RSS Feed

RSS Feed by Calculated Risk on 11/28/2022 08:57:00 AM

Monday, November 28, 2022

Housing November 28th Weekly Update: Inventory Decreased Slightly Week-over-week

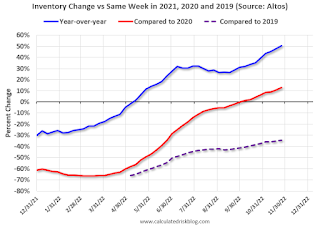

Active inventory decreased slightly. Here are the same week inventory changes for the last four years (usually inventory declines seasonally through the Winter):

2022: -4.8K (smaller than usual decrease in inventory)

2021: -9.9K

2020: -15.1K

2019: -18.4K

Altos reports inventory is down 0.8% week-over-week and down 2.3% from the peak on October 28th.

Click on graph for larger image.

Click on graph for larger image.

This inventory graph is courtesy of Altos Research.

Click on graph for larger image.

Click on graph for larger image.This inventory graph is courtesy of Altos Research.

As of November 25th, inventory was at 564 thousand (7-day average), compared to 569 thousand the prior week.

Compared to the same week in 2021, inventory is up 50.3% from 375 thousand, and compared to the same week in 2020 inventory is up 12.9% from 499 thousand. However, compared to 3 years ago (2019), inventory is down 34.4% from 859 thousand.

Here are the inventory milestones I’ve been watching for with the Altos data:

1. The seasonal bottom (happened on March 4, 2022, for Altos) ✅

2. Inventory up year-over-year (happened on May 20, 2022, for Altos) ✅

3. Inventory up compared to 2020 (happened on October 7, 2022, for Altos) ✅

4. Inventory up compared to 2019 (currently down 34.4%).

Mike Simonsen discusses this data regularly on Youtube.

1. The seasonal bottom (happened on March 4, 2022, for Altos) ✅

2. Inventory up year-over-year (happened on May 20, 2022, for Altos) ✅

3. Inventory up compared to 2020 (happened on October 7, 2022, for Altos) ✅

4. Inventory up compared to 2019 (currently down 34.4%).

Here is a graph of the inventory change vs 2021 (milestone 2 above), 2020 (milestone 3) and 2019 (milestone 4). The blue line is the year-over-year data, the red line is compared to two years ago, and dashed purple is compared to 2019.

A key will be if inventory declines slower than usual during the winter months.

Mike Simonsen discusses this data regularly on Youtube.

Four High Frequency Indicators for the Economy

by Calculated Risk on 11/28/2022 08:29:00 AM

These indicators are mostly for travel and entertainment. It was interesting to watch these sectors recover as the pandemic impact subsided.

The TSA is providing daily travel numbers.

This data is as of November 27th.

Click on graph for larger image.

Click on graph for larger image.This data shows the 7-day average of daily total traveler throughput from the TSA for 2019 (Light Blue), 2020 (Black), 2021 (Blue) and 2022 (Red).

The dashed line is the percent of 2019 for the seven-day average.

The 7-day average is 7.2% below the same week in 2019 (92.8% of 2019). (Dashed line)

Air travel - as a percent of 2019 - has picked up recently - but still below pre-pandemic levels.

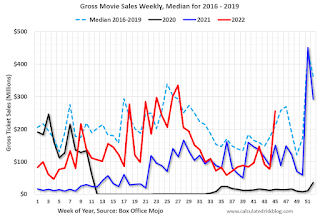

----- Movie Tickets: Box Office Mojo -----

This data shows domestic box office for each week and the median for the years 2016 through 2019 (dashed light blue).

This data shows domestic box office for each week and the median for the years 2016 through 2019 (dashed light blue).

This data shows domestic box office for each week and the median for the years 2016 through 2019 (dashed light blue).

This data shows domestic box office for each week and the median for the years 2016 through 2019 (dashed light blue). Black is 2020, Blue is 2021 and Red is 2022.

The data is from BoxOfficeMojo through November 24th.

Note that the data is usually noisy week-to-week and depends on when blockbusters are released.

Movie ticket sales were at $142 million last week, down about 45% from the median for the week.

Note that the data is usually noisy week-to-week and depends on when blockbusters are released.

Movie ticket sales were at $142 million last week, down about 45% from the median for the week.

NOTE: This is the previous week data, since hotel data wasn't released during the holiday week.

This graph shows the seasonal pattern for the hotel occupancy rate using the four-week average.

This graph shows the seasonal pattern for the hotel occupancy rate using the four-week average. The red line is for 2022, black is 2020, blue is the median, and dashed light blue is for 2021. Dashed purple is 2019 (STR is comparing to a strong year for hotels).

This data is through Nov 12th. The occupancy rate was up 0.9% compared to the same week in 2019.

The 4-week average of the occupancy rate is above the median rate for the previous 20 years (Blue) and close to 2019 levels.

Notes: Y-axis doesn't start at zero to better show the seasonal change.

Notes: Y-axis doesn't start at zero to better show the seasonal change.

This graph, based on weekly data from the U.S. Energy Information Administration (EIA), shows gasoline supplied compared to the same week of 2019.

Blue is for 2020. Purple is for 2021, and Red is for 2022.

As of November 18th, gasoline supplied was down 9.4% compared to the same week in 2019.

Recently gasoline supplied has been running below 2019 and 2021 levels - and sometimes below 2020.

Sunday, November 27, 2022

Sunday Night Futures

by Calculated Risk on 11/27/2022 07:34:00 PM

Weekend:

• Schedule for Week of November 27, 2022

Monday:

• AT 10:30 AM ET, Dallas Fed Survey of Manufacturing Activity for November. This is the last of the regional Fed manufacturing surveys for November.

From CNBC: Pre-Market Data and Bloomberg futures S&P 500 are down 17 and DOW futures are down 110 (fair value).

Oil prices were down over the last week with WTI futures at $76.06 per barrel and Brent at $83.47 per barrel. A year ago, WTI was at $70, and Brent was at $73 - so WTI oil prices are up 9% year-over-year.

Here is a graph from Gasbuddy.com for nationwide gasoline prices. Nationally prices are at $3.62 per gallon. A year ago, prices were at $3.39 per gallon, so gasoline prices are up $0.23 per gallon year-over-year.

Realtor.com Reports Weekly Active Inventory Up 49% Year-over-year; New Listings Down 17%

by Calculated Risk on 11/27/2022 10:20:00 AM

Realtor.com has monthly and weekly data on the existing home market. Here is their weekly report released today from Chief Economist Danielle Hale: Weekly Housing Trends View — Data Week Ending Nov 19, 2022. Note: They have data on list prices, new listings and more, but this focus is on inventory.

• Active inventory continued to grow, increasing 49% above one year ago. Inventory accelerated again, notching a sixth straight week of growth in the yearly trend roughly at or above 2%–in this case nearly double.

...

• New listings–a measure of sellers putting homes up for sale–were again down, dropping 17% from one year ago. This marks a twentieth straight week of year over year declines in homeowners listing their home for sale, a tangible reflection of the ongoing decline in seller confidence.

Here is a graph of the year-over-year change in inventory according to realtor.com.

Here is a graph of the year-over-year change in inventory according to realtor.com. Note the rapid increase in the YoY change earlier this year, from down 30% at the beginning of the year, to up 29% YoY at the beginning of July.

Then the Realtor.com data was stuck at up around 26% to 30% YoY for 14 weeks in a row. This was due to the slowdown in new listings, even as sales had fallen sharply.

Now YoY inventory is increasing again with even higher mortgage rates, suggesting sales are off more than new listings.

Saturday, November 26, 2022

Real Estate Newsletter Articles this Week: "With rising cancellations, the Census Bureau overestimates New Home sales"

by Calculated Risk on 11/26/2022 02:11:00 PM

At the Calculated Risk Real Estate Newsletter this week:

• New Home Sales Increased in October; Completed Inventory Increased With rising cancellations, the Census Bureau overestimates sales

• Lawler: Likely "Dramatic shift" in Household Formation has "Major implications" for 2023

• Final Look at Local Housing Markets in October

• Case-Shiller, FHFA House Prices Indexes and Conforming Loan Limits will be released on Tuesday

This is usually published 4 to 6 times a week and provides more in-depth analysis of the housing market.

You can subscribe at https://calculatedrisk.substack.com/

Most content is available for free (and no Ads), but please subscribe!

Schedule for Week of November 27, 2022

by Calculated Risk on 11/26/2022 08:11:00 AM

The key report this week is the November employment report on Friday.

Other key indicators include the 2nd estimate of Q3 GDP, the September Case-Shiller and FHFA house price indexes, October Personal Income & Outlays (and PCE), the November ISM manufacturing index, and November vehicle sales.

Fed Chair Powell speaks on the economic outlook, inflation and the labor market on Thursday.

10:30 AM: Dallas Fed Survey of Manufacturing Activity for November. This is the last of the regional Fed manufacturing surveys for November.

9:00 AM ET: S&P/Case-Shiller House Price Index for September.

9:00 AM ET: S&P/Case-Shiller House Price Index for September.This graph shows graph shows the Year over year change in the seasonally adjusted National Index, Composite 10 and Composite 20 indexes through the most recent report (the Composite 20 was started in January 2000).

The consensus is for a 14.4% year-over-year increase in the Composite 20 index for September.

9:00 AM: FHFA House Price Index for September. This was originally a GSE only repeat sales, however there is also an expanded index. The 2023 Conforming loan limits will also be announced.

7:00 AM ET: The Mortgage Bankers Association (MBA) will release the results for the mortgage purchase applications index.

8:15 AM: The ADP Employment Report for November. This report is for private payrolls only (no government). The consensus is for 200,000 jobs added, down from 239,000 in October.

8:30 AM: Gross Domestic Product (Second Estimate) and Corporate Profits (Preliminary), 3rd Quarter 2022. The consensus is that real GDP increased 2.7% annualized in Q3, up from the advance estimate of 2.6% in Q3.

9:45 AM: Chicago Purchasing Managers Index for November.

10:00 AM ET: Job Openings and Labor Turnover Survey for October from the BLS.

10:00 AM ET: Job Openings and Labor Turnover Survey for October from the BLS. This graph shows job openings (black line), hires (purple), Layoff, Discharges and other (red column), and Quits (light blue column) from the JOLTS.

Jobs openings increased in September to 10.717 million from 10.280 million in August.

10:00 AM: Pending Home Sales Index for October. The consensus is for a 5.0% decrease in the index.

1:30 PM: Speech, Fed Chair Jerome Powell, Economic Outlook, Inflation, and the Labor Market, At the Brookings Institution, 1775 Massachusetts Avenue N.W., Washington, D.C.

2:00 PM: the Federal Reserve Beige Book, an informal review by the Federal Reserve Banks of current economic conditions in their Districts.

10:30 AM: (likely) FDIC Quarterly Banking Profile, Third quarter.

8:30 AM: The initial weekly unemployment claims report will be released. The consensus is for 235 thousand initial claims, down from 240 thousand last week.

8:30 AM ET: Personal Income and Outlays, October 2022. The consensus is for a 0.4% increase in personal income, and for a 0.8% increase in personal spending. And for the Core PCE price index to increase 0.3%. PCE prices are expected to be up 6.2% YoY, and core PCE prices up 5.0% YoY.

10:00 AM: ISM Manufacturing Index for November. The consensus is for 50.0%, down from 50.2%.

10:00 AM: Construction Spending for October. The consensus is for 0.3% decrease in spending.

All day: Light vehicle sales for November.

All day: Light vehicle sales for November.The consensus is for 14.9 million SAAR in November, unchanged from the BEA estimate of 14.9 million SAAR in October (Seasonally Adjusted Annual Rate).

This graph shows light vehicle sales since the BEA started keeping data in 1967. The dashed line is the current sales rate.

8:30 AM: Employment Report for November. The consensus is for 200,000 jobs added, and for the unemployment rate to be unchanged at 3.7%.

8:30 AM: Employment Report for November. The consensus is for 200,000 jobs added, and for the unemployment rate to be unchanged at 3.7%.There were 261,000 jobs added in October, and the unemployment rate was at 3.7%.

This graph shows the job losses from the start of the employment recession, in percentage terms.

The current employment recession was by far the worst recession since WWII in percentage terms. However, as of August, all of the jobs had returned and, as of October, were 804 thousand above pre-pandemic levels.

Friday, November 25, 2022

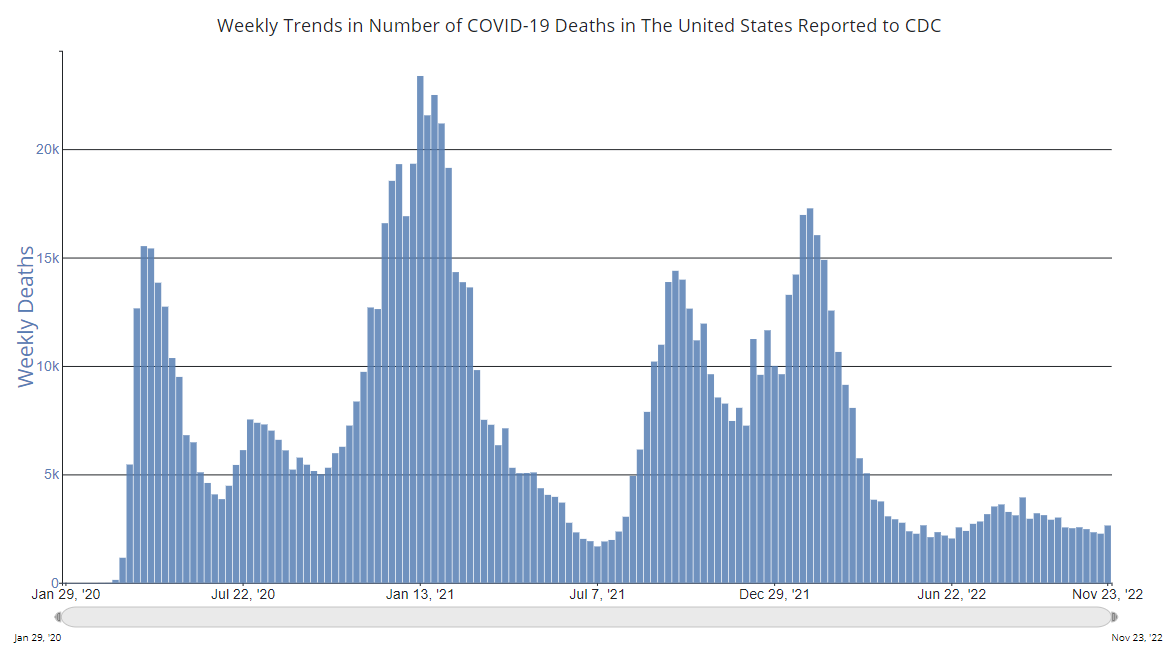

COVID Nov 25, 2022: Update on Cases, Hospitalizations and Deaths

by Calculated Risk on 11/25/2022 08:08:00 PM

NOTE: COVID stats are updated on Fridays.

On COVID (focus on hospitalizations and deaths). Data has switched to weekly.

| COVID Metrics | ||||

|---|---|---|---|---|

| Now | Week Ago | Goal | ||

| New Cases per Week2🚩 | 305,082 | 281,691 | ≤35,0001 | |

| Hospitalized2 | 21,293 | 21,578 | ≤3,0001 | |

| Deaths per Week2🚩 | 2,644 | 2,266 | ≤3501 | |

| 1my goals to stop weekly posts, 2Weekly for Cases, Currently Hospitalized, and Deaths 🚩 Increasing number weekly for Cases, Hospitalized, and Deaths ✅ Goal met. | ||||

Click on graph for larger image.

Click on graph for larger image.This graph shows the weekly (columns) number of deaths reported.

Case-Shiller, FHFA House Prices Indexes and Conforming Loan Limits will be released on Tuesday

by Calculated Risk on 11/25/2022 10:38:00 AM

Today, in the Calculated Risk Real Estate Newsletter: Case-Shiller, FHFA House Prices Indexes and Conforming Loan Limits will be released on Tuesday

Brief excerpt:

Last week, the National Association of Realtors® (NAR) reported that median house prices were up 6.6% year-over-year (YoY) in October. This is down from the peak growth rate of 25.2% YoY in May 2021.You can subscribe at https://calculatedrisk.substack.com/.

Last month, Case-Shiller reported that the National Index was up 13.0% YoY in August, down from a YoY peak of 20.8% in March 2022.

The median prices reported by the NAR are for the most recent month only, so the prices are very timely. However, the prices can be distorted by the mix of homes sold.

Case-Shiller is a repeat sales index (they compare the current price of home to the previous sales price), and it a three-month average. So, the most recent report (for August), was actually for homes closed in June, July and August.

Although median prices can be distorted by the mix and repeat sales indexes (like Case-Shiller and the FHFA) are more accurate measures of house prices, the median price index might provide earlier hints on the direction of prices.

The following graph shows YoY price changes for the NAR median house prices, Case-Shiller National price index, and the FHFA purchase-only index (Fannie and Freddie loans only).

Most of the time, the NAR median price leads the Case-Shiller index, and even though the Case-Shiller September index will show a solid YoY gain, I expect house price growth to decelerate further in coming months and turn negative YoY soon.

Philly Fed: State Coincident Indexes Increased in 20 States in October

by Calculated Risk on 11/25/2022 09:15:00 AM

From the Philly Fed:

The Federal Reserve Bank of Philadelphia has released the coincident indexes for the 50 states for October 2022. Over the past three months, the indexes increased in 36 states, decreased in 11 states, and remained stable in three, for a three-month diffusion index of 50. Additionally, in the past month, the indexes increased in 20 states, decreased in 22 states, and remained stable in eight, for a one-month diffusion index of -4. For comparison purposes, the Philadelphia Fed has also developed a similar coincident index for the entire United States. The Philadelphia Fed’s U.S. index increased 0.7 percent over the past three months and 0.1 percent in OctoberNote: These are coincident indexes constructed from state employment data. An explanation from the Philly Fed:

emphasis added

The coincident indexes combine four state-level indicators to summarize current economic conditions in a single statistic. The four state-level variables in each coincident index are nonfarm payroll employment, average hours worked in manufacturing by production workers, the unemployment rate, and wage and salary disbursements deflated by the consumer price index (U.S. city average). The trend for each state’s index is set to the trend of its gross domestic product (GDP), so long-term growth in the state’s index matches long-term growth in its GDP.

Click on map for larger image.

Click on map for larger image.Here is a map of the three-month change in the Philly Fed state coincident indicators. This map was all red during the worst of the Pandemic and also at the worst of the Great Recession.

The map is mostly positive on a three-month basis.

Source: Philly Fed.

And here is a graph is of the number of states with one month increasing activity according to the Philly Fed.

And here is a graph is of the number of states with one month increasing activity according to the Philly Fed. This graph includes states with minor increases (the Philly Fed lists as unchanged).

In October 23 states had increasing activity including minor increases.

In October 23 states had increasing activity including minor increases.

Thursday, November 24, 2022

Five Economic Reasons to be Thankful

by Calculated Risk on 11/24/2022 11:28:00 AM

Here are five economic reasons to be thankful this Thanksgiving. (Hat Tip to Neil Irwin who started doing this years ago)

1) The Unemployment Rate is Near 50 Year Low

The unemployment rate was at 3.7% in October. The unemployment rate is down from 14.7% in April 2020 (the highest since the Great Depression).

The unemployment rate was at 3.7% in October. The unemployment rate is down from 14.7% in April 2020 (the highest since the Great Depression).

The unemployment rate is down from 4.6% a year ago (October 2021).

This was just up from 3.5% in September - and that matched the lowest unemployment rate since 1969!

2) Low unemployment claims.

This graph shows the 4-week moving average of weekly claims since 1971.

This graph shows the 4-week moving average of weekly claims since 1971.

2) Low unemployment claims.

This graph shows the 4-week moving average of weekly claims since 1971.

This graph shows the 4-week moving average of weekly claims since 1971.Weekly claims were at 240,000 last week.

The dashed line on the graph is the current 4-week average.

The dashed line on the graph is the current 4-week average.

Even though weekly claims have moved up a little recently, the 4-week average is close to the lowest level in 50 years.

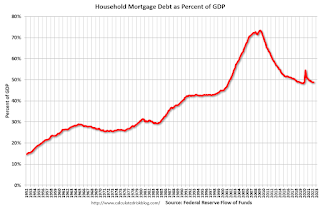

3) Mortgage Debt as a Percent of GDP is much lower than during Housing Bubble

This graph shows household mortgage debt as a percent of GDP.

This graph shows household mortgage debt as a percent of GDP.

3) Mortgage Debt as a Percent of GDP is much lower than during Housing Bubble

This graph shows household mortgage debt as a percent of GDP.

This graph shows household mortgage debt as a percent of GDP. Note this graph was impacted by the sharp decline in Q2 2020 GDP.

Mortgage debt is up $1.46 trillion from the peak during the housing bubble, but, as a percent of GDP is at 48.9%, down from a peak of 73.3% of GDP during the housing bust.

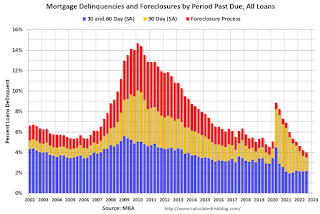

4) Mortgage Delinquency Rate at Lowest Level since at least 1979

Mortgage debt is up $1.46 trillion from the peak during the housing bubble, but, as a percent of GDP is at 48.9%, down from a peak of 73.3% of GDP during the housing bust.

4) Mortgage Delinquency Rate at Lowest Level since at least 1979

This graph, based on data from the MBA through Q3 2022, shows the percent of loans delinquent by days past due. Mortgage delinquencies were at the lowest level since the MBA survey started in 1979.

Note: The sharp increase in 2020 in the 90-day bucket was due to loans in forbearance (included as delinquent, but not reported to the credit bureaus).

The percent of loans in the foreclosure process increased year-over-year in Q3 with the end of the foreclosure moratoriums.

5) Household Debt burdens at Low Levels

This graph, based on data from the Federal Reserve, shows the Total Debt Service Ratio (DSR), and the DSR for mortgages (blue) and consumer debt (yellow).

This graph, based on data from the Federal Reserve, shows the Total Debt Service Ratio (DSR), and the DSR for mortgages (blue) and consumer debt (yellow).The Household debt service ratio was at 13.2% in 2007 and has fallen to under 10% now., and the DSR for mortgages (blue) are near the lowest level for the last 35 years.

This data suggests aggregate household cash flow is in a solid position.

This data suggests aggregate household cash flow is in a solid position.

Happy Thanksgiving to All!

Wednesday, November 23, 2022

Freddie Mac: Mortgage Serious Delinquency Rate decreased in October

by Calculated Risk on 11/23/2022 06:12:00 PM

Freddie Mac reported that the Single-Family serious delinquency rate in October was 0.66%, down from 0.67% September. Freddie's rate is down year-over-year from 1.32% in October 2021.

Freddie's serious delinquency rate peaked in February 2010 at 4.20% following the housing bubble and peaked at 3.17% in August 2020 during the pandemic.

These are mortgage loans that are "three monthly payments or more past due or in foreclosure".

Click on graph for larger image

Click on graph for larger image

Mortgages in forbearance are being counted as delinquent in this monthly report but are not reported to the credit bureaus.

The serious delinquency rate was at 0.60% just prior to the pandemic - almost back to that level.

Note that multi-family delinquencies have been increasing and were at 0.15% in October.

Q4 GDP Tracking: Moving on up

by Calculated Risk on 11/23/2022 12:49:00 PM

From BofA:

On net, today's data pushed up our 4Q US GDP tracking from 1.4% q/q saar to 1.8% q/q saar and left our 3Q US GDP tracking unchanged at 3.0% q/q saar. [Nov 23rd estimate]From Goldman:

emphasis added

We boosted our Q4 GDP tracking estimate by 0.5pp to +1.5% (qoq ar). [Nov 23rd estimate]And from the Altanta Fed: GDPNow

The GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the fourth quarter of 2022 is 4.3 percent on November 23, up from 4.2 percent on November 17. [Nov 23rd estimate]

New Home Sales Increased in October; Completed Inventory Increased

by Calculated Risk on 11/23/2022 10:39:00 AM

Today, in the Calculated Risk Real Estate Newsletter: New Home Sales Increased in October; Completed Inventory Increased

Brief excerpt:

The next graph shows the months of supply by stage of construction. “Months of supply” is inventory at each stage, divided by the sales rate.You can subscribe at https://calculatedrisk.substack.com/.

There are 1.2 months of completed supply (red line). This is getting close to the normal level.

The inventory of new homes under construction is at 5.7 months (blue line). This elevated level of homes under construction is due to supply chain constraints.

And a record 111 thousand homes have not been started - about 2.1 months of supply (grey line) - about double the normal level. Homebuilders are probably waiting to start some homes until they have a firmer grasp on prices and demand.

...

First, as I discussed two months ago, the Census Bureau overestimates sales, and underestimates inventory when cancellation rates are rising, see: New Home Sales and Cancellations: Net vs Gross Sales. So, take the headline sales number with a large grain of salt - the actual negative impact on the homebuilders is far greater than the headline number suggests!

...

There are a large number of homes under construction, and this suggests we will see a sharp increase in completed inventory over the next several months - and that will put pressure on new home prices.

New Home Sales Increase to 632,000 Annual Rate in October

by Calculated Risk on 11/23/2022 10:08:00 AM

The Census Bureau reports New Home Sales in October were at a seasonally adjusted annual rate (SAAR) of 632 thousand.

The previous two months were revised down.

Sales of new single‐family houses in October 2022 were at a seasonally adjusted annual rate of 632,000, according to estimates released jointly today by the U.S. Census Bureau and the Department of Housing and Urban Development. This is 7.5 percent above the revised September rate of 588,000, but is 5.8 percent below the October 2021 estimate of 671,000.

emphasis added

Click on graph for larger image.

Click on graph for larger image.The first graph shows New Home Sales vs. recessions since 1963. The dashed line is the current sales rate.

New home sales are below pre-pandemic levels.

The second graph shows New Home Months of Supply.

The months of supply decreased in October to 8.9 months from 9.4 months in September.

The months of supply decreased in October to 8.9 months from 9.4 months in September. The all-time record high was 12.1 months of supply in January 2009. The all-time record low was 3.5 months, most recently in October 2020.

This is well above the top of the normal range (about 4 to 6 months of supply is normal).

"The seasonally‐adjusted estimate of new houses for sale at the end of October was 470,000. This represents a supply of 8.9 months at the current sales rate."

The last graph shows sales NSA (monthly sales, not seasonally adjusted annual rate).

The last graph shows sales NSA (monthly sales, not seasonally adjusted annual rate).In October 2022 (red column), 48 thousand new homes were sold (NSA). Last year, 51 thousand homes were sold in October.

The all-time high for October was 105 thousand in 2005, and the all-time low for October was 23 thousand in 2010.

This was above expectations, however sales in the two previous months were revised down. I'll have more later today.

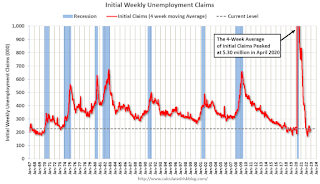

Weekly Initial Unemployment Claims increase to 240,000

by Calculated Risk on 11/23/2022 08:35:00 AM

The DOL reported:

In the week ending November 19, the advance figure for seasonally adjusted initial claims was 240,000, an increase of 17,000 from the previous week's revised level. The previous week's level was revised up by 1,000 from 222,000 to 223,000. The 4-week moving average was 226,750, an increase of 5,500 from the previous week's revised average. The previous week's average was revised up by 250 from 221,000 to 221,250.The following graph shows the 4-week moving average of weekly claims since 1971.

emphasis added

Click on graph for larger image.The dashed line on the graph is the current 4-week average. The four-week average of weekly unemployment claims increased to 226,750.

The previous week was revised up.

Weekly claims were above the consensus forecast.

MBA: Mortgage Applications Increase in Latest Weekly Survey

by Calculated Risk on 11/23/2022 07:00:00 AM

From the MBA: Mortgage Applications Increase in Latest MBA Weekly Survey

Mortgage applications increased 2.2 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending November 18, 2022. Last week’s results include an adjustment for the observance of Veterans Day.

... The Refinance Index increased 2 percent from the previous week and was 86 percent lower than the same week one year ago. The seasonally adjusted Purchase Index increased 3 percent from one week earlier. The unadjusted Purchase Index increased 9 percent compared with the previous week and was 41 percent lower than the same week one year ago.

“The 30-year fixed-rate mortgage fell for the second week in a row to 6.67 percent and is now down almost 50 basis points from the recent peak of 7.16 percent one month ago,” said Joel Kan, MBA’s Vice President and Deputy Chief Economist. “The decrease in mortgage rates should improve the purchasing power of prospective homebuyers, who have been largely sidelined as mortgage rates have more than doubled in the past year. As a result of the drop in mortgage rates, both purchase and refinance applications picked up slightly last week. However, refinance activity is still more than 80 percent below last year’s pace.”

Added Kan, “With the decline in rates, the ARM share of applications also decreased to 8.8 percent of loans last week, down from the range of 10 and 12 percent during the past two months.”

...

The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($647,200 or less) decreased to 6.67 percent from 6.90 percent, with points increasing to 0.68 from 0.56 (including the origination fee) for 80 percent loan-to-value ratio (LTV) loans.

emphasis added

Click on graph for larger image.

Click on graph for larger image.The first graph shows the refinance index since 1990.

With higher mortgage rates, the refinance index has declined sharply this year.

The refinance index is near the lowest level since the year 2000.

The second graph shows the MBA mortgage purchase index

According to the MBA, purchase activity is down 41% year-over-year unadjusted.

According to the MBA, purchase activity is down 41% year-over-year unadjusted.The purchase index is 4% below the pandemic low and just up from the lowest level since 2015.

Note: Red is a four-week average (blue is weekly).

Note: Red is a four-week average (blue is weekly).

Tuesday, November 22, 2022

Wednesday: Unemployment Claims, Durable Goods, New Home Sales, FOMC Minutes

by Calculated Risk on 11/22/2022 08:50:00 PM

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

Wednesday:

• At 7:00 AM ET, The Mortgage Bankers Association (MBA) will release the results for the mortgage purchase applications index.

• At 8:30 AM, The initial weekly unemployment claims report will be released. The consensus is for 225 thousand initial claims, up from 222 thousand last week.

• At 8:30 AM, Durable Goods Orders for October from the Census Bureau. The consensus is for a 0.4% increase in durable goods orders.

• At 10:00 AM, New Home Sales for October from the Census Bureau. The consensus is for 570 thousand SAAR, down from 603 thousand in September.

• At 2:00 PM, FOMC Minutes, Meeting of November 1-2, 2022

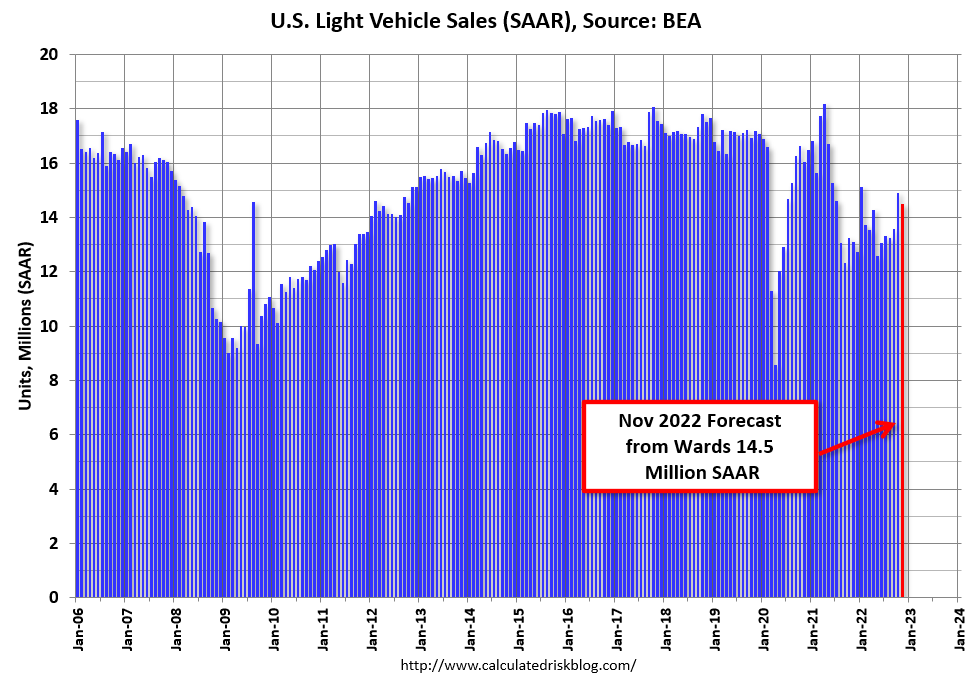

November Vehicle Sales Forecast: Down slightly from October; Up 11% Year-over-year

by Calculated Risk on 11/22/2022 02:58:00 PM

From WardsAuto: November U.S. Light-Vehicle Sales to Slow from Prior Month; Still Point to Stronger Q4 (pay content). Brief excerpt:

Although heavily laden with pickups, inventory will rise again in November, lifting the prospects that the year ends on a strong note by overcoming challenges including myriad economy-related headwinds, high prices, potential railroad labor strike and others.

Click on graph for larger image.

Click on graph for larger image.This graph shows actual sales from the BEA (Blue), and Wards forecast for November (Red).

The Wards forecast of 14.5 million SAAR, would be down 3% from last month, but up 11% from a year ago (sales weakened in the second half of 2021, due to supply chain issues).

Vehicle sales are usually a transmission mechanism for Federal Open Market Committee (FOMC) policy, far behind housing. However, this time, vehicle sales have been suppressed by supply chain issues, and sales will probably not be significantly impacted by higher interest rates.

Black Knight: Mortgage Delinquency Rate Increased in October, Impacted by Hurricane

by Calculated Risk on 11/22/2022 12:43:00 PM

From Black Knight: Black Knight’s First Look: Prepayment Activity Hit Record Low in October as Rates Topped 7%; Mortgage Delinquencies Up 4.5% in First Signs of Hurricane Ian Impact

• Prepayments fell 16.5% to a single-month mortality (SMM) rate of 0.48%, well below the previous record of 0.55% and the lowest recorded since at least 2000 when Black Knight began reporting the metricAccording to Black Knight's First Look report, the percent of loans delinquent increased 4.5% in October compared to September and decreased 22% year-over-year.

• The national delinquency rate rose 4.5% in October to 2.91% – up 12 basis points since September – driven by a sharp 9.4% rise in 30-day delinquencies

• Florida led the jump in new early delinquencies (+19K) – with the state delinquency rate rising 53 basis points to 3.42% -- giving an initial indication of Hurricane Ian impact

• Loans 60 days past due ticked up 2.9% nationally, while those 90 or more days delinquent saw continued – if modest – improvement, inching down another 1.5% in October

• October’s 19.6K foreclosure starts represented a 7% increase that partly reversed September’s decline, but are still 55% below pre-pandemic levels

• Foreclosure starts were initiated on 4% of existing serious delinquencies in October, up slightly from September but still less than half the rate seen in the years leading up to the pandemic

• Active foreclosure inventory held steady as volumes have remained subdued in 2022 due to still historically low foreclosure start levels

emphasis added

Black Knight reported the U.S. mortgage delinquency rate (loans 30 or more days past due, but not in foreclosure) was 2.91% in October, down from 2.78% in September.

The percent of loans in the foreclosure process increased slightly in October at 0.35%, from 0.35% in September.

The number of delinquent properties, but not in foreclosure, is down 555,000 properties year-over-year, and the number of properties in the foreclosure process is up 48,000 properties year-over-year.

| Black Knight: Percent Loans Delinquent and in Foreclosure Process | ||||

|---|---|---|---|---|

| Oct 2022 | Sept 2022 | Oct 2021 | Oct 2020 | |

| Delinquent | 2.91% | 2.78% | 3.74% | 6.44% |

| In Foreclosure | 0.35% | 0.35% | 0.26% | 0.33% |

| Number of properties: | ||||

| Number of properties that are delinquent, but not in foreclosure: | 1,557,000 | 1,491,000 | 1,986,000 | 3,437,000 |

| Number of properties in foreclosure pre-sale inventory: | 186,000 | 185,000 | 138,000 | 178,000 |

| Total Properties | 1,743,000 | 1,677,000 | 2,125,000 | 3,616,000 |

Lawler: Likely "Dramatic shift" in Household Formation has "Major implications" for 2023

by Calculated Risk on 11/22/2022 09:17:00 AM

Today, in the Calculated Risk Real Estate Newsletter: Lawler: Likely "Dramatic shift" in Household Formation has "Major implications" for 2023

A brief excerpt:

Below is a chart showing the CPS/ASEC estimates of the % of 25-34 year olds living alone.There is much more in the article. You can subscribe at https://calculatedrisk.substack.com/

According to CPS/ASEC estimates, the % of adults (18+) living alone jumped to 14.9% in March 2022 from 14.4% in March 2021, and the % of households with just one member climbed to 28.9% from 28.2%. Both “living alone” measures (share of population and share of households) were at the highest levels ever recorded by the CPS/ASEC. The jump in one-person households was the major reason why the average household size as measured by the CPS/ASEC plunged to 2.50 in March 2022 (the lowest ever recorded) from 2.54 in March 2021. (Unrounded the average household size fell by .0341). In terms of share of total households, the one-person share increased the most for young adults (up to 39 years) and for 65-74 year olds. ...

... there is strong reason to believe that household growth is no longer getting the “boost” from behavioral changes as that suggested from March 2021 to March 2021. If that turns out to be true, then household growth is or will return back to growth more consistent with underlying population changes by age group, a development that would imply household growth over the next year of about half that apparently experienced from early 2021 to early 2022. Such a dramatic shift has major implications for projections of rent growth and home price growth next year.

{kind=link}