RSS Feed

RSS Feed by Calculated Risk on 10/26/2022 10:09:00 AM

Wednesday, October 26, 2022

New Home Sales Decrease to 603,000 Annual Rate in September

The Census Bureau reports New Home Sales in September were at a seasonally adjusted annual rate (SAAR) of 603 thousand.

The previous three months were revised down, combined.

Sales of new single‐family houses in September 2022 were at a seasonally adjusted annual rate of 603,000, according to estimates released jointly today by the U.S. Census Bureau and the Department of Housing and Urban Development. This is 10.9 percent below the revised August rate of 677,000 and is 17.6 percent below the September 2021 estimate of 732,000.

emphasis added

Click on graph for larger image.

Click on graph for larger image.The first graph shows New Home Sales vs. recessions since 1963. The dashed line is the current sales rate.

New home sales are below pre-pandemic levels.

The second graph shows New Home Months of Supply.

The months of supply increased in September to 9.2 months from 8.1 months in August.

The months of supply increased in September to 9.2 months from 8.1 months in August. The all-time record high was 12.1 months of supply in January 2009. The all-time record low was 3.5 months, most recently in October 2020.

This is well above the top of the normal range (about 4 to 6 months of supply is normal).

"The seasonally‐adjusted estimate of new houses for sale at the end of September was 462,000. This represents a supply of 9.2 months at the current sales rate."

The last graph shows sales NSA (monthly sales, not seasonally adjusted annual rate).

The last graph shows sales NSA (monthly sales, not seasonally adjusted annual rate).In September 2022 (red column), 49 thousand new homes were sold (NSA). Last year, 58 thousand homes were sold in September.

The all-time high for September was 99 thousand in 2005, and the all-time low for September was 24 thousand in 2011.

This was slightly above expectations, however sales in the three previous months were revised down, combined. I'll have more later today.

MBA: Mortgage Applications Decrease in Latest Weekly Survey; Lowest Level Since 1997

by Calculated Risk on 10/26/2022 07:00:00 AM

From the MBA: Mortgage Applications Decrease in Latest MBA Weekly Survey

Mortgage applications decreased 1.7 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending October 21, 2022.

... The Refinance Index increased 0.1 percent from the previous week and was 86 percent lower than the same week one year ago. The seasonally adjusted Purchase Index decreased 2 percent from one week earlier. The unadjusted Purchase Index decreased 3 percent compared with the previous week and was 42 percent lower than the same week one year ago.

“Mortgage rates increased for the 10th consecutive week, with the 30-year fixed rate reaching 7.16 percent, the highest rate since 2001. The ongoing trend of rising mortgage rates continues to depress mortgage application activity, which remained at its slowest pace since 1997,” said Joel Kan, MBA’s Vice President and Deputy Chief Economist. “Refinance applications were ess entially unchanged, but purchase applications declined 2 percent to the slowest pace since 2015 – over 40 percent behind last year’s pace. Despite higher rates and lower overall application activity, there was a slight increase in FHA purchase applications, as FHA rates remained lower than conventional loan rates.”

Added Kan, “MBA’s forecast expects both economic and housing market weakness in 2023 to drive a 3 percent decline in purchase originations, while refinance volume is anticipated to decline by 24 percent.

...

The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($647,200 or less) increased to 7.16 percent from 6.94 percent, with points decreasing to 0.88 from 0.95 (including the origination fee) for 80 percent loan-to-value ratio (LTV) loans.

emphasis added

Click on graph for larger image.

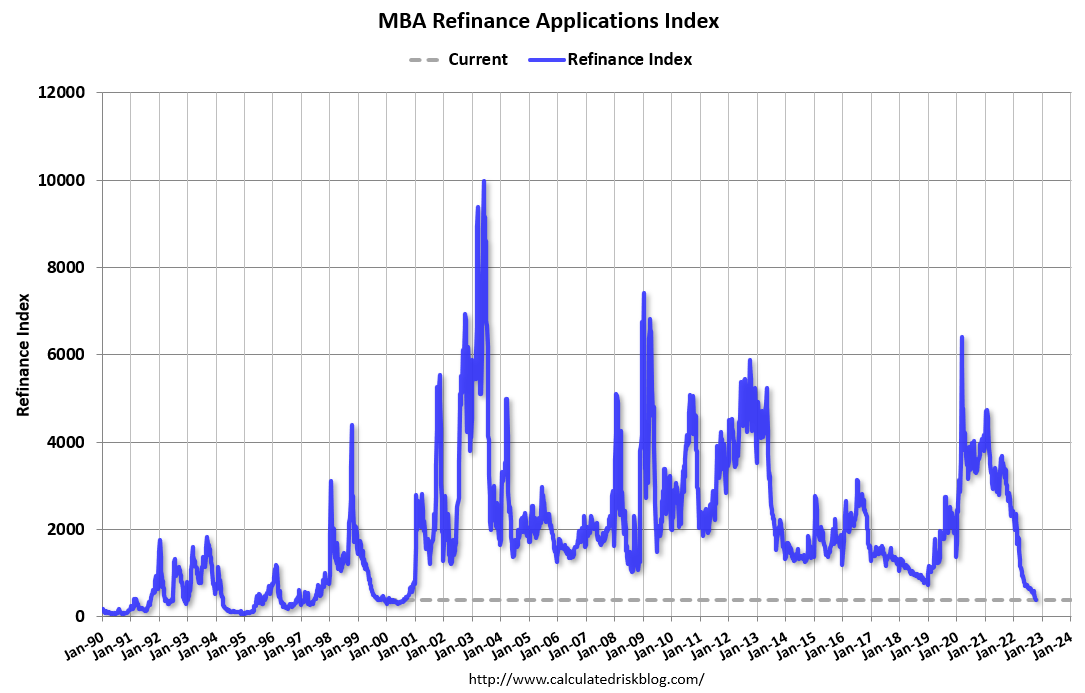

Click on graph for larger image.The first graph shows the refinance index since 1990.

With higher mortgage rates, the refinance index has declined sharply this year.

The refinance index is at the lowest level since the year 2000.

The second graph shows the MBA mortgage purchase index

According to the MBA, purchase activity is down 42% year-over-year unadjusted.

According to the MBA, purchase activity is down 42% year-over-year unadjusted.The purchase index is 12% below the pandemic low and at the lowest level since 2015.

Note: Red is a four-week average (blue is weekly).

Note: Red is a four-week average (blue is weekly).

Tuesday, October 25, 2022

Wednesday: New Home Sales

by Calculated Risk on 10/25/2022 09:01:00 PM

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

Wednesday:

• At 7:00 AM ET, The Mortgage Bankers Association (MBA) will release the results for the mortgage purchase applications index.

• At 10:00 AM, New Home Sales for September from the Census Bureau. The consensus is for 590 thousand SAAR, down from 685 thousand in August.

Freddie Mac: Mortgage Serious Delinquency Rate decreased in September

by Calculated Risk on 10/25/2022 04:42:00 PM

Freddie Mac reported that the Single-Family serious delinquency rate in September was 0.67%, down from 0.70% August. Freddie's rate is down year-over-year from 1.46% in September 2021.

Freddie's serious delinquency rate peaked in February 2010 at 4.20% following the housing bubble and peaked at 3.17% in August 2020 during the pandemic.

These are mortgage loans that are "three monthly payments or more past due or in foreclosure".

Click on graph for larger image

Click on graph for larger image

Mortgages in forbearance are being counted as delinquent in this monthly report but are not reported to the credit bureaus.

The serious delinquency rate was at 0.60% just prior to the pandemic - almost back to that level.

Note that multi-family delinquencies have been increasing and were at 0.13% in September.

Lawler: Update on the Household “Conundrum”

by Calculated Risk on 10/25/2022 02:25:00 PM

Today, in the Real Estate Newsletter: Lawler: Update on the Household “Conundrum”

Excerpt:

This is from housing economist Tom Lawler:There is much more in the article. You can subscribe at https://calculatedrisk.substack.com/

The pandemic wreaked havoc on some of the government surveys designed to measure the number of and characteristics of US households (though there were measurement issues before the pandemic), making it difficult for analysts how much of the extraordinary strength in the housing market during 2021 and early 2022 was related to “demographics” as opposed to behavioral and preference changes. (Here is the November 2021 piece on this issue). Nevertheless, it may still be useful to see what these reports are showing.

...

What is striking about the estimated household gain is that it is significantly above – in fact, about double -- what one would have projected if one had assumed that so-called “headship rates” in each age group (the number of householders in an age group divided by the total population of that age group) had remained the same over this period. Moreover, headship rate increases were concentrated in the 15–34-year-old categories.

If in fact over the 12-month period ending March of this year the number of households increased by almost two million, then household growth significantly outpaced housing production, as total housing completions plus manufactured housing shipments totaled only about 1.44 million.

In terms of household growth, there are several reasons to expect that household growth has slowed sharply since the beginning of this year ...

...

If in fact this dynamic shift between household growth and housing production is taking place, then it, combined with (1) the unprecedented increase in housing prices over a 2-year period from mid-2020 to mid-2022, and (2) the unprecedented surge in mortgage rates this year, would suggest that a non-trivial decline in home prices from the middle of this year to at least the middle of next year would be a logical “base case.” This shift, combined with (1) the unprecedented increase in rents from late 2020 to the middle of this year and (2) the significant increase in rental units coming to market over the next year, suggest not only that rent growth should soon decelerate sharply (in fact, some indicators suggest that it already has), but that an actual decline in rents next year would be a reasonable base case.

Comments on August Case-Shiller and FHFA House Prices

by Calculated Risk on 10/25/2022 10:02:00 AM

Today, in the Calculated Risk Real Estate Newsletter: Case-Shiller: National House Price Index "Continued to Decelerate" to 13.0% year-over-year increase in August

Excerpt:

Both the Case-Shiller House Price Index (HPI) and the Federal Housing Finance Agency (FHFA) HPI for August were released today. Here is a graph of the month-over-month (MoM) change in the Case-Shiller National Index Seasonally Adjusted (SA).

The Case-Shiller Home Price Indices for “August” is a 3-month average of June, July and August closing prices. June closing prices include some contracts signed in April, so there is a significant lag to this data.

The MoM decrease in Case-Shiller was at -0.86% seasonally adjusted. This was the second consecutive MoM decrease, and the largest MoM since February 2010. Since this includes closings in June and July, this suggests prices fell sharply for August closings.

On a seasonally adjusted basis, prices declined in all of the Case-Shiller cities on a month-to-month basis. The largest monthly declines seasonally adjusted were in San Francisco (-3.7%), Seattle (-2.9%), and San Diego (-2.5%). San Francisco has fallen 8.2% from the peak in May 2022.

...

The August Case-Shiller report is mostly for contracts signed in the April through July period when 30-year mortgage rates were in the low-to-mid 5% range. The September report will mostly be for contracts signed in the May through August period - when rates were also in the low-to-mid 5% range.

The impact from higher rates in September and October will not show up for several more months.

There is much more in the article. You can subscribe at https://calculatedrisk.substack.com/

Case-Shiller: National House Price Index "Continued to Decelerate" to 13.0% year-over-year increase in August

by Calculated Risk on 10/25/2022 09:12:00 AM

S&P/Case-Shiller released the monthly Home Price Indices for August ("August" is a 3-month average of June, July and August closing prices).

This release includes prices for 20 individual cities, two composite indices (for 10 cities and 20 cities) and the monthly National index.

From S&P: S&P Corelogic Case-Shiller Index Continued to Decelerate in August

The S&P CoreLogic Case-Shiller U.S. National Home Price NSA Index, covering all nine U.S. census divisions, reported a 13.0% annual gain in August, down from 15.6% in the previous month. The 10- City Composite annual increase came in at 12.1%, down from 14.9% in the previous month. The 20- City Composite posted a 13.1% year-over-year gain, down from 16.0% in the previous month.

Miami, Tampa, and Charlotte reported the highest year-over-year gains among the 20 cities in August. Miami led the way with a 28.6% year-over-year price increase, followed by Tampa in second with a 28.0% increase, and Charlotte in third with a 21.3% increase. All 20 cities reported lower price increases in the year ending August 2022 versus the year ending July 2022.

...

Before seasonal adjustment, the U.S. National Index posted a -1.1% month-over-month decrease in August, while the 10-City and 20-City Composites both posted decreases of -1.6%.

After seasonal adjustment, the U.S. National Index posted a month-over-month decrease of -0.9%, and the 10-City and 20-City Composites both posted decreases of -1.3%.

In August, all 20 cities reported declines before and after seasonal adjustments.

“The forceful deceleration in U.S. housing prices that we noted a month ago continued in our report for August 2022,” says Craig J. Lazzara, Managing Director at S&P DJI. “For example, the National Composite Index rose by 13.0% for the 12 months ended in August, down from its 15.6% year-over-year growth in July. The -2.6% difference between those two monthly rates of change is the largest deceleration in the history of the index (with July’s deceleration now ranking as the second largest). We see similar patterns in our 10-City Composite (up 12.1% in August vs. 14.9% in July) and our 20-City Composite (up 13.1% in August vs. 16.0% in July). Further, price gains decelerated in every one of our 20 cities. These data show clearly that the growth rate of housing prices peaked in the spring of 2022 and has been declining ever since.

“Month-over-month comparisons are consistent with these observations. All three composites declined in July, as did prices in every one of our 20 cities. On a month-over-month basis, the biggest declines occurred on the west coast, with San Francisco (-4.3%), Seattle (-3.9%), and San Diego (-2.8%) falling the most.

emphasis added

Click on graph for larger image.

Click on graph for larger image. The first graph shows the nominal seasonally adjusted Composite 10, Composite 20 and National indices (the Composite 20 was started in January 2000).

The Composite 10 index is down 1.3% in August (SA).

The Composite 20 index is down 1.3% (SA) in August.

The National index is 64% above the bubble peak (SA), and down 0.9% (SA) in August. The National index is up 121% from the post-bubble low set in February 2012 (SA).

The second graph shows the year-over-year change in all three indices.

The second graph shows the year-over-year change in all three indices.The Composite 10 SA is up 12.1% year-over-year. The Composite 20 SA is up 13.1% year-over-year.

The National index SA is up 13.0% year-over-year.

Price increases were lower than expectations. I'll have more later.

Monday, October 24, 2022

Tuesday: Case-Shiller and FHFA House Prices, Richmond Fed Mfg

by Calculated Risk on 10/24/2022 08:54:00 PM

From Matthew Graham at Mortgage News Daily: A Rare Winning Streak For Rates, But Don't Get Excited

From Matthew Graham at Mortgage News Daily: A Rare Winning Streak For Rates, But Don't Get Excited

Now here's a rare thing! Mortgage rates managed to move lower, on average, for the 2nd consecutive business day on Monday. That hasn't happened for roughly 3 weeks, and you'd need to go back another 3 weeks to see the previous example. ... [30 year fixed 7.29%]Tuesday:

emphasis added

• At 9:00 AM ET, S&P/Case-Shiller House Price Index for August. The consensus is for the Composite 20 index to be up 16.1% year-over-year.

• Also at 9:00 AM, FHFA House Price Index for August. This was originally a GSE only repeat sales, however there is also an expanded index.

• At 10:00 AM, Richmond Fed Survey of Manufacturing Activity for October.

October Vehicle Sales Forecast: "Signs of Life"

by Calculated Risk on 10/24/2022 01:54:00 PM

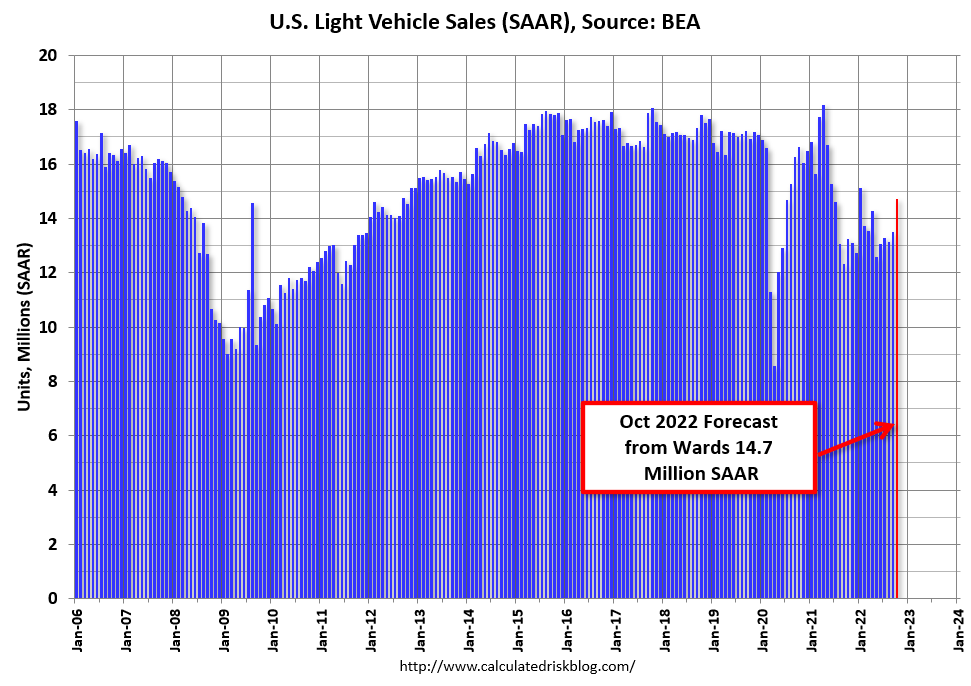

From WardsAuto: October U.S. Light-Vehicle Sales Show Signs of Life (pay content). Brief excerpt:

"The fourth-quarter SAAR is pegged at 14.2 million units, an improvement on Q2’s 13.3 million and Q3’s 13.4 million, but also meaning November-December results will weaken from October, with the primary reason being stiffer economic headwinds expected. Still, inventory will continue rising through the end of November, creating upside to the outlook"

Click on graph for larger image.

Click on graph for larger image.This graph shows actual sales from the BEA (Blue), and Wards forecast for October (Red).

The Wards forecast of 14.7 million SAAR, would be up 9% from last month, and up 11% from a year ago (sales weakened in the second half of 2021, due to supply chain issues).

Vehicle sales are usually a transmission mechanism for Federal Open Market Committee (FOMC) policy, far behind housing. However, this time, vehicle sales have been suppressed by supply chain issues, and sales will probably not be significantly impacted by higher interest rates.

Final Look at Local Housing Markets in September

by Calculated Risk on 10/24/2022 11:36:00 AM

Today, in the Calculated Risk Real Estate Newsletter: Final Look at Local Housing Markets in September

A brief excerpt:

The big story for September existing home sales was the sharp year-over-year (YoY) decline in sales. Another key story was that new listings were down YoY in September as many potential sellers are locked into their current home (low mortgage rate).There is much more in the article. You can subscribe at https://calculatedrisk.substack.com/

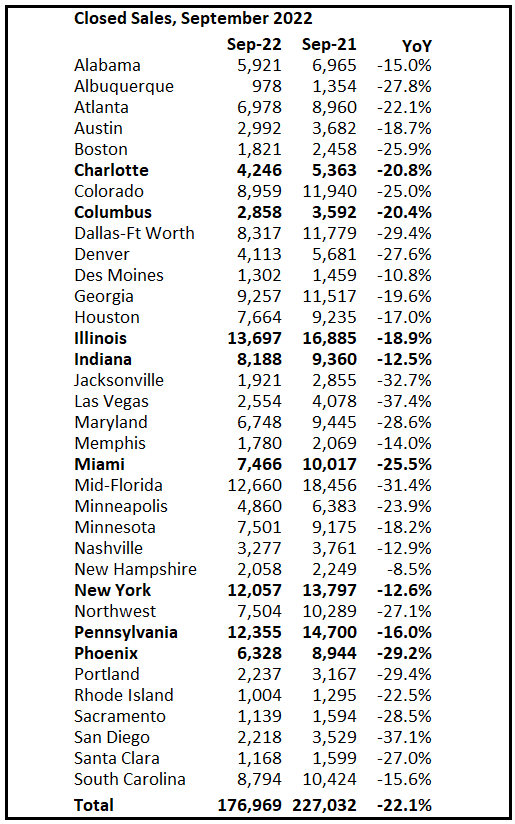

This is the final look at local markets in September. I’m tracking about 35 local housing markets in the US. Some of the 35 markets are states, and some are metropolitan areas. I update these tables throughout the month as additional data is released.

Important: Closed sales in September were mostly for contracts signed in July and August when 30-year mortgage rates averaged about 5.3%. Rates increased to around 6% in September and that will impact closed sales in October and November. In October 30-year mortgage rates have jumped to over 7%, negatively impacting closed sales in November and December.

...

And a table of September sales. In September, sales were down 22.1% YoY Not Seasonally Adjusted (NSA) for these markets. The NAR reported sales were down 21.6% NSA YoY.

Sales in some of the hottest markets are down around 30% YoY (all of California was down 30%), whereas in other markets, sales are only down in the teens YoY.

More local data coming in November for activity in October! We should expect even larger YoY declines in the next few months due to the recent increase in mortgage rates.

Four High Frequency Indicators for the Economy

by Calculated Risk on 10/24/2022 09:23:00 AM

These indicators are mostly for travel and entertainment. It is interesting to watch these sectors recover as the pandemic subsides.

The TSA is providing daily travel numbers.

This data is as of October 23rd.

Click on graph for larger image.

Click on graph for larger image.This data shows the 7-day average of daily total traveler throughput from the TSA for 2019 (Light Blue), 2020 (Black), 2021 (Blue) and 2022 (Red).

The dashed line is the percent of 2019 for the seven-day average.

The 7-day average is down 3.9% from the same day in 2019 (96.1% of 2019). (Dashed line)

Air travel - as a percent of 2019 - seems to be picking up a little, but overall, still below 2019 levels.

----- Movie Tickets: Box Office Mojo -----

This data shows domestic box office for each week and the median for the years 2016 through 2019 (dashed light blue).

This data shows domestic box office for each week and the median for the years 2016 through 2019 (dashed light blue).

This data shows domestic box office for each week and the median for the years 2016 through 2019 (dashed light blue).

This data shows domestic box office for each week and the median for the years 2016 through 2019 (dashed light blue). Black is 2020, Blue is 2021 and Red is 2022.

The data is from BoxOfficeMojo through October 20th.

Note that the data is usually noisy week-to-week and depends on when blockbusters are released.

Movie ticket sales were at $96 million last week, down about 42% from the median for the week.

Note that the data is usually noisy week-to-week and depends on when blockbusters are released.

Movie ticket sales were at $96 million last week, down about 42% from the median for the week.

This graph shows the seasonal pattern for the hotel occupancy rate using the four-week average.

This graph shows the seasonal pattern for the hotel occupancy rate using the four-week average. The red line is for 2022, black is 2020, blue is the median, and dashed light blue is for 2021. Dashed purple is 2019 (STR is comparing to a strong year for hotels).

This data is through Oct 15th. The occupancy rate was down 2.7% compared to the same week in 2019.

The 4-week average of the occupancy rate is above the median rate for the previous 20 years (Blue).

Notes: Y-axis doesn't start at zero to better show the seasonal change.

Notes: Y-axis doesn't start at zero to better show the seasonal change.

This graph, based on weekly data from the U.S. Energy Information Administration (EIA), shows gasoline supplied compared to the same week of 2019.

Blue is for 2020. Purple is for 2021, and Red is for 2022.

As of October 14th, gasoline supplied was down 7.2% compared to the same week in 2019.

Recently gasoline supplied has been running below 2019 and 2021 levels - and sometimes below 2020.

Housing October 24th Weekly Update: Inventory Increased, New High for 2022

by Calculated Risk on 10/24/2022 08:15:00 AM

Active inventory increased again, hitting another new peak for the year. Here are the same week inventory changes for the last four years (usually inventory is declining at this time of year):

2022: +5.7K (still increasing!)

2021: -0.8K

2020: -4.7K

2019: -7.0K

Inventory bottomed seasonally at the beginning of March 2022 and is now up 137% since then. Altos reports inventory is up 1.0% week-over-week.

Click on graph for larger image.

Click on graph for larger image.

This inventory graph is courtesy of Altos Research.

Click on graph for larger image.

Click on graph for larger image.This inventory graph is courtesy of Altos Research.

As of October 21st, inventory was at 572 thousand (7-day average), compared to 566 thousand the prior week.

Compared to the same week in 2021, inventory is up 35.3% from 423 thousand, and compared to the same week in 2020 inventory is up 4.0% from 559 thousand. Compared to 3 years ago, inventory is down 38.4% from 929 thousand.

Here are the inventory milestones I’ve been watching for with the Altos data:

1. The seasonal bottom (happened on March 4, 2022, for Altos) ✅

2. Inventory up year-over-year (happened on May 20, 2022, for Altos) ✅

3. Inventory up compared to 2020 (happened on October 7, 2022, for Altos) ✅

4. Inventory up compared to 2019 (currently down 38.4%).

1. The seasonal bottom (happened on March 4, 2022, for Altos) ✅

2. Inventory up year-over-year (happened on May 20, 2022, for Altos) ✅

3. Inventory up compared to 2020 (happened on October 7, 2022, for Altos) ✅

4. Inventory up compared to 2019 (currently down 38.4%).

Here is a graph of the inventory change vs 2021 (milestone 2 above), 2020 (milestone 3) and 2019 (milestone 4).

The blue line is the year-over-year data, the red line is compared to two years ago, and dashed purple is compared to 2019.

A key will be if inventory continues to increase in the Fall.

Mike Simonsen discusses this data regularly on Youtube.

Sunday, October 23, 2022

Sunday Night Futures

by Calculated Risk on 10/23/2022 06:40:00 PM

Weekend:

• Schedule for Week of October 23, 2022

Monday:

• At 8:30 AM ET, Chicago Fed National Activity Index for September. This is a composite index of other data.

From CNBC: Pre-Market Data and Bloomberg futures S&P 500 are up 38 and DOW futures are up 244 (fair value).

Oil prices were down over the last week with WTI futures at $85.05 per barrel and Brent at $93.50 per barrel. A year ago, WTI was at $85, and Brent was at $85 - so WTI oil prices are unchanged year-over-year.

Here is a graph from Gasbuddy.com for nationwide gasoline prices. Nationally prices are at $3.76 per gallon. A year ago, prices were at $3.35 per gallon, so gasoline prices are up $0.41 per gallon year-over-year.

Retail: October Seasonal Hiring vs. Holiday Retail Sales

by Calculated Risk on 10/23/2022 10:38:00 AM

Every year I track seasonal retail hiring for hints about holiday retail sales. At the bottom of this post is a graph showing the correlation between October seasonal hiring and holiday retail sales.

Here is a graph of retail hiring for previous years based on the BLS employment report:

Click on graph for larger image.

Click on graph for larger image.

This graph shows the historical net retail jobs added for October, November and December by year.

Retailers hired about 700 thousand seasonal workers last year (using BLS data, Not Seasonally Adjusted), and 224 thousand seasonal workers last October.

Note that in the early '90s, retailers started hiring seasonal workers earlier - and the trend towards hiring earlier has continued.

The following scatter graph is for the years 2005 through 2021 and compares October retail hiring with the real increase (inflation adjusted) for retail sales (Q4 over previous Q4).

In general October hiring is a pretty good indicator of seasonal sales. R-square is 0.82 for this small sample. Note: This uses retail sales in Q4, and excludes autos, gasoline and restaurants.

In general October hiring is a pretty good indicator of seasonal sales. R-square is 0.82 for this small sample. Note: This uses retail sales in Q4, and excludes autos, gasoline and restaurants.

NOTE: The dot in the upper right - with real Retail sales up almost 10% YoY is for 2020 - when retail sales soared due to the pandemic spending on goods (service spending was soft).

When the October employment report is released on November 4th, I'll be looking at seasonal retail hiring for hints on what the retailers actually expect for the holiday season.

Saturday, October 22, 2022

Real Estate Newsletter Articles this Week: Record Number of Housing Units Under Construction

by Calculated Risk on 10/22/2022 02:11:00 PM

At the Calculated Risk Real Estate Newsletter this week:

• NAR: Existing-Home Sales Decreased to 4.71 million SAAR in September

• September Housing Starts: Record Number of Housing Units Under Construction

• Monthly Mortgage Payments Up Record Year-over-year

• 3rd Look at Local Housing Markets in September, California Sales off 30% YoY

• Lawler: Early Read on Existing Home Sales in September; CAR Predicts Home Prices to Decline 8.8% in 2023!

• Some "Good News" for Homebuilders

This is usually published 4 to 6 times a week and provides more in-depth analysis of the housing market.

You can subscribe at https://calculatedrisk.substack.com/

Most content is available for free (and no Ads), but please subscribe!

Schedule for Week of October 23, 2022

by Calculated Risk on 10/22/2022 08:11:00 AM

The key reports this week are the advance estimate of Q3 GDP and September New Home sales.

Other key indicators include Personal Income and Outlays for September and Case-Shiller house prices for August.

For manufacturing, the Richmond and Kansas City Fed manufacturing surveys will be released this week.

8:30 AM ET: Chicago Fed National Activity Index for September. This is a composite index of other data.

9:00 AM ET: S&P/Case-Shiller House Price Index for August. The consensus is for the Composite 20 index to be up 16.1% year-over-year.

9:00 AM ET: S&P/Case-Shiller House Price Index for August. The consensus is for the Composite 20 index to be up 16.1% year-over-year.This graph shows the year-over-year change in the nominal seasonally adjusted National Index, Composite 10 and Composite 20 indexes through the most recent report (the Composite 20 was started in January 2000).

9:00 AM: FHFA House Price Index for August. This was originally a GSE only repeat sales, however there is also an expanded index.

10:00 AM: Richmond Fed Survey of Manufacturing Activity for October.

7:00 AM ET: The Mortgage Bankers Association (MBA) will release the results for the mortgage purchase applications index.

10:00 AM: New Home Sales for September from the Census Bureau.

10:00 AM: New Home Sales for September from the Census Bureau. This graph shows New Home Sales since 1963. The dashed line is the sales rate for last month.

The consensus is for 590 thousand SAAR, down from 685 thousand in August.

8:30 AM: The initial weekly unemployment claims report will be released. The consensus is for an increase to 225 thousand from 214 thousand last week.

8:30 AM: Gross Domestic Product, 3rd quarter 2022 (advance estimate). The consensus is that real GDP increased 2.4% annualized in Q3, up from -0.6% in Q2.

8:30 AM ET: Durable Goods Orders for September from the Census Bureau. The consensus is for a 0.5% increase in durable goods orders.

11:00 AM: Kansas City Fed Survey of Manufacturing Activity for October.

8:30 AM ET: Personal Income and Outlays for September. The consensus is for a 0.3% increase in personal income, and for a 0.4% increase in personal spending. And for the Core PCE price index to increase 0.5%. PCE prices are expected to be up 6.2% YoY, and core PCE prices up 5.2% YoY.

10:00 AM: Pending Home Sales Index for September. The consensus is 5.0% decrease in the index.

10:00 AM: University of Michigan's Consumer sentiment index (Final for October). The consensus is for a reading of 59.8.

Friday, October 21, 2022

COVID Oct 21, 2022: Update on Cases, Hospitalizations and Deaths

by Calculated Risk on 10/21/2022 09:11:00 PM

30-year mortgage rates at a 20-year high.

30-year mortgage rates at a 20-year high.

NOTE: COVID stats are updated on Fridays.

On COVID (focus on hospitalizations and deaths). Data has switched to weekly.

Weekly deaths bottomed in July 2021 at 1,666.

| COVID Metrics | ||||

|---|---|---|---|---|

| Now | Week Ago | Goal | ||

| New Cases per Week2 | 260,808 | 265,175 | ≤35,0001 | |

| Hospitalized2🚩 | 21,062 | 19,625 | ≤3,0001 | |

| Deaths per Week2 | 2,566 | 2,582 | ≤3501 | |

| 1my goals to stop weekly posts, 2Weekly for Cases, Currently Hospitalized, and Deaths 🚩 Increasing number weekly for Cases, Hospitalized, and Deaths ✅ Goal met. | ||||

Click on graph for larger image.

Click on graph for larger image.This graph shows the weekly (columns) number of deaths reported.

Total Housing Completions Will Increase About 6% in 2022

by Calculated Risk on 10/21/2022 02:56:00 PM

Even as housing starts slow, completions will increase in 2022 compared to 2021.

This graph shows total housing completions and placements since 1968 with an estimate for 2022. Note that the net additional to the housing stock is less because of demolitions and destruction of older housing units.

Click on graph for larger image.

Click on graph for larger image.My current estimate is total completions (single family, multi-family, manufactured homes) will increase about 6% in 2022 to over 1.5 million. This will be close to the same level of completions as in 2007.

This is an update to an August article in the Calculated Risk Real Estate Newsletter: Update: Housing Completions will Increase Sharply in Late 2022 and Early 2023

Q3 GDP Tracking: In 2% Range

by Calculated Risk on 10/21/2022 10:06:00 AM

The advance estimate for Q3 GDP will be released next Thursday and the consensus is that real GDP increased 2.4%, on a seasonally adjusted annual rate basis.

From BofA:

The smaller-than-expected decline in existing home sales lifted our 3Q US GDP tracker from 2.0% q/q saar to 2.1%. [October 20th estimate]From Goldman:

emphasis added

Following this morning’s data, we left our Q3 GDP tracking estimate unchanged at +2.4% (qoq ar). [October 20th estimate]And from the Altanta Fed: GDPNow

The GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the third quarter of 2022 is 2.9 percent on October 19, up from 2.8 percent on October 14. After recent releases from the Federal Reserve Board of Governors and the US Census Bureau, the nowcast of third-quarter real gross private domestic investment growth increased from -3.6 percent to -3.3 percent. [October 19th estimate]

Black Knight: Mortgage Delinquency Rate decreased in September

by Calculated Risk on 10/21/2022 08:11:00 AM

From Black Knight: Black Knight: September Prepayments at More Than 20-Year Low on Spiking Interest Rates; Foreclosure Starts Fall 9% from August, Remain 53% Below Pre-Pandemic Levels

• Prepayment activity dropped -14.9% to a single-month mortality (SMM) rate of 0.57% in September – below the recent record of 0.59% set in January 2019 – to the lowest level since November 2000According to Black Knight's First Look report, the percent of loans delinquent decreased 0.2% in September compared to August and decreased 29% year-over-year.

• The national delinquency rate inched down -0.2% from August to 2.78%, just 3 basis points above the record low set in May 2022, with the number of past-due mortgages holding relatively steady across the board

• The number of borrowers a single payment past due rose by 1%, while 90-day delinquencies fell -1.5 % in September and are now only 24% above the pre-pandemic serious delinquency rate

• Foreclosure starts fell 9% from August to 18,400 – 53% below pre-pandemic levels – with starts initiated on 3% of serious delinquencies, still less than half the rate of the years leading up to the pandemic

• Active foreclosure inventory held steady in the month at volumes that have remained subdued in early 2022 after the record lows of 2021 due to widespread moratoriums and forbearance protections

• Prepays (SMM) edged up 1.5% for the month, due to calendar-related effects, but are still down by 69% year-over-year as rising rates continue to put downward pressure on both purchase and refinance lending

emphasis added

Black Knight reported the U.S. mortgage delinquency rate (loans 30 or more days past due, but not in foreclosure) was 2.78% in September, down from 2.79% in August.

The percent of loans in the foreclosure process was unchanged in September at 0.35%, from 0.35% in August.

The number of delinquent properties, but not in foreclosure, is down 577,000 properties year-over-year, and the number of properties in the foreclosure process is up 50,000 properties year-over-year.

| Black Knight: Percent Loans Delinquent and in Foreclosure Process | ||||

|---|---|---|---|---|

| Sept 2022 | Aug 2022 | Sept 2021 | Sept 2020 | |

| Delinquent | 2.78% | 2.79% | 3.91% | 6.66% |

| In Foreclosure | 0.35% | 0.35% | 0.26% | 0.34% |

| Number of properties: | ||||

| Number of properties that are delinquent, but not in foreclosure: | 1,491,000 | 1,489,000 | 2,068,000 | 3,542,000 |

| Number of properties in foreclosure pre-sale inventory: | 185,000 | 185,000 | 135,000 | 181,000 |

| Total Properties | 1,677,000 | 1,674,000 | 2,203,000 | 3,722,000 |