RSS Feed

RSS Feed by Calculated Risk on 9/29/2010 09:26:00 PM

Wednesday, September 29, 2010

Two Stories: JPMorgan halts some foreclosures, Fed to release crisis transaction details

Here are two stories we've been discussing in the comments ...

From David Streitfeld at the NY Times: JPMorgan Suspending Foreclosures

JPMorgan Chase, said it was halting 56,000 foreclosures because some of its employees might have improperly signed court documents. All of the suspensions are in the 23 states where foreclosures must be approved by a court, including New York, New Jersey, Connecticut, Florida and Illinois.It is amazing that the servicers haven't reviewed all their procedures already ...

And from Fed Chairman Ben Bernanke: Regulatory Reform Implementation

A final element of the Federal Reserve's efforts to implement the Dodd-Frank Act relates to the transparency of our balance sheet and liquidity programs. Well before enactment, we were providing a great deal of relevant information on our website, in statistical releases, and in regular reports to the Congress. Under a framework established by the act, the Federal Reserve will, by December 1, provide detailed information regarding individual transactions conducted across a range of credit and liquidity programs over the period from December 1, 2007, to July 20, 2010. This information will include the names of counterparties, the date and dollar value of individual transactions, the terms of repayment, and other relevant information. On an ongoing basis, subject to lags specified by the Congress to protect the efficacy of the programs, the Federal Reserve also will routinely provide information regarding the identities of counterparties, amounts financed or purchased and collateral pledged for transactions under the discount window, open market operations, and emergency lending facilities.Apparently disclosure isn't a problem now.

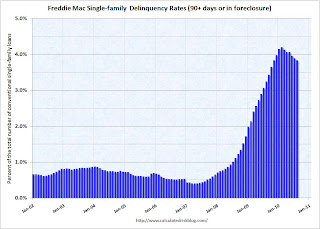

Fannie Mae and Freddie Mac: Serious Delinquent Rates decline

by Calculated Risk on 9/29/2010 05:01:00 PM

Click on graph for larger image in new window.

Fannie Mae reported today that the rate of serious delinquencies - at least 90 days behind - for conventional loans in its single-family guarantee business decreased to 4.82% in July, down from 4.99% in June - and up from 4.17% in July 2009.

"Includes seriously delinquent conventional single-family loans as a percent of the total number of conventional single-family loans."

The second graph is for the delinquency rate for Freddie Mac. The rate declined to 3.83% in August (Freddie reports a month quicker than Fannie), from 3.89% in July.

The second graph is for the delinquency rate for Freddie Mac. The rate declined to 3.83% in August (Freddie reports a month quicker than Fannie), from 3.89% in July.

Some of the rapid increase last year was probably because of foreclosure moratoriums, and distortions from modification programs because loans in trial mods were considered delinquent until the modifications were made permanent.

More modifications have become permanent and no longer counted as delinquent, and Fannie Mae and Freddie Mac are foreclosing again (they have a record number of REOs) - so there has been a decline in the delinquency rate.

Fed's Rosengren: Fed must respond "vigorously, creatively, thoughtfully, and persistently"

by Calculated Risk on 9/29/2010 01:31:00 PM

I cautioned that today was Fed speech day! Boston Fed president Eric Rosengren is currently a voting member of the FOMC ...

From Rosengren: How Should Monetary Policy Respond to a Slow Recovery?

I’ve called this talk “How Should Monetary Policy Respond to a Slow Recovery?” My answer to that question is: vigorously, creatively, thoughtfully, and persistently, as long as we have options at our disposal. And we do have options, despite having pushed short-term rates to the zero lower bound.On unemployment:

[T]he most recent recession is far less a reflection of dislocation in a few industries but rather reflects a general decline in almost all industries. ... in this recession there has been a peak to trough loss of employment of 5 percent or greater in construction, manufacturing, retail trade, wholesale trade, transportation, information technology, financial activities, and professional and business services. To me, this does not suggest that the driver is structural change in the economy increasing job mismatches – although no doubt some of that exists – but instead I see here a widespread decline in demand across most industries.And on QE2:

Now I’d like to make a few observations on Fed purchases of Treasury securities.And his conclusion:

First, the positives: Purchases of long-term Treasury securities are likely to push down long-term interest rates on Treasury bonds, but also are likely to reduce rates on other long-term securities. Some have argued that it would be difficult to reduce Treasury rates further, but Figure 13 highlights, importantly, that U.S. Treasury rates are still well above the zero bound, roughly equivalent to rates in Germany, and well above long-term rates in Japan.

Now some concerns: While purchases of Treasury securities have the advantage of not directly “allocating credit” to a particular industry, they have the disadvantage of only indirectly affecting the private borrowing rates that more directly affect private investment spending. In addition, Treasury purchases raise for some a concern that the Fed intends to monetize the federal debt, using monetary policy to accommodate the financing of fiscal policy. I can assure you that we have no desire or intention whatsoever to do so.

While lower long-term rates are likely the primary channel through which asset purchases would influence the economy, purchases of Treasury or mortgage-backed securities also expand the Federal Reserve’s balance sheet and increase the amount of reserves in the financial system. This expansion of reserves might serve as an effective signal that highlights the determination of the Federal Reserve to reduce disinflationary pressures.

Certainly, views on securities purchases differ within the ranks of policymakers and all manner of observers. I would just reiterate that it is important to keep firmly in mind the goal of such purchases: to stimulate the economy by reducing long-term interest rates to a level that is more consistent with where they would be, were we able to further reduce the federal funds rate.

While the economy is growing, it is currently growing too slowly to significantly reduce the unemployment rate or stem disinflationary pressures created by the high degree of slack in the economy. While fiscal policies may be the most effective way to stimulate the economy when short-term interest rates approach the zero bound, unconventional monetary policies provide additional policy options. Of course, policymakers need to carefully weigh the benefits and costs of unconventional monetary policy – some of which I have tried to share with you today. Yet all in all, my firm view is that it is important that policymakers be open to implementing policies consistent with achieving full employment, and an appropriate level of inflation, within a reasonable time frame.There is much more in this speech.

Fed's Plosser opposes QE2

by Calculated Risk on 9/29/2010 12:49:00 PM

With QE2 arriving on November 3rd - barring an upside surprise in the economic data - it is interesting to hear the views of the Fed presidents.

From Philadelphia Fed President Charles Plosser: Economic Outlook. On QE2:

[I]t is difficult, in my view, to see how additional asset purchases by the Fed, even if they move interest rates on long-term bonds down by 10 or 20 basis points, will have much impact on the near-term outlook for employment. Sending a signal that monetary policymakers are taking actions in an attempt to directly affect the near-term path of the unemployment rate, and then for those actions to have no demonstrable effects, would hurt the Fed’s credibility and possibly erode the effectiveness of our future actions to ensure price stability. It also risks leading the public to believe that the Fed is seeking to monetize the deficit and make it more difficult to return to normal policy when the time comes.And on the outlook:

While the near-term outlook has softened a bit, I expect growth in the national economy to be around 3 to 3½ percent over the next two years, with stronger business spending on equipment and software, moderate growth of consumer spending, and gradual improvement in household balance sheets.Although I agree that there will be some geographic and skill mismatches going forward because of the housing bubble - I don't think that is the main problem impacting the labor markets right now. There are many highly skilled people currently unemployed in many sectors - so Plosser's view appears incorrect.

The unemployment rate continues to be one of the biggest challenges our economy faces. Although unemployment will begin to decline gradually, it will take some time for it to return to its long-run level. As the economy strengthens and firms become convinced that the recovery is sustainable, hiring will pick up over the rest of this year and in 2011. But it may take even longer to address the sectoral, geographic, and skill imbalances that seem to plague the labor markets.

I expect inflation to remain subdued. As long as inflation expectations remain well anchored, I see little risk of a period of sustained deflation.

I'm surprised that Plosser is sticking with his optimistic (so far wrong) economic outlook. Right now Plosser is an alternate member of the FOMC and next year he will be a voting member (along with several other Fed presidents with similar views).

Fed's Kocherlakota revises down forecast

by Calculated Risk on 9/29/2010 10:31:00 AM

Minneapolis Federal Reserve President Narayana Kocherlakota spoke in London today. He has been one of more optimistic Fed presidents, and he revised down his forecast today ...

From Kocherlakota: Economic Outlook and the Current Tools of Monetary Policy

Our September estimates are distinctly lower than our August estimates. I now expect GDP growth to be around 2.4 percent in the second half of 2010 and around 2.5 percent in 2011.This still seems too optimistic, but he is moving in the right direction.

...

From the fourth quarter of 2009 through the second quarter of 2010, the change in the PCE price level was just over 0.5 percent, which works out to an annual rate of just over 1 percent. ... I expect inflation to remain at about this level during the rest of this year. However, our Minneapolis forecasting model predicts that it will rise back into the more desirable 1.5-2 percent range in 2011.

...

To summarize: GDP is growing, but more slowly than I expected or than we would like. Inflation is a little low, but only temporarily. The behavior of unemployment is deeply troubling.

And on the coming QE2:

My own guess is that further uses of QE would have a more muted effect on Treasury term premia. Financial markets are functioning much better in late 2010 than they were in early 2009. As a result, the relevant spreads are lower, and I suspect that it will be somewhat more challenging for the Fed to impact them.Kocherlakota is currently an alternate member of the FOMC and will be a voting member next year. It is interesting that certain Fed presidents are now revising down their overly optimistic forecasts - all but guaranteeing QE2 (even if he thinks it will have little impact).

Estimate of Decennial Census impact on September payroll employment: minus 78,000

by Calculated Risk on 9/29/2010 10:02:00 AM

The Census Bureau released the weekly payroll data for the week ending September 18th today (ht Bob_in_MA).

If we subtract the number of temporary 2010 Census workers in the week containing the 12th of the month, from the same week for the previous month - this provides a close estimate for the impact of the Census hiring on payroll employment.

The Census Bureau releases the actual number with the employment report.

Click on graph for larger image in new window.

Click on graph for larger image in new window.

This graph shows the number of Census workers paid each week. The red labels are the weeks of the BLS payroll survey.

The Census payroll decreased from 83,955 for the week ending August 14th to 6,038 for the week ending September 18th.

So my estimate for the impact of the Census on September payroll employment is minus 78 thousand (this will probably be close). The employment report will be released on October 8th, and the headline number for September - including Census numbers - will probably be close to zero. But a key number will be the hiring ex-Census (so we will add back the Census workers again this month).

The following table compares the weekly payroll report estimate to the monthly BLS report on Census hiring - this shows the estimate is usually very close:

| Payroll, Weekly Pay Period | Payroll, Monthly BLS | Change based on weekly report | Actual Change (monthly) | |

|---|---|---|---|---|

| Jan | 25 | 24 | ||

| Feb | 41 | 39 | 16 | 15 |

| Mar | 96 | 87 | 55 | 48 |

| Apr | 156 | 154 | 61 | 67 |

| May | 574 | 564 | 418 | 410 |

| Jun | 344 | 339 | -230 | -225 |

| Jul | 200 | 196 | -144 | -143 |

| Aug | 84 | 82 | -116 | -114 |

| Sep | 6 | -78 | ||

| All thousands | ||||

There are very few temporary decennial workers left on the payroll, and this month marks the end of the weekly payroll report from the Census Bureau: "These data will continue through the end of September with the last release of data being the week of Sept. 26-Oct. 2."

I'll have more on the September employment report (due Oct 8th) this Sunday in the weekly schedule.