RSS Feed

RSS Feed by Calculated Risk on 11/21/2022 08:41:00 PM

Monday, November 21, 2022

Tuesday: Richmond Fed Mfg

From Matthew Graham at Mortgage News Daily: Mortgage Rates Little-Changed to Start Holiday-Shortened Week

From Matthew Graham at Mortgage News Daily: Mortgage Rates Little-Changed to Start Holiday-Shortened Week

Mortgage rates made their biggest recent move (and their biggest single day move ever) 2 Thursday's ago after a key report showed inflation was lower than expected in October. There has been some jockeying for position among various mortgage lenders since then, but remarkably little change to the average 30yr fixed rate which is once again in the mid 6% range. ... [30 year fixed 6.64%]Tuesday:

emphasis added

• At 8:30 AM ET, Richmond Fed Survey of Manufacturing Activity for November.

MBA Survey: "Share of Mortgage Loans in Forbearance Increases Slightly to 0.70% in October"

by Calculated Risk on 11/21/2022 04:12:00 PM

Note: This is as of October 31st.

From the MBA: Share of Mortgage Loans in Forbearance Increases Slightly to 0.70% in October

The Mortgage Bankers Association’s (MBA) monthly Loan Monitoring Survey revealed that the total number of loans now in forbearance increased by 1 basis point from 0.69% of servicers’ portfolio volume in the prior month to 0.70% as of October 31, 2022. According to MBA’s estimate, 350,000 homeowners are in forbearance plans.

The share of Fannie Mae and Freddie Mac loans in forbearance increased 1 basis point to 0.31%. Ginnie Mae loans in forbearance increased 8 basis points to 1.41%, and the forbearance share for portfolio loans and private-label securities (PLS) declined 11 basis points to 1.03%.

“The overall share of loans in forbearance increased slightly in October, but it was a mixed bag by investor type. The forbearance rate for Ginnie Mae, Fannie Mae, and Freddie Mac loans increased, and there was a decline in portfolio and PLS loans in forbearance,” said Marina Walsh, CMB, MBA’s Vice President of Industry Analysis. “Several factors were behind the first monthly increase in forbearances in 29 months, including the effects of Hurricane Ian in the Southeast, the diminishing number of loans bought out of Ginnie Mae pools and placed in portfolio, and the fact that new forbearance requests have closely matched forbearance exits for the past three months.”

...

Added Walsh, “The overall share of loans that were current last month decreased 15 basis points to 95.70%, with 44 states reporting declines (not delinquent or in foreclosure). Florida, which was hit the hardest by Hurricane Ian, experienced a 49-basis-point drop in the share of loans that were current – the biggest decline of all states.”

emphasis added

Click on graph for larger image.

Click on graph for larger image.This graph shows the percent of portfolio in forbearance by investor type over time.

The share of forbearance plans had been decreasing, although there was a slight increase in October. At the end of October, there were about 350,000 homeowners in forbearance plans.

Final Look at Local Housing Markets in October

by Calculated Risk on 11/21/2022 12:43:00 PM

Today, in the Calculated Risk Real Estate Newsletter: Final Look at Local Housing Markets in October

A brief excerpt:

The big story for October existing home sales was the sharp year-over-year (YoY) decline in sales. Another key story was that new listings were down further YoY in October as many potential sellers are locked into their current home (low mortgage rate). And active inventory increased sharply YoY.There is much more in the article. You can subscribe at https://calculatedrisk.substack.com/

This is the final look at local markets in October. I’m tracking about 35 local housing markets in the US. Some of the 35 markets are states, and some are metropolitan areas. I update these tables throughout each month as additional data is released.

Important: Closed sales in October were mostly for contracts signed in August and September. Rates increased to around 6% in September and that impacted closed sales in October. In October 30-year mortgage rates jumped to over 7%, and that will negatively impact closed sales in November and December.

...

And a table of October sales. In October, sales were down 28.6% YoY Not Seasonally Adjusted (NSA) for these markets. ... The NAR reported sales were down 29.5% NSA YoY in October.

Sales in some of the hottest markets are down around 40% YoY (all of California was down 37%), whereas in other markets, sales are only down in around 20% YoY.

...

More local data coming in December for activity in November! We should expect an even larger YoY sales decline in November and December due to the increase in mortgage rates in September and October.

Housing November 21st Weekly Update: Inventory Decreased Slightly Week-over-week

by Calculated Risk on 11/21/2022 08:57:00 AM

Active inventory decreased slightly. Here are the same week inventory changes for the last four years (usually inventory declines seasonally through the Winter):

2022: -3.0K (smaller than usual decrease in inventory)

2021: -8.9K

2020: -10.5K

2019: -14.7K

Altos reports inventory is down 0.5% week-over-week and down 1.5% from the peak on October 28th.

Click on graph for larger image.

Click on graph for larger image.

This inventory graph is courtesy of Altos Research.

Click on graph for larger image.

Click on graph for larger image.This inventory graph is courtesy of Altos Research.

As of November 18th, inventory was at 569 thousand (7-day average), compared to 572 thousand the prior week.

Compared to the same week in 2021, inventory is up 47.7% from 385 thousand, and compared to the same week in 2020 inventory is up 10.6% from 514 thousand. However, compared to 3 years ago (2019), inventory is down 35.2% from 877 thousand.

Here are the inventory milestones I’ve been watching for with the Altos data:

1. The seasonal bottom (happened on March 4, 2022, for Altos) ✅

2. Inventory up year-over-year (happened on May 20, 2022, for Altos) ✅

3. Inventory up compared to 2020 (happened on October 7, 2022, for Altos) ✅

4. Inventory up compared to 2019 (currently down 35.2%).

1. The seasonal bottom (happened on March 4, 2022, for Altos) ✅

2. Inventory up year-over-year (happened on May 20, 2022, for Altos) ✅

3. Inventory up compared to 2020 (happened on October 7, 2022, for Altos) ✅

4. Inventory up compared to 2019 (currently down 35.2%).

Here is a graph of the inventory change vs 2021 (milestone 2 above), 2020 (milestone 3) and 2019 (milestone 4).

The blue line is the year-over-year data, the red line is compared to two years ago, and dashed purple is compared to 2019.

A key will be if inventory declines slower than usual during the winter months.

Mike Simonsen discusses this data regularly on Youtube.

Four High Frequency Indicators for the Economy

by Calculated Risk on 11/21/2022 08:32:00 AM

These indicators are mostly for travel and entertainment. It was interesting to watch these sectors recover as the pandemic impact subsided.

The TSA is providing daily travel numbers.

This data is as of November 20th.

Click on graph for larger image.

Click on graph for larger image.This data shows the 7-day average of daily total traveler throughput from the TSA for 2019 (Light Blue), 2020 (Black), 2021 (Blue) and 2022 (Red).

The dashed line is the percent of 2019 for the seven-day average.

The 7-day average is 2.6% below the same week in 2019 (97.4% of 2019). (Dashed line)

Air travel - as a percent of 2019 - has picked up recently.

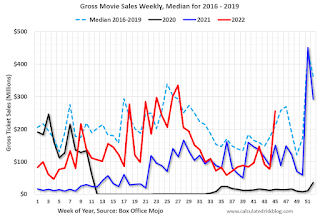

----- Movie Tickets: Box Office Mojo -----

This data shows domestic box office for each week and the median for the years 2016 through 2019 (dashed light blue).

This data shows domestic box office for each week and the median for the years 2016 through 2019 (dashed light blue).

This data shows domestic box office for each week and the median for the years 2016 through 2019 (dashed light blue).

This data shows domestic box office for each week and the median for the years 2016 through 2019 (dashed light blue). Black is 2020, Blue is 2021 and Red is 2022.

The data is from BoxOfficeMojo through November 17th.

Note that the data is usually noisy week-to-week and depends on when blockbusters are released.

Movie ticket sales were at $255 million last week - almost entirely due to Black Panther: Wakanda Forever - up about 21% from the median for the week.

Note that the data is usually noisy week-to-week and depends on when blockbusters are released.

Movie ticket sales were at $255 million last week - almost entirely due to Black Panther: Wakanda Forever - up about 21% from the median for the week.

This graph shows the seasonal pattern for the hotel occupancy rate using the four-week average.

This graph shows the seasonal pattern for the hotel occupancy rate using the four-week average. The red line is for 2022, black is 2020, blue is the median, and dashed light blue is for 2021. Dashed purple is 2019 (STR is comparing to a strong year for hotels).

This data is through Nov 12th. The occupancy rate was up 0.9% compared to the same week in 2019.

The 4-week average of the occupancy rate is above the median rate for the previous 20 years (Blue) and close to 2019 levels.

Notes: Y-axis doesn't start at zero to better show the seasonal change.

Notes: Y-axis doesn't start at zero to better show the seasonal change.

This graph, based on weekly data from the U.S. Energy Information Administration (EIA), shows gasoline supplied compared to the same week of 2019.

Blue is for 2020. Purple is for 2021, and Red is for 2022.

As of November 11th, gasoline supplied was down 6.2% compared to the same week in 2019.

Recently gasoline supplied has been running below 2019 and 2021 levels - and sometimes below 2020.

Sunday, November 20, 2022

Sunday Night Futures

by Calculated Risk on 11/20/2022 07:02:00 PM

Weekend:

• Schedule for Week of November 20, 2022

Monday:

• AT 8:30 AM ET, Chicago Fed National Activity Index for October. This is a composite index of other data.

From CNBC: Pre-Market Data and Bloomberg futures S&P 500 are down 5 and DOW futures are down 40 (fair value).

Oil prices were down over the last week with WTI futures at $80.08 per barrel and Brent at $87.62 per barrel. A year ago, WTI was at $77, and Brent was at $81 - so WTI oil prices are up 4% year-over-year.

Here is a graph from Gasbuddy.com for nationwide gasoline prices. Nationally prices are at $3.67 per gallon. A year ago, prices were at $3.41 per gallon, so gasoline prices are up $0.26 per gallon year-over-year.

Hotels: Occupancy Rate Up 0.9% Compared to Same Week in 2019

by Calculated Risk on 11/20/2022 08:15:00 AM

U.S. hotel performance came in higher than the previous week and showed improved comparisons to 2019, according to STR‘s latest data through Nov. 12.The following graph shows the seasonal pattern for the hotel occupancy rate using the four-week average.

Nov. 6-12, 2022 (percentage change from comparable week in 2019*):

• Occupancy: 64.6% (+0.9%)

• Average daily rate (ADR): US$148.43 (+17.1%)

• Revenue per available room (RevPAR): US$95.89 (+18.2%)

*Due to the pandemic impact, STR is measuring recovery against comparable time periods from 2019.

emphasis added

Click on graph for larger image.The red line is for 2022, black is 2020, blue is the median, and dashed light blue is for 2021. Dashed purple is 2019 (STR is comparing to a strong year for hotels).

The 4-week average of the occupancy rate is above the median rate for the previous 20 years (Blue) and close to 2019 levels.

Note: Y-axis doesn't start at zero to better show the seasonal change.

The 4-week average of the occupancy rate will decline into the Winter.

Saturday, November 19, 2022

Real Estate Newsletter Articles this Week: Record Number of Housing Units Under Construction

by Calculated Risk on 11/19/2022 02:11:00 PM

At the Calculated Risk Real Estate Newsletter this week:

• October Housing Starts: Record Number of Housing Units Under Construction

• NAR: Existing-Home Sales Decreased to 4.43 million SAAR in October

• 3rd Look at Local Housing Markets in October; California Sales off 37% YoY, Prices Fall; Early Read on October Sales

• Lawler: Are US Rents Falling?

• 2nd Look at Local Housing Markets in October

This is usually published 4 to 6 times a week and provides more in-depth analysis of the housing market.

You can subscribe at https://calculatedrisk.substack.com/

Most content is available for free (and no Ads), but please subscribe!

Schedule for Week of November 20, 2022

by Calculated Risk on 11/19/2022 08:11:00 AM

The key report this week is October New Home sales.

For manufacturing, the Richmond Fed manufacturing survey will be released this week.

8:30 AM ET: Chicago Fed National Activity Index for October. This is a composite index of other data.

10:00 AM: Richmond Fed Survey of Manufacturing Activity for November.

7:00 AM ET: The Mortgage Bankers Association (MBA) will release the results for the mortgage purchase applications index.

8:30 AM: The initial weekly unemployment claims report will be released. The consensus is for 225 thousand initial claims, up from 222 thousand last week.

8:30 AM: Durable Goods Orders for October from the Census Bureau. The consensus is for a 0.4% increase in durable goods orders.

10:00 AM: New Home Sales for October from the Census Bureau.

10:00 AM: New Home Sales for October from the Census Bureau. This graph shows New Home Sales since 1963. The dashed line is the sales rate for last month.

The consensus is for 570 thousand SAAR, down from 603 thousand in September.

2:00 PM: FOMC Minutes, Meeting of November 1-2, 2022

All US markets will be closed in observance of the Thanksgiving Day Holiday.

The NYSE and the NASDAQ will close early at 1:00 PM ET.

Friday, November 18, 2022

COVID Nov 18, 2022: Update on Cases, Hospitalizations and Deaths

by Calculated Risk on 11/18/2022 08:27:00 PM

NOTE: COVID stats are updated on Fridays.

On COVID (focus on hospitalizations and deaths). Data has switched to weekly.

Weekly deaths bottomed in July 2021 at 1,666.

| COVID Metrics | ||||

|---|---|---|---|---|

| Now | Week Ago | Goal | ||

| New Cases per Week2 | 280,711 | 289,884 | ≤35,0001 | |

| Hospitalized2 | 21,275 | 21,722 | ≤3,0001 | |

| Deaths per Week2 | 2,222 | 2,347 | ≤3501 | |

| 1my goals to stop weekly posts, 2Weekly for Cases, Currently Hospitalized, and Deaths 🚩 Increasing number weekly for Cases, Hospitalized, and Deaths ✅ Goal met. | ||||

Click on graph for larger image.

Click on graph for larger image.This graph shows the weekly (columns) number of deaths reported.

Early Q4 GDP Tracking

by Calculated Risk on 11/18/2022 02:47:00 PM

From BofA:

Existing home sales actually fell less than we expected, implying slightly stronger brokers’ commissions in 4Q. As a result, our tracking estimate for residential investment in 4Q edged up. That said, after rounding, our 4Q GDP tracking estimate was unchanged at 1.3% q/q saar. [Nov 18th estimate]From Goldman:

emphasis added

We lowered our Q4 GDP tracking estimate by 0.1pp to +0.9% (qoq ar). [Nov 18th estimate]And from the Altanta Fed: GDPNow

The GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the fourth quarter of 2022 is 4.2 percent on November 17, down from 4.4 percent on November 16. [Nov 17th estimate]

More Analysis on October Existing Home Sales

by Calculated Risk on 11/18/2022 11:41:00 AM

Today, in the CalculatedRisk Real Estate Newsletter: NAR: Existing-Home Sales Decreased to 4.43 million SAAR in October

Excerpt:

On prices, the NAR reported:There is much more in the article. You can subscribe at https://calculatedrisk.substack.com/ (Most content is available for free, so please subscribe).The median existing-home price for all housing types in October was $379,100, a gain of 6.6% from October 2021 ($355,700), as prices rose in all regions. This marks 128 consecutive months of year-over-year increases, the longest-running streak on record.Median prices are distorted by the mix (repeat sales indexes like Case-Shiller and FHFA are probably better for measuring prices).

The YoY change in the median price peaked at 25.2% in May 2021 and has now slowed to 6.6%. The YoY increase in October was the lowest since June 2020. Note that the median price usually starts falling seasonally in July, so the 1.1% decline in October in the median price was partially seasonal, however the 8.4% decline over the last four months has been much larger than the usual seasonal decline.

It is likely the median price will be down year-over-year in a few months.

NAR: Existing-Home Sales Decreased to 4.43 million SAAR in October

by Calculated Risk on 11/18/2022 10:12:00 AM

From the NAR: Existing-Home Sales Slumped 5.9% in October

Existing-home sales retreated for the ninth straight month in October, according to the National Association of REALTORS®. All four major U.S. regions registered month-over-month and year-over-year declines.

Total existing-home sales - completed transactions that include single-family homes, townhomes, condominiums and co-ops – decreased 5.9% from September to a seasonally adjusted annual rate of 4.43 million in October. Year-over-year, sales dropped by 28.4% (down from 6.19 million in October 2021).

...

Total housing inventory registered at the end of October was 1.22 million units, which was down 0.8% from both September and one year ago (1.23 million). Unsold inventory sits at a 3.3-month supply at the current sales pace, up from 3.1 months in September and 2.4 months in October 2021.

emphasis added

Click on graph for larger image.

Click on graph for larger image.This graph shows existing home sales, on a Seasonally Adjusted Annual Rate (SAAR) basis since 1993.

Sales in October (4.43million SAAR) were down 5.9% from the previous month and were 28.4% below the October 2021 sales rate.

The second graph shows nationwide inventory for existing homes.

According to the NAR, inventory decreased to 1.22 million in October from 1.23 million in September.

According to the NAR, inventory decreased to 1.22 million in October from 1.23 million in September.Headline inventory is not seasonally adjusted, and inventory usually decreases to the seasonal lows in December and January, and peaks in mid-to-late summer.

The last graph shows the year-over-year (YoY) change in reported existing home inventory and months-of-supply. Since inventory is not seasonally adjusted, it really helps to look at the YoY change. Note: Months-of-supply is based on the seasonally adjusted sales and not seasonally adjusted inventory.

Inventory was essentially unchanged year-over-year (blue) in October compared to October 2021.

Inventory was essentially unchanged year-over-year (blue) in October compared to October 2021.

Months of supply (red) increased to 3.3 months in October from 3.1 months in September.

This was slightly above the consensus forecast. I'll have more later.

The last graph shows the year-over-year (YoY) change in reported existing home inventory and months-of-supply. Since inventory is not seasonally adjusted, it really helps to look at the YoY change. Note: Months-of-supply is based on the seasonally adjusted sales and not seasonally adjusted inventory.

Inventory was essentially unchanged year-over-year (blue) in October compared to October 2021.

Inventory was essentially unchanged year-over-year (blue) in October compared to October 2021. Months of supply (red) increased to 3.3 months in October from 3.1 months in September.

This was slightly above the consensus forecast. I'll have more later.

LA Port Traffic Down Sharply in October

by Calculated Risk on 11/18/2022 08:45:00 AM

Notes: The expansion to the Panama Canal was completed in 2016 (As I noted a few years ago), and some of the traffic that used the ports of Los Angeles and Long Beach is probably going through the canal. This might be impacting TEUs on the West Coast.

Container traffic gives us an idea about the volume of goods being exported and imported - and usually some hints about the trade report since LA area ports handle about 40% of the nation's container port traffic.

The following graphs are for inbound and outbound traffic at the ports of Los Angeles and Long Beach in TEUs (TEUs: 20-foot equivalent units or 20-foot-long cargo container).

To remove the strong seasonal component for inbound traffic, the first graph shows the rolling 12-month average.

Click on graph for larger image.

Click on graph for larger image.

On a rolling 12-month basis, inbound traffic decreased 2.2% in October compared to the rolling 12 months ending in September. Outbound traffic decreased 0.4% compared to the rolling 12 months ending the previous month.

The 2nd graph is the monthly data (with a strong seasonal pattern for imports).

Usually imports peak in the July to October period as retailers import goods for the Christmas holiday, and then decline sharply and bottom in February or March depending on the timing of the Chinese New Year.

Usually imports peak in the July to October period as retailers import goods for the Christmas holiday, and then decline sharply and bottom in February or March depending on the timing of the Chinese New Year.

Imports were down 26% YoY in October, and exports were down 5% YoY.

It is possible that exports have bottomed after declining for several years (even prior to the pandemic).

Thursday, November 17, 2022

Friday: Existing Home Sales

by Calculated Risk on 11/17/2022 08:35:00 PM

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

Friday:

• At 10:00 AM ET, Existing Home Sales for October from the National Association of Realtors (NAR). The consensus is for 4.39 million SAAR, down from 4.71 million in September.

• Also at 10:00 AM, State Employment and Unemployment (Monthly) for October 2022

Realtor.com Reports Weekly Active Inventory Up 45% Year-over-year; New Listings Down 18%

by Calculated Risk on 11/17/2022 02:10:00 PM

Realtor.com has monthly and weekly data on the existing home market. Here is their weekly report released today from Chief Economist Danielle Hale: Weekly Housing Trends View — Data Week Ending Nov 12, 2022. Note: They have data on list prices, new listings and more, but this focus is on inventory.

• Active inventory continued to grow, increasing 45% above one year ago. Inventory accelerated again, notching a fifth straight week of gains roughly at or above 2% after a fair amount of stability between July and September. Fewer newly listed homes would normally cause a decline in inventory, but buyers have retreated from the housing market as higher and more uncertain costs make it difficult to ascertain purchasing power and set a budget.

...

• New listings–a measure of sellers putting homes up for sale–were again down, dropping 18% from one year ago. This marks the nineteenth week of year over year declines in homeowners listing their home for sale, a tangible reflection of the ongoing decline in seller confidence. Because potential sellers have pulled back so significantly, prices are decelerating in a more modest fashion than might otherwise be the case.

Here is a graph of the year-over-year change in inventory according to realtor.com.

Here is a graph of the year-over-year change in inventory according to realtor.com. Note the rapid increase in the YoY change earlier this year, from down 30% at the beginning of the year, to up 29% YoY at the beginning of July.

Then the Realtor.com data was stuck at up around 26% to 30% YoY for 14 weeks in a row. This was due to the slowdown in new listings, even as sales had fallen sharply.

Now YoY inventory is increasing again with even higher mortgage rates, suggesting sales are off more than new listings.

October Housing Starts: Record Number of Housing Units Under Construction

by Calculated Risk on 11/17/2022 09:22:00 AM

Today, in the CalculatedRisk Real Estate Newsletter: October Housing Starts: Record Number of Housing Units Under Construction

Excerpt:

The fourth graph shows housing starts under construction, Seasonally Adjusted (SA).There is much more in the post. You can subscribe at https://calculatedrisk.substack.com/ (Most content is available for free, so please subscribe).

Red is single family units. Currently there are 794 thousand single family units (red) under construction (SA). This is below the previous six months, and 36 thousand below the recent peak in April and May. Single family units under construction have peaked since single family starts are now declining. The reason there are so many homes under construction is probably due to supply constraints.

Blue is for 2+ units. Currently there are 928 thousand multi-family units under construction. This is the highest level since December 1973! For multi-family, construction delays are probably also a factor. The completion of these units should help with rent pressure.

Combined, there are 1.722 million units under construction. This is the all-time record number of units under construction.

Housing Starts Decreased to 1.425 million Annual Rate in October

by Calculated Risk on 11/17/2022 08:42:00 AM

From the Census Bureau: Permits, Starts and Completions

Housing Starts:

Privately‐owned housing starts in October were at a seasonally adjusted annual rate of 1,425,000. This is 4.2 percent below the revised September estimate of 1,488,000 and is 8.8 percent below the October 2021 rate of 1,563,000. Single‐family housing starts in October were at a rate of 855,000; this is 6.1 percent below the revised September figure of 911,000. The October rate for units in buildings with five units or more was 556,000.

Building Permits:

Privately‐owned housing units authorized by building permits in October were at a seasonally adjusted annual rate of 1,526,000. This is 2.4 percent below the revised September rate of 1,564,000 and is 10.1 percent below the October 2021 rate of 1,698,000. Single‐family authorizations in October were at a rate of 839,000; this is 3.6 percent below the revised September figure of 870,000. Authorizations of units in buildings with five units or more were at a rate of 633,000 in October.

emphasis added

Click on graph for larger image.

Click on graph for larger image.The first graph shows single and multi-family housing starts for the last several years.

Multi-family starts (blue, 2+ units) decreased in October compared to September. Multi-family starts were up 17.8% year-over-year in October.

Single-family starts (red) decreased in October and were down 20.8% year-over-year.

The second graph shows single and multi-family housing starts since 1968.

The second graph shows single and multi-family housing starts since 1968. This shows the huge collapse following the housing bubble, and then the eventual recovery.

Total housing starts in October were above expectations, however, starts in August and September were revised down slightly, combined.

I'll have more later …

Weekly Initial Unemployment Claims decrease to 222,000

by Calculated Risk on 11/17/2022 08:33:00 AM

The DOL reported:

In the week ending November 12, the advance figure for seasonally adjusted initial claims was 222,000, a decrease of 4,000 from the previous week's revised level. The previous week's level was revised up by 1,000 from 225,000 to 226,000. The 4-week moving average was 221,000, an increase of 2,000 from the previous week's revised average. The previous week's average was revised up by 250 from 218,750 to 219,000.The following graph shows the 4-week moving average of weekly claims since 1971.

emphasis added

Click on graph for larger image.

Click on graph for larger image.The dashed line on the graph is the current 4-week average. The four-week average of weekly unemployment claims increased to 221,000.

The previous week was revised up.

Weekly claims were above the consensus forecast.

Wednesday, November 16, 2022

Thursday: Housing Starts, Unemployment Claims, Philly Fed Mfg

by Calculated Risk on 11/16/2022 09:06:00 PM

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

Thursday:

• At 8:30 AM ET, Housing Starts for October. The consensus is for 1.410 million SAAR, down from 1.439 million SAAR.

• Also at 8:30 AM, The initial weekly unemployment claims report will be released. The consensus is for 230 thousand initial claims, up from 225 thousand last week.

• Also at 8:30 AM, the Philly Fed manufacturing survey for November. The consensus is for a reading of -8.0, up from -8.7.

• At 11:00 AM: the Kansas City Fed manufacturing survey for November.