RSS Feed

RSS Feed by Calculated Risk on 4/13/2012 01:20:00 PM

Friday, April 13, 2012

Bernanke: "Some Reflections on the Crisis and the Policy Response"

Note: Bernanke didn't discuss current monetary policy.

From Fed Chairman Ben Bernanke: "Some Reflections on the Crisis and the Policy Response"

On the originate-to-distribute model:

Private-sector risk management also failed to keep up with financial innovation in many cases. An important example is the extension of the traditional originate-to-distribute business model to encompass increasingly complex securitized credit products, with wholesale market funding playing a key role. In general, the originate-to-distribute model breaks down the process of credit extension into components or stages--from origination to financing and to the postfinancing monitoring of the borrower's ability to repay--in a manner reminiscent of how manufacturers distribute the stages of production across firms and locations. This general approach has been used in various forms for many years and can produce significant benefits, including lower credit costs and increased access of consumers and small and medium-sized businesses to capital markets. However, the expanded use of this model to finance subprime mortgages through securitization was mismanaged at several points, including the initial underwriting, which deteriorated markedly, in part because of incentive schemes that effectively rewarded originators for the quantity rather than the quality of the mortgages extended. Loans were then packaged into securities that proved complex, opaque, and unwieldy; for example, when defaults became widespread, the legal agreements underlying the securitizations made reasonable modifications of troubled mortgages difficult. Rating agencies' ratings of asset-backed securities were revealed to be subject to conflicts of interest and faulty models. At the end of the chain were investors who often relied mainly on ratings and did not make distinctions among AAA-rated securities. Even if the ultimate investors wanted to do their own credit analysis, the information needed to do so was often difficult or impossible to obtain.CR Note: This wasn't just for subprime. Even worse were the Alt-A loans! Also I don't think Bernanke spent enough time on the failure of regulators to recognize the very loose lending.

I think the housing bubble (and subsequent bust) can be understood very well by looking at each step of originate-to-distribute model, and also at the willful lack of regulatory oversight. Bernanke suggests housing was just the trigger, but if the regulators couldn't see that loaning people 100+ LTV, with stated income, and a low teaser rate would end poorly, then there was no way they could see the systemic risk!

Bernanke concludes:

The financial crisis of 2007-09 was difficult to anticipate for two reasons: First, financial panics, being to a significant extent self-fulfilling crises of confidence, are inherently difficult to foresee. Second, although the crisis bore some resemblance at a conceptual level to the panics known to Bagehot, it occurred in a rather different institutional context and was propagated and amplified by a number of vulnerabilities that had developed outside the traditional banking sector. Once identified, however, the panic could be addressed to a significant extent using classic tools, including backstop liquidity provision by central banks, both here and abroad.I disagree that the crisis "was difficult to anticipate". I think the potential for the housing bust to lead to a financial crisis was fairly obvious (I first mentioned the possibility of a financial crisis as a result of the then coming housing bust in 2005).

Key Measures of Inflation in March

by Calculated Risk on 4/13/2012 11:54:00 AM

Earlier today the BLS reported:

The Consumer Price Index for All Urban Consumers (CPI-U) increased 0.3 percent in March on a seasonally adjusted basis ... The index for all items less food and energy rose 0.2 percent in MarchThe Cleveland Fed released the median CPI and the trimmed-mean CPI this morning:

According to the Federal Reserve Bank of Cleveland, the median Consumer Price Index rose 0.2% (2.2% annualized rate) in March. The 16% trimmed-mean Consumer Price Index increased 0.2% (2.7% annualized rate) during the month.Note: The Cleveland Fed has the median CPI details for March here.

...

Earlier today, the BLS reported that the seasonally adjusted CPI for all urban consumers increased 0.3% (3.5% annualized rate) in March. The CPI less food and energy increased 0.2% (2.8% annualized rate) on a seasonally adjusted basis.

Click on graph for larger image.

Click on graph for larger image.This graph shows the year-over-year change for these four key measures of inflation. On a year-over-year basis, the median CPI rose 2.4%, the trimmed-mean CPI rose 2.4%, and core CPI rose 2.3%. Core PCE is for February and increased 1.9% year-over-year.

These measures show inflation on a year-over-year basis is mostly still above the Fed's 2% target.

Consumer Sentiment declines slightly in April to 75.7

by Calculated Risk on 4/13/2012 09:55:00 AM

Click on graph for larger image.

The preliminary Reuters / University of Michigan consumer sentiment index for April declined slightly to 75.7, down from the final March reading of 76.2.

This was below the consensus forecast of 76.2. Overall sentiment is still fairly weak - probably due to a combination of the high unemployment rate, high gasoline prices and sluggish economy - however sentiment has rebounded from the decline last summer and is up from 69.8 in April 2011.

BLS: CPI increases 0.3% in March

by Calculated Risk on 4/13/2012 08:33:00 AM

The Consumer Price Index for All Urban Consumers (CPI-U) increased 0.3 percent in March on a seasonally adjusted basis, the U.S. Bureau of Labor Statistics reported today. Over the last 12 months, the all items index increased 2.7 percent before seasonal adjustment.I'll post a graph later today after the Cleveland Fed releases the median and trimmed-mean CPI. This was at the consensus forecast of a 0.3% increase in CPI and a 0.2% increase in core CPI.

...

The gasoline index continued to rise, more than offsetting a decline in the household energy index and leading to a 0.9 percent increase in the energy index. The food index rose 0.2 percent as the index for meats, poultry, fish, and eggs increased notably.

The index for all items less food and energy rose 0.2 percent in March after increasing 0.1 percent in February.

Thursday, April 12, 2012

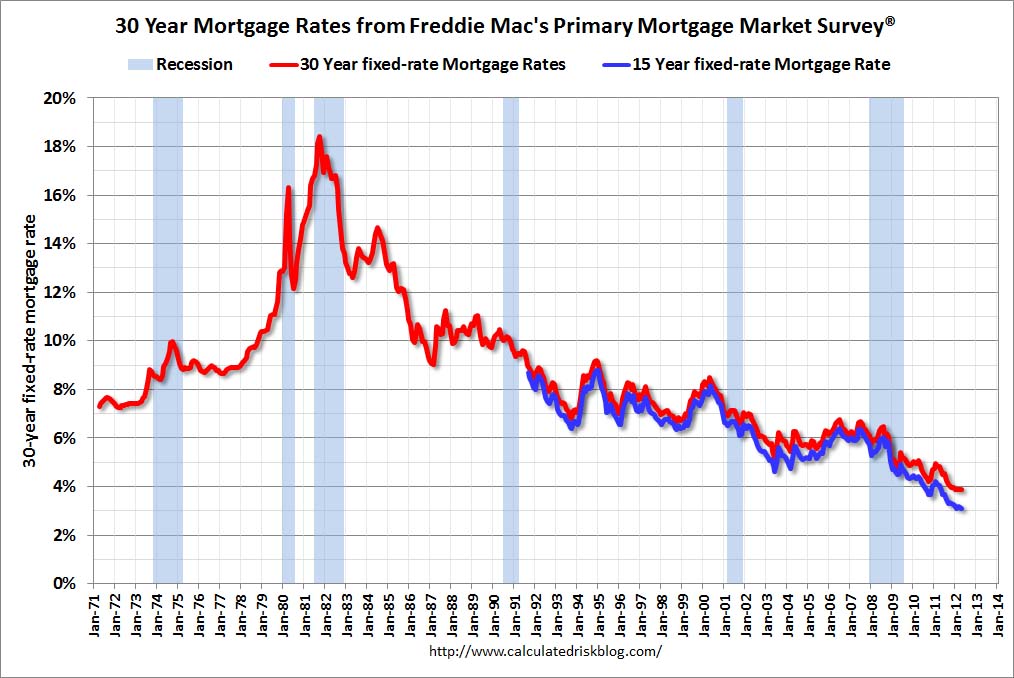

Freddie Mac: 15-Year Fixed-Rate Mortgage Hits New All-Time Record

by Calculated Risk on 4/12/2012 08:52:00 PM

From Freddie Mac: 15-Year Fixed-Rate Mortgage Hits New All-Time Record Low

Freddie Mac (OTC: FMCC) today released the results of its Primary Mortgage Market Survey® (PMMS®), showing average fixed mortgage rates declining for the third consecutive week ... The 30-year fixed averaged just above its record low while the 15-year fixed averaged a new all-time record low of 3.11 percent breaking its previous low of 3.13 percent on March 8, 2012.

...

30-year fixed-rate mortgage (FRM) averaged 3.88 percent with an average 0.7 point for the week ending April 12, 2012, down from last week when it averaged 3.98 percent. Last year at this time, the 30-year FRM averaged 4.91 percent.

Click on graph for larger image.

Click on graph for larger image.This graph shows the 15 and 30 year fixed rates from the Freddie Mac survey. The Primary Mortgage Market Survey® started in 1971 (15 year in 1991).

This reminds me: I had an 11% assumable mortgage on a house I was selling in the early '80s, and the "low" mortgage rate was a strong selling feature!