RSS Feed

RSS Feed by Calculated Risk on 11/11/2022 02:09:00 PM

Friday, November 11, 2022

Early Q4 GDP Tracking

It is early in Q4 ... we will have more estimates next week.

From BofA:

[Forecast 1.0% in Q4] Overall, the data since our last weekly publication pushed down our 3Q GDP tracking estimate from 3.1% q/q saar (seasonally adjusted annual rate) to 3.0% q/q saar. Looking ahead to next week, there are a number of data releases that could affect 3Q tracking, including retail sales on Wednesday, which will also kick-off our 4Q tracking. [Nov 11th estimate]And from the Altanta Fed: GDPNow

emphasis added

The GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the fourth quarter of 2022 is 4.0 percent on November 9, up from 3.6 percent on November 3. [Nov 9th estimate]

Current State of the Housing Market; Overview for mid-November

by Calculated Risk on 11/11/2022 09:46:00 AM

Today, in the Calculated Risk Real Estate Newsletter: Current State of the Housing Market; Overview for mid-November

A brief excerpt:

Over the last month …There is much more in the article. You can subscribe at https://calculatedrisk.substack.com/

1. New listings have declined further year-over-year.

2.Mortgage rates had increased further but declined this week.

3. House prices are declining month-over-month (MoM) as measured by the repeat sales indexes.

...

The next graph shows the month-over-month (MoM) decrease in the seasonally adjusted Case-Shiller index. The MoM decrease in Case-Shiller was at -0.86% seasonally adjusted. This was the second consecutive MoM decrease, and the largest MoM since February 2010. Since this includes closings in June and July, this suggests prices fell sharply for August closings.

...

Next Friday, the NAR will release existing home sales for October. This report will likely show another sharp year-over-year decline in sales for October.

Hotels: Occupancy Rate Down 9.2% Compared to Same Week in 2019

by Calculated Risk on 11/11/2022 08:29:00 AM

As expected due to the Halloween calendar shift, U.S. hotel performance came in lower than the previous week and showed weakened comparisons to 2019, according to STR‘s latest data through Nov. 5.The following graph shows the seasonal pattern for the hotel occupancy rate using the four-week average.

Oct. 30 through Nov. 5, 2022 (percentage change from comparable week in 2019*):

• Occupancy: 62.4% (-9.2%)

• Average daily rate (ADR): $147.48 (+11.4%)

• Revenue per available room (RevPAR): $91.99 (+1.1%)

While none of the Top 25 Markets showed an occupancy increase over 2019, Tampa came closest to its pre-pandemic comparable (-1.0% to 72.4%). ...

*Due to the pandemic impact, STR is measuring recovery against comparable time periods from 2019.

emphasis added

Click on graph for larger image.

Click on graph for larger image.The red line is for 2022, black is 2020, blue is the median, and dashed light blue is for 2021. Dashed purple is 2019 (STR is comparing to a strong year for hotels).

The 4-week average of the occupancy rate is above the median rate for the previous 20 years (Blue).

Note: Y-axis doesn't start at zero to better show the seasonal change.

The 4-week average of the occupancy rate will decline into the Winter.

Thursday, November 10, 2022

Realtor.com Reports Weekly Active Inventory Up 42% Year-over-year; New Listings Down 20%

by Calculated Risk on 11/10/2022 04:27:00 PM

Realtor.com has monthly and weekly data on the existing home market. Here is their weekly report released today from Chief Economist Danielle Hale: Weekly Housing Trends View — Data Week Ending Nov 5, 2022. Note: They have data on list prices, new listings and more, but this focus is on inventory.

• Active inventory continued to grow, increasing 42% above one year ago. Inventory accelerated by a more modest amount this week, but it was still the fourth consecutive week of roughly 2+% inventory gains after a fair amount of stability since July. Inventory growth even in the face of fewer newly listed homes indicates how many buyers have retreated from the housing market rather than navigate higher costs stemming from higher purchase prices and higher mortgage rates.

...

• New listings–a measure of sellers putting homes up for sale–were again down, dropping 20% from one year ago. This marks the eighteenth week of year over year declines in homeowners listing their home for sale, a sign that homeowners are well aware of the market’s reset. This data suggests that many potential sellers may be joining buyers in “wait-and-see” mode.

Here is a graph of the year-over-year change in inventory according to realtor.com.

Here is a graph of the year-over-year change in inventory according to realtor.com. Note the rapid increase in the YoY change earlier this year, from down 30% at the beginning of the year, to up 29% YoY at the beginning of July.

Then the Realtor.com data was stuck at up around 26% to 30% YoY for 14 weeks in a row. This was due to the slowdown in new listings, even as sales had fallen sharply.

Now YoY inventory is increasing again with even higher mortgage rates, suggesting sales are off more than new listings.

Housing and Inflation

by Calculated Risk on 11/10/2022 02:02:00 PM

Today, in the Calculated Risk Real Estate Newsletter: Housing and Inflation

A brief excerpt:

A few key points:There is much more in the article. You can subscribe at https://calculatedrisk.substack.com/

• The Fed has been raising rates to slow inflation. Since housing is a key transmission mechanism for Fed policy, the housing market has slowed dramatically as the Fed raised rates (and mortgage rates increased).

• The CPI report this morning contained some good news on inflation.

• The BLS reported “The index for shelter contributed over half of the monthly all items increase”.

• The BLS measure for shelter is seriously lagged and is likely behind the curve on the sharp slowdown in rents.

...

Both CPI and core CPI were below expectations, and the year-over-year change is declining. Bond yields fell sharply this morning, and the 30-year mortgage rate dropped significantly to 6.67% from 7.25% yesterday (average top tier scenarios with zero points).

...

My current view is inflation will ease quicker than the Fed currently expects.

MBA: "Mortgage Delinquencies Decrease to New Survey Low in the Third Quarter of 2022"

by Calculated Risk on 11/10/2022 11:33:00 AM

From the MBA: Mortgage Delinquencies Decrease to New Survey Low in the Third Quarter of 2022

The delinquency rate for mortgage loans on one-to-four-unit residential properties decreased to a seasonally adjusted rate of 3.45 percent of all loans outstanding at the end of the third quarter of 2022, according to the Mortgage Bankers Association’s (MBA) National Delinquency Survey.

For the purposes of the survey, MBA asks servicers to report loans in forbearance as delinquent if the payment was not made based on the original terms of the mortgage. The delinquency rate was down 19 basis points from the second quarter of 2022 and down 143 basis points from one year ago.

“For the second quarter in a row, the mortgage delinquency rate fell to its lowest level since MBA’s survey began in 1979 – declining to 3.45 percent. Foreclosure starts and loans in the process of foreclosure also dropped in the third quarter to levels further below their historical averages,” said Marina Walsh, CMB, MBA’s Vice President of Industry Analysis. “The relatively small number of seriously delinquent homeowners are working with their mortgage servicers to find foreclosure alternatives, including loan workouts that allow for home retention.”

emphasis added

Click on graph for larger image.

Click on graph for larger image.This graph shows the percent of loans delinquent by days past due. Overall delinquencies decreased in Q3 to a record low.

From the MBA:

Compared to second-quarter 2022, the seasonally adjusted mortgage delinquency rate decreased for all loans outstanding to 3.45 percent, the lowest level in the history of the survey dating back to 1979. By stage, the 30-day delinquency rate remained unchanged at 1.66 percent, the 60-day delinquency rate increased 4 basis points to 0.53 percent, and the 90-day delinquency bucket decreased 22 basis points to 1.27 percent.This sharp increase in 2020 in the 90-day bucket was due to loans in forbearance (included as delinquent, but not reported to the credit bureaus).

...

The delinquency rate includes loans that are at least one payment past due but does not include loans in the process of foreclosure. For much of the last two years, foreclosure moratoria were in place, which kept these numbers artificially low. ... The percentage of loans in the foreclosure process at the end of the third quarter of 2022 was 0.56 percent, down 3 basis points from the second quarter of 2022, and 10 basis points higher than one year ago.

The percent of loans in the foreclosure process increased year-over-year in Q3 with the end of the foreclosure moratoriums.

Cleveland Fed: Median CPI increased 0.5% and Trimmed-mean CPI increased 0.4% in October

by Calculated Risk on 11/10/2022 11:18:00 AM

The Cleveland Fed released the median CPI and the trimmed-mean CPI this morning:

According to the Federal Reserve Bank of Cleveland, the median Consumer Price Index rose 0.5% in October. The 16% trimmed-mean Consumer Price Index increased 0.4% in October. "The median CPI and 16% trimmed-mean CPI are measures of core inflation calculated by the Federal Reserve Bank of Cleveland based on data released in the Bureau of Labor Statistics’ (BLS) monthly CPI report".

Click on graph for larger image.

Click on graph for larger image.This graph shows the year-over-year change for these four key measures of inflation.

On a year-over-year basis, the median CPI rose 7.0%, the trimmed-mean CPI rose 7.0%, and the CPI less food and energy rose 6.3%. Core PCE is for September and increased 5.1% year-over-year.

Note: The Cleveland Fed released the median CPI details here: "Fuel oil and other fuels" increased at a 232% annualized rate in October.

Note that Owners' Equivalent Rent and Rent of Primary Residence account for almost 1/3 of median CPI, and these measures were up between 6.0% annualized in the Midwest and 8.5% in the South with an average of close to 8% annualized. The year-over-year increase for OER was less in October than in September. This data is lagged, and actually rent growth has slowed sharply in recent months.

Weekly Initial Unemployment Claims increase to 225,000

by Calculated Risk on 11/10/2022 08:38:00 AM

The DOL reported:

In the week ending November 5, the advance figure for seasonally adjusted initial claims was 225,000, an increase of 7,000 from the previous week's revised level. The previous week's level was revised up by 1,000 from 217,000 to 218,000. The 4-week moving average was 218,750, a decrease of 250 from the previous week's revised average. The previous week's average was revised up by 250 from 218,750 to 219,000.The following graph shows the 4-week moving average of weekly claims since 1971.

emphasis added

Click on graph for larger image.

Click on graph for larger image.The dashed line on the graph is the current 4-week average. The four-week average of weekly unemployment claims decreased to 218,750.

The previous week was revised up.

Weekly claims were above the consensus forecast.

BLS: CPI increased 0.4% in October; Core CPI increased 0.3%

by Calculated Risk on 11/10/2022 08:32:00 AM

The Consumer Price Index for All Urban Consumers (CPI-U) rose 0.4 percent in October on a seasonally adjusted basis, the same increase as in September, the U.S. Bureau of Labor Statistics reported today. Over the last 12 months, the all items index increased 7.7 percent before seasonal adjustment.Both CPI and core CPI were below expectations. I'll post a graph later today after the Cleveland Fed releases the median and trimmed-mean CPI.

The index for shelter contributed over half of the monthly all items increase, with the indexes for gasoline and food also increasing. The energy index increased 1.8 percent over the month as the gasoline index and the electricity index rose, but the natural gas index decreased. The food index increased 0.6 percent over the month with the food at home index rising 0.4 percent.

The index for all items less food and energy rose 0.3 percent in October, after rising 0.6 percent in September. The indexes for shelter, motor vehicle insurance, recreation, new vehicles, and personal care were among those that increased over the month. Indexes which declined in October included the used cars and trucks, medical care, apparel, and airline fares indexes.

The all items index increased 7.7 percent for the 12 months ending October, this was the smallest 12-month increase since the period ending January 2022. The all items less food and energy index rose 6.3 percent over the last 12 months. The energy index increased 17.6 percent for the 12 months ending October, and the food index increased 10.9 percent over the last year; all of these increases were smaller than for the period ending September.

emphasis added

Wednesday, November 09, 2022

Thursday: CPI, Unemployment Claims

by Calculated Risk on 11/09/2022 09:01:00 PM

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

Thursday:

• At 8:30 AM ET, The Consumer Price Index for October from the BLS. The consensus is for a 0.7% increase in CPI, and a 0.5% increase in core CPI. The consensus is for CPI to be up 8.0% year-over-year and core CPI to be up 6.6% YoY.

• Also at 8:30 AM: The initial weekly unemployment claims report will be released. The consensus is for 220 thousand initial claims, up from 217 thousand last week.

Second Home Market: South Lake Tahoe in October

by Calculated Risk on 11/09/2022 01:25:00 PM

With the pandemic, there was a surge in 2nd home buying.

I'm looking at data for some second home markets - and I'm tracking those markets to see if there is an impact from lending changes, rising mortgage rates or the easing of the pandemic.

This graph is for South Lake Tahoe since 2004 through October 2022, and shows inventory (blue), and the year-over-year (YoY) change in the median price (12-month average).

Note: The median price is distorted by the mix, but this is the available data.

Following the housing bubble, prices declined for several years in South Lake Tahoe, with the median price falling about 50% from the bubble peak.

Currently inventory is still very low, but still up almost 4-fold from the record low set in February 2022, and up 37% year-over-year. Prices are up 2.6% YoY (and the YoY change has been trending down).

It is possible that the YoY change will turn negative soon - even with inventory at historically fairly low levels.

New Home Cancellations increased Sharply in Q3

by Calculated Risk on 11/09/2022 10:29:00 AM

Today, in the Calculated Risk Real Estate Newsletter: New Home Cancellations increased Sharply in Q3

A brief excerpt:

First, a few quotes from some homebuilders:There is much more in the article. You can subscribe at https://calculatedrisk.substack.com/"During most of the year, demand for our homes was strong. Beginning in June and continuing through today, we have seen a moderation in housing demand caused by significant increases in mortgage interest rates and general economic uncertainty.” [Donald R. Horton, Chairman of the Board, said] …The Company’s cancellation rate (cancelled sales orders divided by gross sales orders) for the fourth quarter of fiscal 2022 was 32% compared to 19% in the prior year quarter. D.R. Horton

“In response to the significant shift in market conditions in 2022, we have slowed the pace of our housing starts, have increased sales incentives, and are taking additional pricing actions in many of our communities.” Pulte Group

New Orders decreased 15%, while the average sales price of New Orders increased 3% in the third quarter of 2022 compared to the third quarter of 2021. New Orders were negatively impacted in each of our reportable segments by the significant increase in mortgage interest rates during the quarter, which resulted in a decline in affordability and in turn, led to lower absorption rates and to an increase in the cancellation rate quarter over quarter. NVR

emphasis addedHere is a table of selected public builders and the currently reported cancellation rate (I’m still gathering data).

Disclaimer: the cancellation rates are from SEC filings only, and while deemed to be reliable is not guaranteed.

In general, cancellation rates doubled or tripled in the most recent quarter compared to 2021.

MBA: Mortgage Applications Decrease in Latest Weekly Survey

by Calculated Risk on 11/09/2022 07:00:00 AM

From the MBA: Mortgage Applications Decrease in Latest MBA Weekly Survey

— Mortgage applications decreased 0.1 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending November 4, 2022.

... The Refinance Index decreased 4 percent from the previous week and was 87 percent lower than the same week one year ago. The seasonally adjusted Purchase Index increased 1 percent from one week earlier. The unadjusted Purchase Index decreased 1 percent compared with the previous week and was 41 percent lower than the same week one year ago.

“Mortgage rates edged higher last week following news that the Federal Reserve will continue raising short-term rates to combat high inflation. The 30-year fixed rate remained above 7 percent for the third consecutive week, with increases for most loan types,” said Joel Kan, MBA’s Vice President and Deputy Chief Economist. “Purchase applications increased for the first time after six weeks of declines but remained close to 2015 lows, as homebuyers remained sidelined by higher rates and ongoing economic uncertainty. Refinances continued to fall, with the index hitting its lowest level since August 2000.”

...

The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($647,200 or less) increased to 7.14 percent from 7.06 percent, with points increasing to 0.77 from 0.73 (including the origination fee) for 80 percent loan-to-value ratio (LTV) loans.

emphasis added

Click on graph for larger image.

Click on graph for larger image.The first graph shows the refinance index since 1990.

With higher mortgage rates, the refinance index has declined sharply this year.

The refinance index is at the lowest level since the year 2000.

The second graph shows the MBA mortgage purchase index

According to the MBA, purchase activity is down 41% year-over-year unadjusted.

According to the MBA, purchase activity is down 41% year-over-year unadjusted.The purchase index is 11% below the pandemic low and near the lowest level since 2015.

Note: Red is a four-week average (blue is weekly).

Note: Red is a four-week average (blue is weekly).

Tuesday, November 08, 2022

CPI Preview and Owners' equivalent rent

by Calculated Risk on 11/08/2022 03:31:00 PM

On Thursday, the BLS will release inflation data for October. The consensus is for a 0.7% increase in CPI, and a 0.5% increase in core CPI. The consensus is for CPI to be up 8.0% year-over-year and core CPI to be up 6.6% YoY.

Here is a preview from Goldman Sachs economists Manuel Abecasis and Spencer Hill:

We expect a below-consensus 0.44% increase in core CPI in October (vs. 0.5% consensus), which would lower the year-on-year rate to 6.46% (vs. 6.5% consensus). We expect moderate increases in both food and energy prices to raise headline CPI by 0.49% (vs. 0.6% consensus), which would lower the year-on-year rate to 7.8% (vs. 7.9% consensus).Recently we've seen used car prices down over 10% YoY, and framing lumber prices down 33% YoY. One of the keys will be rent, especially Owners' equivalent rent (OER). In Goldman's note, they echoed Fed Chair Powell's comment about rents have "some significant rate increases coming":

[W]e expect shelter inflation to run hot (rent +0.78%, OER + 0.75%)—even though alternative web-based measures of new tenant rent growth have slowed—because continuing tenant rent levels still have a long way to catch up to new tenant market rates.However, Rental housing economist Jay Parsons argues rental data will "cool faster than the Fed expects:

emphasis added

Click on graph for larger image.

Click on graph for larger image.Here's the data to show real-life rent inflation will cool faster than the Fed suggested last week-- and not just for asking rents:

We’ve plunged back to long-term average in “loss to lease” – meaning the runway for renewal lease rents will significantly narrow going forward...

“Loss to lease” is the gap between today’s market asking rents and the average in-place (embedded) rent (aka “contract rent,” which is what the CPI attempts to measure). As a general rule of thumb: The larger the loss to lease, the larger the renewal increase...

Here is a dissertation from economist Adam Ozimek showing a significant lag in CPI measured rents: Sticky Rents and the CPI for Owner-Occupied Housing Rent inflation will be a key for the Fed.

CHRISTOPHER RUGABER. Thank you, Chris Rugaber at Associated Press. Just to go back to housing for a minute, you mentioned the impact that rate increases have had on housing, home sales are down 25 percent in the past year, and so forth, but none of this is really showing up in, as you know, in the government's inflation measures. And as we go forward, private real-time data is clearly showing these hits to housing. Are you going to need to put a greater weigh on that in order to ascertain things like whether there's over tightening going on or will you still focus as much on the more lagging government indicators?

CHAIR POWELL. So this is an interesting subject. So I start by saying I guess that the measure that's in the CPI and the PCE, it captures rents for all tenants, not just the new, not just new leases. And that makes sense actually because that, for that reason, that conceptually that is, that's sort of the right target for monetary policy. And the same thing is true for owners' equivalent rent which comes off of, it's a re-weighting of tenant rents. The private measures are of course good at picking up the, at the margin, the new leases and they tell you a couple things; one thing is, once you, I think right now, if you look at the pattern of that series of the new leases, it's very pro-cyclical, so rents went up much more than the CPI and PCE rents did. And now they're coming down faster. So but what you're, the implication is that there are still as people, as non-new leases rollover and expire, right? You still, they're still in the pipeline, there's still some significant rate increases coming. Okay? But at some point, once you get through that, the new leases are going to tell you, what they're telling you is there will come a point at which rent inflation will start to come down. But that point is well out from where we are now. So we're well-aware of that of course and we look at it. And we've, but I would say that in terms of the right way to think about inflation really is to look at the measure that we do look at, but considering that we also know that at some point you'll see rents coming down.

emphasis added

Leading Index for Commercial Real Estate Increases in October

by Calculated Risk on 11/08/2022 01:16:00 PM

From Dodge Data Analytics: Dodge Momentum Index Continues to Climb in October

he Dodge Momentum Index (DMI), issued by Dodge Construction Network, improved 9.6% (2000=100) in October to 199.7 from the revised September reading of 182.2. During the month, the DMI continued its steady ascent, with the commercial component rising 13%, and the institutional component ticking up 2.9%.

Commercial planning was bolstered by a solid increase in office and hotel projects. The institutional component was varied, experiencing growth in recreational and education projects, countered by a decline in the number of healthcare and public planning projects. On a year-over-year basis, the DMI was 28% higher than in October 2021, the commercial component was up 29%, and institutional planning was 25% higher.

...

“The sustained upward trajectory in the Momentum Index shows optimism from owners and developers that projects will continue to move forward, even with rising concerns of an economic recession,” said Sarah Martin, senior economist for Dodge Construction Network. “Specific nonresidential segments, such as data centers and life science laboratories, have thrived in 2022 and continue to support strength in planning activity. As we move into next year, however, labor and supply shortages, high material costs and high interest rates will likely temper planning activity back to a more moderate pace.”

emphasis added

Click on graph for larger image.

Click on graph for larger image.This graph shows the Dodge Momentum Index since 2002. The index was at 199.7 in October, up from 182.2 in September.

According to Dodge, this index leads "construction spending for nonresidential buildings by a full year". This index suggests a solid pickup in commercial real estate construction into 2023.

Update: Framing Lumber Prices Close to Pre-Pandemic Levels

by Calculated Risk on 11/08/2022 11:19:00 AM

Here is another monthly update on framing lumber prices.

This graph shows CME random length framing futures through November 8th.

Lumber was at $447 per 1000 board feet this morning.

This is down from the peak of $1,733, and down 33% from $663 a year ago.

Prices are close to the pre-pandemic levels of around $400.

Click on graph for larger image.

Click on graph for larger image.

It is unlikely we will see a runup in prices as happened at the end of last year due to the housing slowdown.

Prices are close to the pre-pandemic levels of around $400.

Click on graph for larger image.

Click on graph for larger image.There is somewhat of a seasonal demand for lumber, and lumber prices usually peak in April or May, although prices peaked much earlier this year.

It is unlikely we will see a runup in prices as happened at the end of last year due to the housing slowdown.

1st Look at Local Housing Markets in October

by Calculated Risk on 11/08/2022 08:53:00 AM

Today, in the Calculated Risk Real Estate Newsletter: 1st Look at Local Housing Markets in October

A brief excerpt:

This is the first look at local markets in October. I’m tracking about 35 local housing markets in the US. Some of the 35 markets are states, and some are metropolitan areas. I’ll update these tables throughout the month as additional data is released.There is much more in the article. You can subscribe at https://calculatedrisk.substack.com/

Closed sales in October were mostly for contracts signed in August and September. Mortgage rates moved higher in September, and that impacted closed sales in October.

The further sharp increase in mortgage rates in October - with the 30-year mortgage over 7% - will impact closed sales in November and December.

...

In October, sales were down 38.0%. In September, these same markets were down 28.5% YoY Not Seasonally Adjusted (NSA).

Note that in October 2022, there were the same number of selling days as in October 2021, so the SA decline will be similar to the NSA decline. And this suggests another significant step down in sales!

Many more local markets to come!

Monday, November 07, 2022

Tuesday: Small Business Survey

by Calculated Risk on 11/07/2022 09:00:00 PM

From Matthew Graham at Mortgage News Daily: New Issuance Keeping Pressure on Bonds Ahead of CPI

From Matthew Graham at Mortgage News Daily: New Issuance Keeping Pressure on Bonds Ahead of CPI

CPI-watching is all the more interesting these days due to the extreme prevalence of one particular month-over-month reading. Core monthly inflation came in at 0.6% no fewer than 8 times since the start of the pandemic, and 5 of those have been in 2022. No other level has been even half as prevalent. In annualized term, 0.6% represents a 7.2% core inflation rate--well over the current 6.6% level. The 2 most recent reports both came in at 0.6%, making it even more of a line in the sand--one that can help us identify a turning point. ... [30 year fixed 7.25%]Tuesday:

emphasis added

• At 6:00 AM ET, NFIB Small Business Optimism Index for October.

Fed Survey: Banks reported Tighter Standards, Weaker Demand for Most Loan Types; Stronger Demand for HELOCs

by Calculated Risk on 11/07/2022 05:06:00 PM

From the Federal Reserve: The October 2022 Senior Loan Officer Opinion Survey on Bank Lending Practices

The October 2022 Senior Loan Officer Opinion Survey on Bank Lending Practices (SLOOS) addressed changes in the standards and terms on, and demand for, bank loans to businesses and households over the past three months, which generally correspond to the third quarter of 2022.

Regarding loans to businesses, survey respondents reported, on balance, tighter standards and weaker demand for commercial and industrial (C&I) loans to firms of all sizes over the third quarter. Meanwhile, banks reported tighter standards and weaker demand for all commercial real estate (CRE) loan categories.

For loans to households, lending standards tightened or remained basically unchanged across all categories of residential real estate (RRE) loans and demand weakened for all such loans. In addition, banks reported tighter standards and stronger demand for home equity lines of credit (HELOCs). Standards tightened for credit card loans and other consumer loans while standards for auto loans remained unchanged. Meanwhile, demand strengthened for credit card loans, was unchanged for other consumer loans, and weakened for auto loans.

emphasis added

Click on graph for larger image.

Click on graph for larger image.This graph on Residential Real Estate demand is from the Senior Loan Officer Survey Charts.

This shows that demand has declined sharply.

The left graph is 1990 to 2014. The right graph is 2015 to Q3 2022.

Housing November 7th Weekly Update: Inventory Decreased Slightly Week-over-week

by Calculated Risk on 11/07/2022 12:09:00 PM

Active inventory decreased slightly. Here are the same week inventory changes for the last four years (usually inventory is declining sharply at this time of year):

2022: -2.2K (smaller than usual decrease in inventory)

2021: -13.0K

2020: -13.4K

2019: -20.7K

Inventory bottomed seasonally at the beginning of March 2022 and is now up 138% since then. Altos reports inventory is down 0.4% week-over-week.

Click on graph for larger image.

Click on graph for larger image.

This inventory graph is courtesy of Altos Research.

Click on graph for larger image.

Click on graph for larger image.This inventory graph is courtesy of Altos Research.

As of November 4th, inventory was at 575 thousand (7-day average), compared to 577 thousand the prior week.

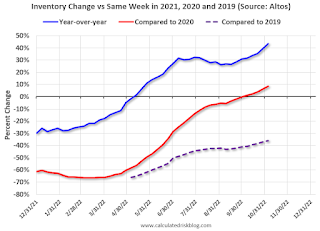

Compared to the same week in 2021, inventory is up 43.5% from 401 thousand, and compared to the same week in 2020 inventory is up 8.5% from 530 thousand. Compared to 3 years ago (2019), inventory is down 36.0% from 898 thousand.

Here are the inventory milestones I’ve been watching for with the Altos data:

1. The seasonal bottom (happened on March 4, 2022, for Altos) ✅

2. Inventory up year-over-year (happened on May 20, 2022, for Altos) ✅

3. Inventory up compared to 2020 (happened on October 7, 2022, for Altos) ✅

4. Inventory up compared to 2019 (currently down 36.0%).

1. The seasonal bottom (happened on March 4, 2022, for Altos) ✅

2. Inventory up year-over-year (happened on May 20, 2022, for Altos) ✅

3. Inventory up compared to 2020 (happened on October 7, 2022, for Altos) ✅

4. Inventory up compared to 2019 (currently down 36.0%).

Here is a graph of the inventory change vs 2021 (milestone 2 above), 2020 (milestone 3) and 2019 (milestone 4).

The blue line is the year-over-year data, the red line is compared to two years ago, and dashed purple is compared to 2019.

A key will be if inventory declines slowly during the winter months.

Mike Simonsen discusses this data regularly on Youtube.