports of petroleum products are close to zero.

The trade deficit with China increased to $31.5 billion in May, from $26.1 billion a year ago.

The trade deficit was close to the consensus forecast, and the deficit for April was revised down.

Weekly Initial Unemployment Claims Increase to 235,000

by Calculated Risk on 7/07/2022 08:34:00 AM

The DOL reported:

In the week ending July 2, the advance figure for seasonally adjusted initial claims was 235,000, an increase of 4,000 from the previous week's unrevised level of 231,000. The 4-week moving average was 232,500, an increase of 750 from the previous week's unrevised average of 231,750.The following graph shows the 4-week moving average of weekly claims since 1971.

emphasis added

Click on graph for larger image.

Click on graph for larger image.The dashed line on the graph is the current 4-week average. The four-week average of weekly unemployment claims increased to 232,500.

The previous week was unrevised.

Weekly claims were higher than the consensus forecast.

Wednesday, July 06, 2022

Thursday: Unemployment Claims, Trade Deficit

by Calculated Risk on 7/06/2022 09:02:00 PM

Thursday:

• At 8:15 AM ET, The ADP Employment Report for June will NOT be released.

"ADP Research Institute (ADPRI) and the Stanford Digital Economy Lab (the "Lab") announced they will retool the ADP National Employment Report (NER) methodology to provide a more robust, high-frequency view of the labor market and trajectory of economic growth. In preparation for the changeover to the new report and methodology, ADPRI will pause issuing the current report and has targeted August 31, 2022 ..."• At 8:30 AM, The initial weekly unemployment claims report will be released. The consensus is for 225 thousand down from 231 thousand last week.

• Also at 8:30 AM, Trade Balance report for May from the Census Bureau. The consensus is the trade deficit to be $84.9 billion. The U.S. trade deficit was at $87.1 billion the previous month.

On COVID (focus on hospitalizations and deaths):

| COVID Metrics | ||||

|---|---|---|---|---|

| Now | Week Ago | Goal | ||

| Percent fully Vaccinated | 66.9% | --- | ≥70.0%1 | |

| Fully Vaccinated (millions) | 222.3 | --- | ≥2321 | |

| New Cases per Day3 | 106,178 | 108,391 | ≤5,0002 | |

| Hospitalized3🚩 | 28,101 | 26,543 | ≤3,0002 | |

| Deaths per Day3 | 267 | 345 | ≤502 | |

| 1 Minimum to achieve "herd immunity" (estimated between 70% and 85%). 2my goals to stop daily posts, 37-day average for Cases, Currently Hospitalized, and Deaths 🚩 Increasing 7-day average week-over-week for Cases, Hospitalized, and Deaths ✅ Goal met. | ||||

Click on graph for larger image.

Click on graph for larger image.This graph shows the daily (columns) and 7-day average (line) of deaths reported.

Average daily deaths bottomed in July 2021 at 214 per day.